Key Takeaways

- USDC dropped to $0.87 in March 2023 when $3.3B got frozen at Silicon Valley Bank, 100% reserves mean nothing if you can’t access them

- Attestations verify balances on one date; audits verify controls over time, most stablecoins skip the audit, creating transparency gaps

- USDC holds 45% in BlackRock’s USDXX with monthly attestations; USDT dropped commercial paper but hides 15.9% in undisclosed investments

- The GENIUS Act (July 2025) requires monthly attestations, limits reserves to Treasuries/cash/repos, and gives holders 14-day bankruptcy recovery

- Mid-market companies can’t redeem directly, $100K minimums force reliance on secondary markets that freeze during crises

- Keep stablecoin exposure under 5% of liquid assets, convert to fiat daily/weekly, and set 2% de-peg alerts

It was 9:47 AM Eastern on a Saturday morning when USDC, the second-largest stablecoin, pegged at exactly $1.00 and started trading at $0.87 on Coinbase.

Within two hours, corporate treasury teams across North America faced a crisis they’d never planned for. Supplier payments that were supposed to settle at $1.00 per USDC were suddenly worth 13% less. A $2 million international wire translated to $1.74 million in actual purchasing power. Automated payment systems that assumed “stable” suddenly weren’t.

The culprit? Circle, USDC’s issuer, disclosed that $3.3 billion of its $40 billion in reserves,8.25% of total backing, was stuck at Silicon Valley Bank, which had just collapsed under FDIC receivership. Despite being “100% backed by cash and cash equivalents,” those reserves were temporarily inaccessible. The market reacted instantly.

For three days, CFOs learned a brutal lesson: “Fully backed” doesn’t guarantee “fully liquid” during banking system stress.

Circle’s reserves were indeed there, verified by monthly attestations from Deloitte. Every dollar of USDC was backed 1:1. But when your custodian bank fails on a Friday, reserves don’t matter if you can’t access them on Saturday.

The de-peg only reversed after the Federal Reserve announced it would make SVB depositors whole, including Circle’s $3.3 billion. USDC returned to $1.00 by March 13. But the damage to confidence was done: more than 3,400 automatic liquidations triggered on DeFi lending protocols, and enterprise treasury teams suddenly understood that stablecoin infrastructure carries counterparty risk they’d never properly evaluated.

Fast forward to October 2025

Stablecoins processed $14 trillion in transactions in 2024, surpassing Visa’s payment volume. Deloitte’s latest CFO Signals survey shows 39% of CFOs at companies with $10 million or more in revenue plan to accept stablecoin payments within two years. The GENIUS Act, passed in July 2025, established the first comprehensive federal framework for stablecoin regulation, bringing banking-grade oversight to an industry that desperately needed it.

And yet, most finance leaders still don’t understand what “reserve audits” actually verify, or more importantly, what they miss.

This isn’t about crypto speculation or blockchain revolution. This is about treasury risk management for a payment infrastructure that’s becoming too significant to ignore. If you’re evaluating stablecoin adoption, or if your board is asking why you aren’t, you need to understand what happened in March 2023, what’s changed since, and what due diligence questions actually matter.

Because the next time someone pitches you on “100% backed reserves verified by monthly audits,” you’ll know exactly what that means ,and what it doesn’t.

What De-pegging Actually Means (And Why It’s Not Just Crypto Volatility)

When Bitcoin drops 15% in a day, that’s expected price discovery. When a stablecoin drops 15% in two hours, that’s a structural failure.

De-pegging occurs when a stablecoin’s market price deviates significantly from its $1.00 target peg, typically more than 2-3% sustained for over 24 hours. Unlike cryptocurrency volatility, which is feature of speculative assets, de-pegging represents a breakdown in the mechanism that’s supposed to maintain price stability.

Here’s why that matters for corporate treasury: You don’t budget for your cash equivalents to lose 13% of value over a weekend. Treasury policies treat stablecoins as functional substitutes for dollars in payment workflows,same-day settlement, minimal FX risk, consistent $1.00 valuation. When that assumption breaks, it’s not a portfolio loss. It’s an operational crisis.

The Five Triggers That Actually Cause De-pegging

Research from S&P Global, the Federal Reserve, and peer-reviewed academic studies identifies the primary failure modes:

1. Banking system failure

When your stablecoin issuer’s reserve custodian bank collapses, reserves become inaccessible, even if they exist. SVB’s failure froze $3.3 billion of Circle’s $40 billion in reserves, triggering USDC’s de-peg.

2. Reserve impairment

If the assets backing your stablecoin lose value or become illiquid, the 1:1 backing claim breaks down. This was Tether’s vulnerability in 2021, when 65% of reserves were held in commercial paper of unknown credit quality.

3. Liquidity crisis

Even with perfect reserves, if redemption requests exceed the issuer’s processing capacity, secondary market selling creates price pressure. Tether processes approximately $2 billion in daily redemptions against a $157+ billion market cap, meaning under 2% daily liquidity.

4. Loss of confidence

Transparency failures trigger panic selling before any actual reserve problem materializes. When Tether admitted in 2019 that only 74% of USDT was backed by cash equivalents, market confidence plummeted despite reserves remaining mostly intact.

5. Counterparty failure

Banking relationships severed, custody providers compromised, or payment rail access cut off, any critical dependency breaking creates redemption friction that manifests as de-pegging.

Why This Isn’t Like Crypto Volatility (And Why That Matters)

Bitcoin is designed to fluctuate. Stablecoins explicitly promise not to. That distinction has massive implications for how you evaluate risk:

- Enterprise treasury policies treat stablecoins as cash equivalents, not speculative investments.

- Accounting classification depends on stability, if value fluctuates, it may not qualify as a monetary instrument under GAAP.

- Operational planning assumes $1.00 = $1.00 when budgeting supplier payments or contractor payroll.

When USDC dropped to $0.87, companies holding $5 million in USDC for international payments suddenly had $4.35 million in purchasing power. That’s not a trading loss, it’s a cash flow crisis that could delay payroll, breach supplier contracts, or trigger covenant violations if working capital calculations included stablecoin balances.

The Cascade Effect: How One Stablecoin’s Problem Becomes Everyone’s Problem

Here’s what most CFOs miss: stablecoins are interconnected through DeFi protocols in ways that create systemic contagion risk.

When USDC de-pegged in March 2023, DAI, a $4+ billion stablecoin that was 42% collateralized by USDC, also fell to $0.96. Investors holding DAI suddenly faced exposure to Circle’s SVB problem despite never directly holding USDC.

The damage spread further: stablecoins deposited as collateral in DeFi lending protocols (Aave, Compound, MakerDAO) triggered automatic liquidations when their value dropped below minimum collateral thresholds. More than 3,400 positions were forcibly sold within hours.

Even if your company doesn’t use DeFi, these cascading liquidations create secondary market illiquidity, meaning when you need to sell your stablecoins at $1.00, there may be no buyers. You’re stuck holding a de-pegged asset until confidence restores, regardless of whether reserves are actually intact.

That’s why evaluating reserve quality isn’t just about your chosen stablecoin, it’s about understanding the entire ecosystem’s interconnected risk.

The Critical Distinction Finance Leaders Miss: Attestation ≠ Audit

Most stablecoin marketing says “audited reserves.” What they actually provide is attestations, and the difference is everything.

Here’s the gap: An attestation verifies that assets equal liabilities on a specific date. An audit examines whether the company has effective internal controls, appropriate governance, accurate financial reporting, and sustainable business practices.

Think of it this way: An attestation tells you there’s $40 billion in the vault on March 31. An audit tells you whether the company has proper processes to keep that $40 billion safe, whether they’re following stated policies, and whether their financial statements fairly represent their financial condition.

For enterprise treasury, that distinction matters because you’re not just evaluating a point-in-time balance, you’re evaluating an ongoing counterparty relationship.

What Monthly Reserve Attestations Actually Verify

Both USDC and USDT provide periodic reserve attestations from accounting firms. Here’s what those attestations cover, and what they don’t:

What’s Verified:

- Total assets equal or exceed total liabilities (stablecoins in circulation) on the attestation date

- Asset composition matches disclosed categories (cash, Treasury bills, repos, etc.)

- Assets are held in accounts under issuer’s control at named custodian banks

- No material misstatement in the reserve breakdown presented

What’s Not Verified:

- Internal control effectiveness, Are there proper segregation of duties, dual approval processes, fraud prevention systems?

- Intra-month fluctuations, Attestation is a snapshot; reserves could dip below 100% between reports

- Asset quality, A Treasury bill is listed at face value, but credit quality, counterparty exposure, and liquidation capacity aren’t assessed

- Redemption processing capacity, Do they have operational infrastructure to handle stress scenarios?

- Governance quality, Board oversight, risk management frameworks, compliance programs aren’t in scope

This isn’t a criticism of attestations, they serve an important transparency function. But they’re not a substitute for comprehensive financial audits, and treating them as equivalent creates blind spots in your risk assessment.

USDC vs. USDT: A Tale of Two Transparency Standards

Let’s get specific. Here’s what Circle (USDC) and Tether (USDT) actually provide as of October 2025:

USDC (Circle) Disclosures

- Attestation frequency: Monthly reports by Deloitte & Touche LLP (Big 4 accounting firm)

- Public disclosure cadence: Weekly reserve composition updates on Circle’s website

- Reserve structure (as of October 2025):

- ~45% held in Circle Reserve Fund (USDXX), a BlackRock-managed, SEC-registered government money market fund that invests exclusively in U.S. Treasury securities

- ~43% in overnight repurchase agreements collateralized by U.S. Treasuries

- ~12% in cash deposits at top-tier U.S. regulated banks

- Daily reporting: BlackRock publishes daily net asset value (NAV) for the USDXX fund on its public portal

- Regulatory status: GENIUS Act compliant; holds New York Department of Financial Services (NYDFS) BitLicense

- Full audit status: No publicly disclosed annual financial audit

What this means for CFOs: USDC offers best-in-class transparency among fiat-backed stablecoins. Monthly Big 4 attestations, weekly public updates, and the BlackRock-managed fund structure provide institutional-grade oversight. However, the absence of full financial audits means you’re still making an informed bet on Circle’s operational competence, not receiving comprehensive assurance.

USDT (Tether) Disclosures

- Attestation frequency: Quarterly reports by BDO Italia (top-5 accounting firm, not Big 4)

- Public disclosure cadence: Quarterly, with 30-45 day lag from quarter-end

- Reserve structure (Q2 2025):

- 84.1% in cash, cash equivalents, short-term deposits, and U.S. Treasury securities

- 15.9% in “other investments” including secured loans, corporate bonds, funds, and precious metals

- $127.5 billion in direct U.S. Treasury holdings, making Tether one of the top 18 holders globally

- Liquidity classification: 97.6% of reserves classified as liquid or near-liquid assets

- Regulatory status: Limited U.S. regulatory oversight; British Virgin Islands corporate structure

- Full audit status: Refuses full financial audits; exploring engagement with Big Four firm in 2025 under Trump administration regulatory clarity

What this means for CFOs: Tether has made significant transparency improvements since 2021, eliminating commercial paper entirely and massively increasing Treasury holdings. However, quarterly attestations (vs. monthly), non-Big 4 attestation provider, offshore structure, and continued refusal to conduct full audits create elevated due diligence requirements. The 15.9% “other investments” category also lacks granular disclosure, creating opacity around potential tail risk.

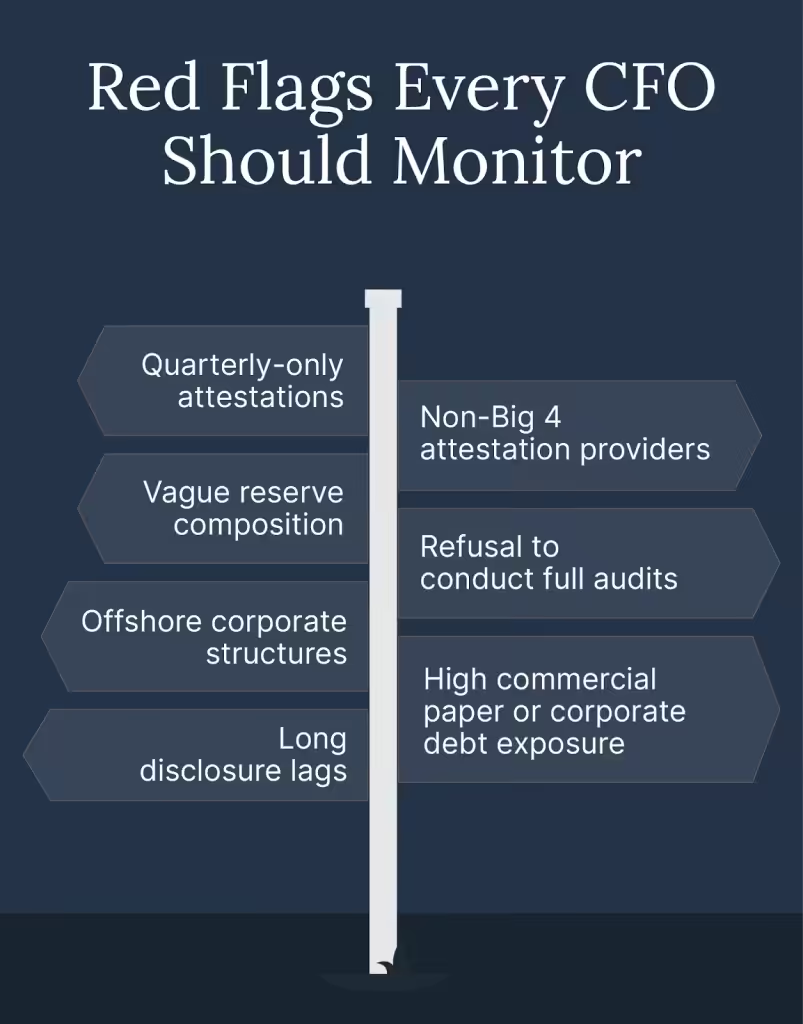

Red Flags Every CFO Should Monitor

When evaluating stablecoin reserve disclosures, watch for these warning signs:

1. Quarterly-only attestations

Monthly is the current industry best practice. Quarterly reporting increases the window for undisclosed reserve fluctuations.

2. Non-Big 4 attestation providers

While top-5 firms like BDO are credible, Big 4 firms (Deloitte, PwC, EY, KPMG) bring deeper resources, crypto-specific expertise, and reputational accountability.

3. Vague reserve composition

“Other investments” exceeding 10% of total reserves without detailed breakdown signals opacity. You need to know: secured vs. unsecured? What counterparties? What credit ratings?

4. Refusal to conduct full audits

If an issuer with $157 billion in circulation won’t submit to comprehensive financial audits, ask why. What are they protecting?

5. Offshore corporate structures

British Virgin Islands, Cayman Islands, and similar jurisdictions offer limited regulatory recourse if something goes wrong.

6. High commercial paper or corporate debt exposure

These assets become illiquid during financial stress, precisely when you need reserves to be accessible.

7. Long disclosure lags

If it’s July and you’re reading March’s attestation report, you’re making decisions on 4-month-old data.

What’s Actually Backing Your Stablecoin (And Why Composition Matters More Than You Think)

Not all “fully backed” reserves are created equal. The liquidity hierarchy of reserve assets determines how quickly issuers can process redemptions during stress, which directly impacts whether you can convert stablecoins back to fiat when you need to.

Here’s the ranking that matters:

Crisis Liquidity Performance (Best to Worst):

- Cash at regulated U.S. banks, Instant access (assuming bank is solvent)

- U.S. Treasury bills, Next-day settlement in normal markets

- Overnight repurchase agreements, Next-day unwind, collateralized by Treasuries

- Government money market funds, Next-day redemption under normal conditions

- Commercial paper, 2-90 day maturity, market-dependent liquidity

- Corporate bonds, Days to weeks to sell, highly illiquid during stress

The March 2023 lesson: Even “cash” can become temporarily inaccessible when your banking partner fails. Circle’s $3.3 billion at SVB was Category 1 (cash), theoretically the most liquid possible, but became frozen over a weekend because FDIC receivership doesn’t operate on Saturdays.

This is why reserve composition matters as much as reserve sufficiency. 100% backing with illiquid assets is a time bomb waiting for a liquidity crisis.

The GENIUS Act: What Changed in July 2025

The GENIUS Act, signed into law in July 2025, established federal reserve standards that fundamentally upgraded stablecoin risk management:

Permitted Reserve Assets:

- U.S. dollars (currency and coin)

- U.S. Treasury bills with ≤93 days to maturity

- Overnight repurchase agreements backed by U.S. Treasuries

- Demand deposits at U.S. regulated banks

- Government money market fund shares (SEC Rule 2a-7 registered)

Prohibited Assets:

- Commercial paper (eliminated Tether’s historical risk)

- Corporate bonds

- Algorithmic stabilization mechanisms

- Equity securities

- Crypto assets

Bankruptcy Protection Innovation:

The Act requires reserves to be held in segregated, bankruptcy-remote accounts. If a stablecoin issuer fails, holder claims receive super-priority status, ranked above administrative expenses in bankruptcy proceedings. Reserves must be distributed ratably to holders within 14 days.

CFO translation: If Circle or Tether goes bankrupt tomorrow, your stablecoin holdings aren’t trapped in years of bankruptcy court. You’re first in line for recovery, and distribution happens in two weeks, not two years.

This is a massive improvement over March 2023, when it wasn’t clear whether USDC holders had any legal claim on reserves or would be treated as unsecured creditors.

USDC’s BlackRock Advantage: What the Circle Reserve Fund Actually Means

In response to the SVB crisis, Circle restructured how it holds reserves. Approximately 45% of USDC backing now sits in the Circle Reserve Fund (ticker: USDXX), a government money market fund managed by BlackRock.

Here’s why that matters:

SEC Regulatory Oversight

USDXX is registered under the Investment Company Act of 1940 and complies with SEC Rule 2a-7, which governs money market funds. This subjects it to daily portfolio diversification requirements, maturity restrictions, and credit quality standards.

Daily Liquidity Reporting

BlackRock publishes daily net asset value (NAV), portfolio holdings, and maturity profiles on its public website. You get real-time transparency into nearly half of USDC’s reserves.

Institutional Custody

Assets are held by State Street Bank as custodian, adding an additional layer of institutional-grade asset protection.

Diversification

Instead of concentrating cash at 2-3 banks (SVB risk), the fund spreads investments across dozens of U.S. Treasury securities and overnight repos, eliminating single-point-of-failure banking risk.

CFO takeaway: The USDXX structure means 45% of USDC reserves operate under the same regulatory framework as corporate treasury money market funds you already use. That’s bank-grade oversight, not crypto-native self-regulation.

Tether’s Evolution: From Commercial Paper to Treasury Dominance

Tether’s reserve journey illustrates how transparency pressure drives behavior change, even without regulatory mandate.

2019: Tether admits only 74% of USDT backed by cash equivalents; remainder in loans and receivables of undisclosed nature.

2021: 65% of reserves held in commercial paper, short-term corporate debt. Tether refuses to disclose which companies issued the paper, raising concerns about credit quality and Chinese counterparty exposure.

2022: Following sustained market pressure, Tether commits to eliminating commercial paper. By October 2022, commercial paper holdings reach zero.

2025: $127.5 billion in U.S. Treasury holdings makes Tether one of the largest sovereign debt holders globally, ranking alongside major nations. Q2 2025 attestation shows 84.1% in cash/Treasuries/equivalents.

The arc is clear: Market discipline and transparency demands forced Tether from opacity to disclosure, from risky commercial paper to ultra-safe Treasuries. But the refusal to conduct full audits remains a lingering credibility gap.

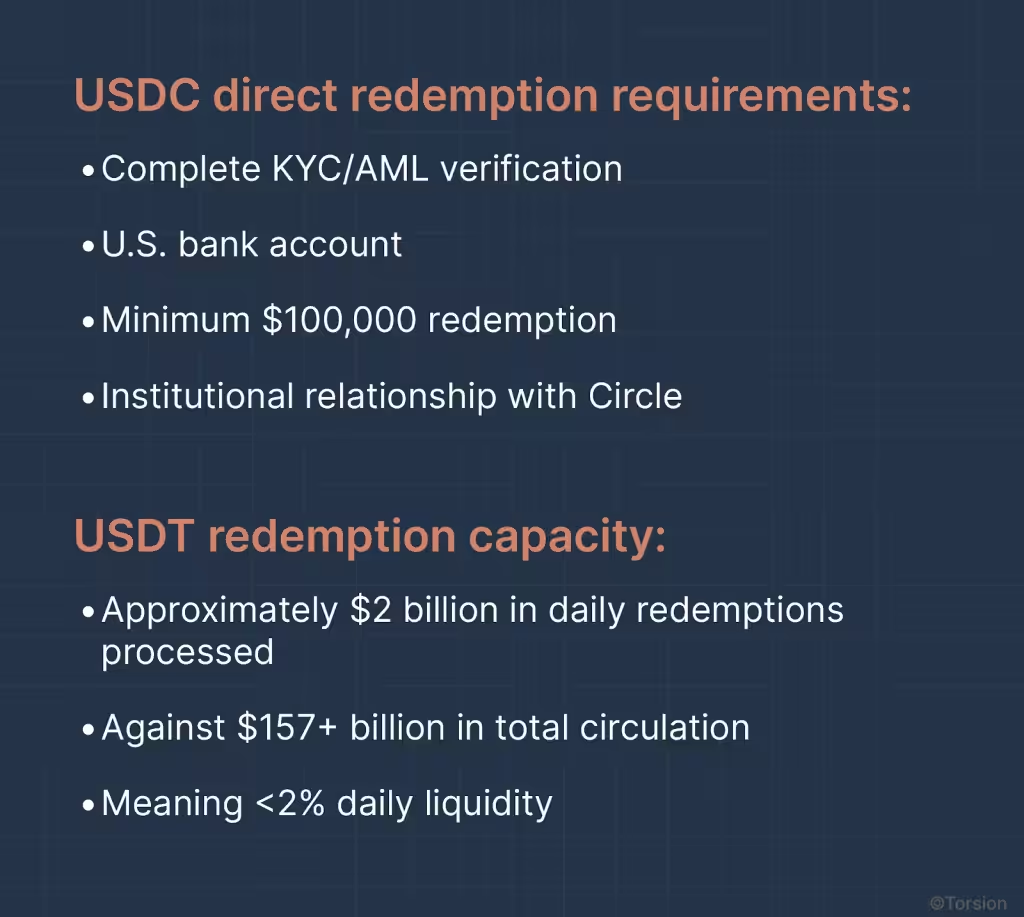

The Redemption Capacity Problem Nobody Talks About

Here’s the uncomfortable truth: even with perfect reserves, you may not be able to redeem stablecoins directly.

What this means: If you’re a mid-market company holding $500,000 in USDC for supplier payments, you likely cannot redeem directly with Circle. You’re dependent on secondary market liquidity, selling to institutional arbitrageurs on Coinbase, Kraken, or OTC desks.

During the March 2023 de-peg, that secondary market dried up. Buyers disappeared. Even though Circle continued processing direct redemptions at $1.00 for qualified institutions, most holders were forced to sell at $0.87-$0.92 because they lacked direct access.

Risk mitigation: Torsion’s infrastructure solves this by maintaining relationships with institutional liquidity providers and direct issuer redemption access, ensuring you can convert to fiat at prevailing rates even during stress, without building that capability in-house.

The CFO Due Diligence Checklist: 7 Questions That Actually Matter

Before integrating stablecoin payment infrastructure, your vendor evaluation needs to cover these dimensions. Guessing wrong costs you credibility with the board, and potentially millions in trapped liquidity.

1. Issuer Financial Health & Transparency

Questions to ask your infrastructure partner:

- What’s the attestation frequency for the stablecoin we’d be using? (Monthly is current best practice)

- Which accounting firm provides attestations? (Big 4 strongly preferred)

- How often is reserve composition publicly disclosed? (Weekly for USDC, quarterly for USDT)

- Has a full financial audit been conducted? If not, why? (Red flag if the answer is vague)

- What regulatory licenses does the issuer hold? (NYDFS, OCC, state money transmitter licenses)

Documentation you need:

- Last 6 months of attestation reports (not just the latest)

- Reserve composition breakdown by asset type and maturity

- Regulatory filings, if publicly available

- Banking partner disclosure (which banks custody the reserves?)

Red flags that should pause your evaluation:

- Quarterly-only attestations when monthly is standard

- Refusal to name banking partners or custody providers

- “Other investments” >10% without detailed breakdown

- History of reserve composition misstatements (Tether 2019-2021)

- Offshore corporate structure with limited regulatory oversight

How Torsion helps: We monitor USDC and USDT reserve attestations monthly and alert clients to composition changes that increase risk exposure. You shouldn’t need a crypto analyst on staff to track whether Tether’s commercial paper holdings are creeping back up.

2. Banking & Custody Partner Risk

The SVB lesson was clear: your stablecoin is only as reliable as the banks holding its reserves.

Questions to ask:

- Which banks custody the reserve assets? (Transparency is key)

- Are reserves held at multiple institutions, or concentrated at 1-2 banks? (Diversification reduces single-point-of-failure risk)

- What’s the custody provider’s regulatory status? (U.S. banking charter or trust company license preferred)

- Are reserves held in segregated, bankruptcy-remote accounts per GENIUS Act requirements?

- What happens to reserves if a custody bank fails? (SVB scenario planning)

March 2023 context: Circle held 8% of USDC reserves at SVB. When the bank failed Friday afternoon, those funds became inaccessible over the weekend, triggering the de-peg before FDIC could make depositors whole on Monday.

Best practice: Issuers should spread reserves across 5+ top-tier banks and publicly disclose concentration risk. Circle has since diversified banking relationships; Tether’s banking partners remain largely undisclosed.

How Torsion helps: Our infrastructure partners use institutional-grade custody (Fireblocks, Anchorage Digital) with bank-level security, insurance, and regulatory oversight. We’ve done the custody due diligence so your treasury team doesn’t have to become experts in multi-party computation (MPC) wallet security.

3. Redemption Mechanics & Capacity

Questions that reveal operational risk:

- Can our company redeem directly with the issuer, or only through secondary markets?

- What are the KYC/onboarding requirements for direct redemption access?

- What’s the issuer’s stated daily redemption capacity? (Tether: ~$2B daily vs. $157B outstanding)

- What’s the historical redemption processing time? (Target: same-day or T+1)

- Have redemptions ever been suspended? Under what circumstances?

The uncomfortable truth: Tether processes about $2 billion in daily redemptions against $157+ billion in circulation, meaning less than 2% daily liquidity. If 5% of holders tried to redeem simultaneously during a panic, processing would take multiple days.

USDC has higher relative capacity, but most corporate users still can’t access direct redemption due to $100K minimums and institutional relationship requirements.

Secondary market dependency: During March 2023, even though Circle continued processing $1.00 redemptions for qualified institutions, retail and mid-market users were forced to sell at $0.87-$0.92 on exchanges because they lacked direct access.

How Torsion helps: We maintain institutional liquidity provider relationships and direct issuer redemption access. When you need to convert stablecoins to fiat, whether for $50K or $5M, settlement happens at prevailing rates without you building those relationships individually.

4. Regulatory Compliance Status

The July 2025 GENIUS Act changed everything. Now you need to verify compliance, not just assume it.

Questions to ask:

- Is the issuer GENIUS Act compliant (U.S.) or MiCA authorized (EU)?

- Does the issuer file monthly reserve disclosures with regulators?

- What AML/KYC program is in place for transaction monitoring?

- How are OFAC sanctions screening handled?

- Is the issuer subject to federal banking supervision or state trust company regulations?

GENIUS Act requirements (July 2025):

- Monthly attestations mandatory (not just voluntary)

- Reserve composition restrictions (no commercial paper or algorithmic mechanisms)

- Federal banking charter or state trust company license required

- Segregated reserve accounts with super-priority creditor status for holders

- Monthly reporting to Federal Reserve or OCC

MiCA requirements (EU, June 2024):

- 1:1 backing with high-quality liquid assets

- Redemption at par value (€1.00) guaranteed at any time

- Significant token designation if >10M users or €5B market cap triggers additional capital requirements

- Daily reserve monitoring and public disclosure

How Torsion helps: We track regulatory changes across jurisdictions (U.S., EU, UK, Singapore) and ensure our payment infrastructure remains compliant as rules evolve. When MiCA added new disclosure requirements in June 2024, our clients didn’t need to retrofit their processes, we handled it.

5. Integration & Operational Risk

Questions that reveal hidden implementation costs:

- Which custody platforms support this stablecoin? (Fireblocks, Anchorage, BitGo are institutional-grade)

- What API uptime SLAs are provided? (99.9% minimum for payment-critical infrastructure)

- How is transaction monitoring handled for suspicious activity reporting?

- What disaster recovery and business continuity plans exist?

- Can transactions be reversed if sent to the wrong address? (No, blockchain is immutable; plan for human error)

The integration trap: Stablecoin APIs don’t natively connect to NetSuite, SAP, QuickBooks, or Xero. Without middleware, your accounting team is manually copying blockchain transaction IDs into spreadsheets for month-end reconciliation.

The custody trap: If you self-custody stablecoins (manage private keys in-house), you’re responsible for security, disaster recovery, and key management. One compromised laptop = complete loss of funds. Zero reversibility.

How Torsion helps: REST API integration with existing payment systems. Automated reconciliation. Monthly reports formatted for your accounting team. Your treasury staff never touches crypto infrastructure directly, they interact with familiar payment workflows that happen to settle via stablecoins under the hood.

6. Accounting & Tax Treatment

This is where finance leaders get surprised: stablecoin accounting is more complex than “it’s worth $1, so treat it like cash.”

Questions your controller will ask:

- How should stablecoins be classified on the balance sheet? (Cash equivalent vs. intangible asset)

- Are FX gains/losses recognized if value fluctuates from $1.00?

- What tax reporting automation is available (1099 generation, cost basis tracking)?

- Does the solution integrate with our existing treasury management system (TMS)?

The accounting challenge:

FASB hasn’t issued stablecoin-specific guidance. The GENIUS Act doesn’t address accounting classification. Under current GAAP, most enterprises must treat stablecoins as indefinite-lived intangible assets (like domain names), not cash or cash equivalents, even though they function like cash in payment workflows.

This means:

- Fair value measurement required at each reporting period (even for stable $1.00 assets)

- Potential P&L volatility from mark-to-market adjustments

- Cannot be included in “cash and cash equivalents” line item for ratio calculations

How Torsion helps: We provide accounting classification guidance, automated transaction tagging by business purpose, and monthly close documentation formatted for external auditors. If your company treats stablecoins as intangible assets, our reporting shows acquisition date, carrying value, and fair value adjustments, exactly what Grant Thornton or Deloitte needs to see.

7. Historical Stress Performance

Past behavior predicts future behavior. How did this stablecoin perform when tested?

Questions to ask:

- Has this stablecoin ever de-pegged? When, why, severity, duration?

- How did the issuer respond during the crisis? (Communication speed, transparency, remediation)

- Were reserves fully maintained throughout the stress event?

- Were redemptions processed normally, or were there delays/suspensions?

USDC track record:

- March 2023: De-pegged to $0.87 due to SVB exposure; recovered in 3 days after federal intervention

- No other significant de-pegs since launch in 2018

- Redemptions continued during crisis (though at discount on secondary market for non-institutional users)

- Circle disclosed issue within hours and maintained transparent communication throughout

USDT track record:

- No major de-pegging events since 2017 (brief dips to $0.99-$0.98 during market stress, but nothing sustained)

- Transparency controversies 2019-2021 created confidence issues, but peg held

- Sustained periods trading $0.99-$1.01 (within acceptable range for fiat-backed stablecoins)

The 3-year milestone: Both USDC and USDT have now gone 2.5+ years since March 2023 without major de-pegging, despite multiple regional bank failures (First Republic, Signature), crypto exchange collapses, and market volatility. That’s a meaningful stress test passed.

How Torsion helps: We monitor real-time de-pegging indicators (secondary market pricing, on-chain redemption volumes, reserve attestation anomalies) and alert clients when risk metrics shift. You’re not checking CoinGecko every morning, we’re doing that.

Risk Mitigation: What to Do When You Decide to Move Forward

Due diligence complete. The board is interested. The CEO is asking for a pilot. Now what?

Set Exposure Limits That Protect the Business

Initial adoption framework:

- Limit stablecoin holdings to <5% of liquid assets during the first 6 months

- Structure for velocity, not volume, Optimize for high transaction throughput but low end-of-day balances

- Same-day conversion policy, Treasury rule: convert stablecoin receipts to fiat daily or weekly to minimize exposure time

- Maintain traditional payment backup, Don’t route mission-critical vendor payments exclusively through stablecoins until you’ve tested for 90+ days

Issuer diversification:

If using both USDC and USDT, understand you haven’t eliminated correlation risk, both are vulnerable to the same regulatory changes, banking system stress, and market confidence dynamics. True diversification means maintaining SWIFT/ACH/wire capabilities in parallel.

Stress testing your exposure:

Model this scenario: stablecoin de-pegs to $0.85 for 72 hours. At your current payment volumes, what’s the maximum loss exposure? Can you absorb that without breaching covenants, missing payroll, or delaying supplier payments? If not, your exposure is too high.

Build Monitoring & Governance Protocols

Monthly treasury review checklist:

- Examine latest reserve attestation report (typically available 15-30 days after month-end)

- Track reserve composition shifts, Set alerts if Treasury holdings drop >10% or “other investments” increase >5%

- Monitor real-time de-pegging indicators, Daily spot price via CoinGecko/CoinMarketCap; threshold alert if >2% deviation for >24 hours

- Review issuer regulatory status, Has NYDFS, OCC, or SEC issued any enforcement actions or guidance changes?

Threshold-based escalation:

- De-peg >2% for >24 hours → Escalate to CFO; prepare to cease new stablecoin-denominated payments

- Reserve composition shift toward illiquid assets → Schedule vendor review call; assess whether to reduce exposure

- Attestation report delay >45 days → Red flag; activate contingency planning

- Regulatory enforcement action against issuer → Immediate executive review; consider pausing usage pending resolution

Audit trail for external auditors:

- Blockchain transaction IDs for all payments (immutable proof of settlement)

- Monthly reconciliation against on-chain data (Etherscan, blockchain explorers)

- Business purpose documentation for each transaction (vendor invoice, contractor agreement)

- Screenshots of market prices at transaction time (FX rate evidence for accounting)

How Torsion helps: We provide monthly risk summary reports highlighting attestation changes, composition shifts, and regulatory updates, formatted for CFO review in under 5 minutes. You’re not building this monitoring infrastructure from scratch.

Negotiate Contractual Protections

With your infrastructure partner/custody provider:

- SLA for redemption processing, Target: same business day for conversions to fiat

- Liability provisions, Define responsibility for losses during de-pegging events (expect caps; negotiate best available)

- Data portability, Ability to switch providers with 30-day notice and full transaction history export

- Insurance coverage, Rare for stablecoin infrastructure, but emerging for enterprise clients; negotiate if available

- Termination rights, If stablecoin de-pegs >5% for >48 hours, you can exit without penalty

With suppliers accepting stablecoins:

- Price denomination in fiat USD, Not stablecoin units; avoids disputes if value fluctuates

- 24-hour acceptance window, Supplier must acknowledge payment receipt within 24 hours (locks in value)

- Alternative payment method defined, If stablecoin infrastructure unavailable, revert to wire transfer with X-day notice

Establish Internal Controls

Your treasury policy should specify:

Approved use cases:

- ✅ Cross-border supplier payments where SWIFT is slow/expensive

- ✅ Contractor payroll in jurisdictions with limited banking access

- ✅ Just-in-time payments requiring same-day settlement

- ❌ Long-term cash reserves or store of value

- ❌ Speculative trading or yield farming

- ❌ Any transaction where reversibility might be needed (dispute risk)

Dual approval requirements:

Stablecoin transactions exceeding $50,000 require two authorized signers, same standard as wire transfers.

Wallet custody:

Corporate stablecoin wallets must be managed through institutional custody providers (Fireblocks, Anchorage), never individual employee devices or browser-based wallets.

Private key management:

Hardware security module (HSM) or multi-party computation (MPC) custody required, no single person can move funds.

Reconciliation frequency:

Daily for transaction activity. Monthly for balance verification against on-chain data.

Compliance documentation:

- Maintain travel rule data (sender/recipient identifying information) for transactions >$3,000

- AML/KYC records for all counterparties receiving payments

- OFAC sanctions screening evidence (automated through infrastructure partner)

- Tax reporting documentation (Form 1099 equivalent for contractor payments)

How Torsion helps: Our platform enforces these controls automatically, dual approval workflows, sanctions screening, transaction monitoring, so you’re not building compliance infrastructure from scratch.

What Changed After March 2023 (And What Hasn’t)

The stablecoin landscape in October 2025 is fundamentally different from March 2023. But pockets of risk remain.

The Regulatory Transformation

GENIUS Act (U.S., July 2025)

First comprehensive federal stablecoin framework. Monthly attestations are now legally required, not voluntary. Reserve composition is restricted to ultra-liquid, high-quality assets. Issuers must hold federal banking charters or state trust company licenses. Most importantly: bankruptcy-remote segregation with super-priority creditor status for stablecoin holders means if your issuer fails, you’re first in line for recovery within 14 days.

MiCA (EU, fully operational June 2024)

E-money token (EMT) framework for fiat-backed stablecoins. 1:1 redemption at par value is legally guaranteed, not just promised. Issuers exceeding 10 million users or €5 billion market cap receive “significant token” designation, triggering additional capital requirements and daily regulatory monitoring.

Net effect: Stablecoins now operate under banking-grade regulatory oversight in the world’s two largest economic blocs. This is not the “Wild West” anymore.

Issuer Evolution Since the Crisis

Circle (USDC) improvements:

- Moved reserves to BlackRock-managed Circle Reserve Fund (USDXX), bringing SEC oversight and daily reporting

- Increased disclosure frequency from monthly to weekly for reserve composition

- Diversified banking relationships beyond 2-3 major banks

- Achieved full GENIUS Act compliance immediately upon passage (July 2025)

Tether (USDT) improvements:

- Eliminated commercial paper entirely, zero as of October 2022 (down from 65% in 2021)

- Increased U.S. Treasury holdings to $127.5 billion, ranking among the world’s largest sovereign debt holders

- Reduced attestation lag time from 90+ days to 30-45 days

- Exploring Big Four audit engagement in 2025 under Trump administration regulatory clarity

The arc is clear: Both major issuers responded to March 2023 by increasing transparency, improving reserve quality, and reducing counterparty concentration risk.

What Hasn’t Changed: Remaining Risk Gaps

Tether’s transparency ceiling

Despite improvements, Tether still refuses full financial audits, providing only quarterly attestations from BDO Italia. The 15.9% “other investments” category lacks granular disclosure. Offshore corporate structure (British Virgin Islands) limits regulatory recourse if problems emerge.

Redemption bottlenecks persist

Retail and mid-market users still cannot redeem directly with issuers in most cases. You’re dependent on secondary market liquidity via exchanges and OTC desks. During stress events, that liquidity can evaporate, leaving you stuck selling at discounts.

Accounting ambiguity unresolved

FASB has not issued stablecoin-specific guidance. The GENIUS Act doesn’t address accounting classification. CFOs are left navigating whether stablecoins are cash equivalents (preferred for treasury operations) or intangible assets (current GAAP interpretation).

The positive milestone: No major de-pegging events in 2.5+ years, despite First Republic and Signature Bank failures, Binance regulatory issues, and significant crypto market volatility. Both USDC and USDT have been stress-tested under real-world banking system failures and held the peg.

When Stablecoins Make Sense for Your Treasury (And When to Wait)

Not every company should adopt stablecoin infrastructure tomorrow. Here’s the decision framework.

Use Cases Where Benefits Outweigh Risks

Strong candidates for stablecoin adoption:

Cross-border B2B payments

1-hour settlement vs. 3-5 days for SWIFT. Cost reduction of 40-60% compared to traditional correspondent banking fees. If you’re paying suppliers in Latin America, Southeast Asia, or Africa where SWIFT infrastructure is expensive and slow, stablecoins offer tangible ROI.

Emerging market expansion

Access countries where traditional payment processors (Visa, Mastercard, PayPal) decline to operate due to sanctions risk, banking infrastructure limitations, or fraud concerns. Stablecoins operate on censorship-resistant rails.

Contractor and freelancer payments

Real-time settlement, lower per-transaction fees than PayPal or Wise (formerly TransferWise). Especially valuable for global remote workforces paid weekly or bi-weekly.

24/7 treasury operations

No weekend or holiday blackout periods. If your business operates globally and needs to process payments outside U.S. banking hours, stablecoins don’t sleep.

Payment processor diversification

Backup payment rail when Visa/Mastercard decline high-risk merchant categories, or when geopolitical sanctions block traditional banking access to specific regions.

Not Recommended For

Long-term cash reserves

Stablecoins lack FDIC insurance, carry counterparty risk, and create accounting complexity. They’re payment rails, not savings accounts.

Speculative investment or yield generation

Outside the treasury mandate. If someone pitches you on “staking USDC for 5% APY,” you’re taking on DeFi protocol risk that audit committees won’t approve.

Payroll to W-2 employees

Regulatory and tax complexity. Most U.S. employees expect direct deposit in USD to checking accounts, not stablecoins to crypto wallets. Contractor 1099 payments are different, those work well.

Any use case requiring reversibility

Blockchain transactions are immutable. If you send $500,000 to the wrong wallet address, there’s no “stop payment” function. Plan for human error through dual approval and address whitelisting.

When to Wait

Hold off on stablecoin adoption if:

- Treasury policy explicitly prohibits crypto-adjacent assets, Fix the policy first; don’t work around it

- Accounting/audit team lacks digital asset expertise, You’ll create month-end close chaos without proper guidance

- Payment volume is too small to justify integration cost, If you’re processing <$1M monthly in international payments, ROI may not be there yet

- Suppliers/vendors have no capability to receive stablecoins, You need counterparties who can accept them; adoption is growing but not universal

- Regulatory status in your jurisdiction remains unclear, GENIUS Act covers U.S.; MiCA covers EU; other regions may still be evolving

The Torsion Value Proposition: Abstraction at the Integration Layer

Here’s the core problem: Enterprise finance teams need stablecoin payment efficiency but lack the specialized expertise to safely adopt crypto infrastructure.

That’s the gap Torsion fills.

How we handle complexity so you don’t have to:

Infrastructure layer: Pre-vetted custody partners (Fireblocks, Anchorage Digital) with institutional-grade security, insurance, and regulatory oversight. You’re not evaluating 50+ wallet providers or comparing MPC vs. HSM custody models.

Compliance automation: AML/KYC verification, OFAC sanctions screening, travel rule reporting for transactions >$3K. You’re not building a compliance team that understands both treasury operations and blockchain analytics.

Accounting integration: Transaction tagging by business purpose, automated month-end reconciliation, audit trail documentation formatted for external auditors. Your controller isn’t learning Etherscan to verify on-chain settlement.

Risk management: Monthly reserve attestation monitoring, real-time de-pegging alerts, regulatory change tracking across jurisdictions. Your treasury team isn’t becoming crypto analysts.

Payment automation: REST API integration with NetSuite, SAP, QuickBooks, Xero. Direct fiat on/off ramps for USD ↔ stablecoin conversion.