Key Takeaways

- GENIUS Act (July 2025) and MiCA (December 2024) ended regulatory uncertainty, CFOs can now implement stablecoin infrastructure without compliance ambiguity

- 54% of companies plan stablecoin adoption within 6-12 months (post-GENIUS Act), regulatory clarity accelerated enterprise implementation from “wait and see” to active deployment

- Core requirements align across frameworks: 1:1 reserve backing, monthly audits, algorithmic ban, redemption rights, both U.S. and EU standards protect consumers while enabling enterprise use

- Most CFOs are users, not issuers, standard BSA/AML compliance applies (same as wire transfers), no stablecoin license required

- CEO/CFO certification carries criminal liability: Up to 20 years imprisonment and $5M fine for false reserve certification under GENIUS Act, making audit-ready infrastructure non-negotiable

- Implementation deadline: January 2027 (or 120 days after Treasury issues final regulations), 15-month window creates urgency for Q4 2025/Q1 2026 implementation

- Torsion provides GENIUS Act + MiCA compliance built-in: 2-4 week implementation with BSA/AML infrastructure, monthly compliance reporting, and SOC 2 certification, treasury teams never touch crypto infrastructure directly

June 15, 2025. A manufacturing CFO presents to the board. The question comes up: “Should we implement stablecoin payments for international suppliers?”

The answer: “Regulatory uncertainty makes this premature. We’re monitoring developments.”

October 20, 2025. Same CFO, same board, different conversation.

The question: “Why aren’t we implementing stablecoin payments when competitors are?”

What changed in 90 days? July 18, 2025, the GENIUS Act passed with bipartisan support (Senate 68-30, House 308-122). For the first time since stablecoins emerged, U.S. companies could implement payment infrastructure without regulatory ambiguity.

The data confirms the shift: 54% of companies now plan stablecoin adoption within 6-12 months, up from single digits pre-regulation. Stablecoins processed $14 trillion in 2024, surpassing Visa. The cross-border payment opportunity: $2.1-4.2 trillion by 2030.

The European Union moved first. MiCA (Markets in Crypto-Assets) became fully applicable December 30, 2024. The United States followed seven months later. Together, these frameworks ended the “wait and see” era.

This isn’t about whether stablecoins have business value, 41% of current users report 10%+ cost reduction on international transactions. This is about understanding the regulatory requirements that make compliant implementation possible, and why the companies moving in Q4 2025 will capture advantages competitors spend 2026 chasing.

The $45 Billion Lesson That Changed Everything

Before examining what GENIUS Act and MiCA require, we need to understand why they exist.

May 2022. TerraUSD (UST), an algorithmic stablecoin with a $45 billion market cap, collapsed in one week. The mechanism was elegant in theory: UST maintained its $1 peg through a sister token, LUNA, with no reserve backing. When confidence broke and UST dropped below $1, the algorithm created trillions of LUNA tokens to restore the peg. Both crashed to zero.

The damage: $45 billion wiped out, investors ruined, the entire crypto market shaken.

The response: Regulators in the U.S. and EU realized algorithmic designs created systemic risk without consumer protection. The solution wasn’t to ban stablecoins, it was to require reserve backing, monthly audits, and federal oversight.

Terra/Luna’s collapse catalyzed the regulatory frameworks that make enterprise adoption possible today. Both GENIUS Act and MiCA explicitly ban algorithmic stablecoins. Only fiat-backed stablecoins with audited 1:1 reserve backing qualify under either framework.

GENIUS Act: What the U.S. Framework Actually Requires

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins) creates a federal framework for payment stablecoin regulation. Here’s what it actually mandates, not summaries, but specific requirements.

Defining “Payment Stablecoins” (and What Doesn’t Qualify)

The law defines a payment stablecoin as a digital asset that:

- Is designed to maintain stable value relative to a fixed amount of monetary value

- Is issued by an institution subject to federal or state supervision

- Is redeemable on demand for face value in dollars

- Functions primarily as a means of payment or settlement

What this excludes:

- Algorithmic stablecoins (no reserve backing)

- Crypto assets designed as investments

- Stablecoins that pay interest to holders

- Securities or commodities under SEC/CFTC jurisdiction

Translation for CFOs: Compliant stablecoins are regulated payment instruments, more like wire transfers or ACH, less like securities. This matters because it determines which regulators have jurisdiction and what compliance obligations apply.

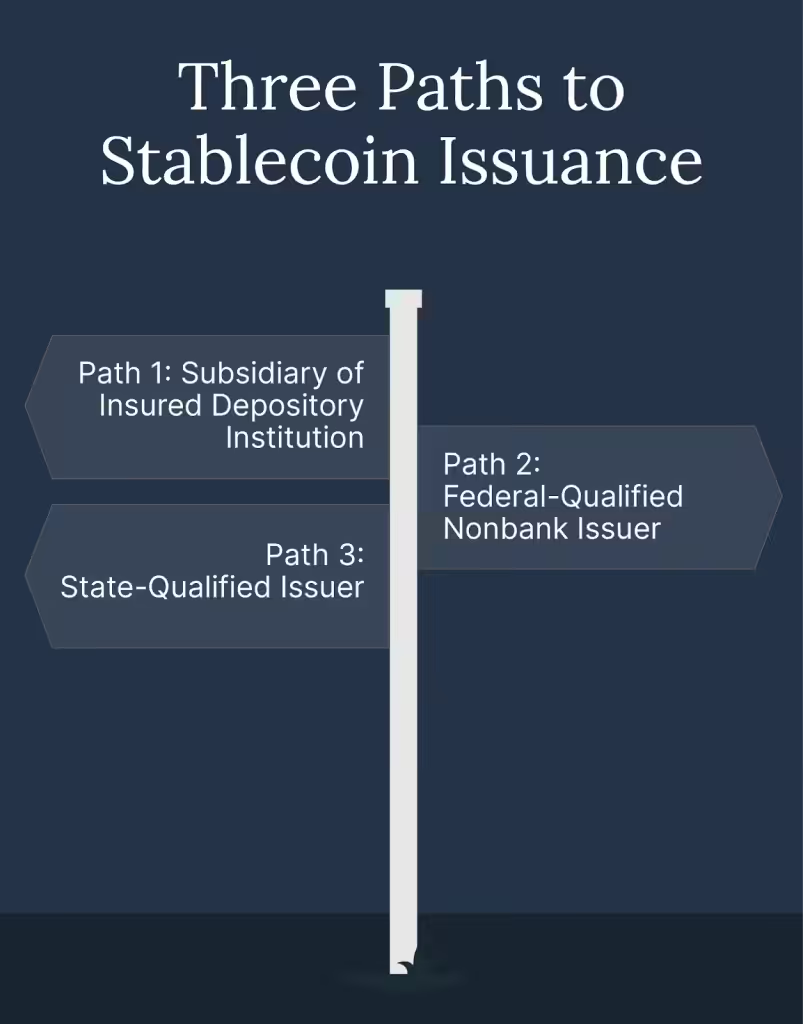

Three Paths to Stablecoin Issuance

The GENIUS Act creates three licensing options for stablecoin issuers:

Path 1: Subsidiary of Insured Depository Institution

- Banks and credit unions can issue stablecoins through subsidiaries

- Subject to primary federal banking regulator oversight (OCC, Federal Reserve, FDIC)

- Inherits existing regulatory infrastructure and capital requirements

Path 2: Federal-Qualified Nonbank Issuer

- Direct OCC oversight as payment stablecoin issuer

- Must meet capital, liquidity, and operational requirements comparable to banks

- Example: Stripe’s pending OCC national bank charter application

Path 3: State-Qualified Issuer

- State money transmitter licensing initially

- Must “graduate” to federal oversight if circulation exceeds $10 billion

- Provides path for smaller issuers to enter market with state-level compliance

What matters for enterprise treasury teams: You’re almost certainly users, not issuers. You don’t need a stablecoin license. You need infrastructure that connects to compliant issuers while maintaining standard BSA/AML controls your treasury already operates.

Reserve Requirements: The Core Protection

This is where the Terra/Luna lesson gets codified into federal law:

1:1 Reserve Backing

- Every payment stablecoin must be backed by reserves equal to 100% of outstanding stablecoins

- Permitted reserve assets:

- Physical U.S. currency

- Federal Reserve balances

- U.S. Treasury bills (short-term only, no longer maturity bonds)

- Repurchase agreements backed by U.S. government securities

- Other low-risk, highly liquid assets approved by regulators

Monthly Third-Party Audits

- Registered public accounting firms must examine reserves monthly

- Audits must verify reserve adequacy, composition, and segregation

- Results publicly disclosed

CEO/CFO Certification Requirement

- Chief executive and financial officers must personally certify reserve accuracy

- Liability exposure: False certification carries criminal penalties up to 20 years imprisonment and $5 million fine

- This personal accountability provision makes CFOs extremely cautious about infrastructure partners

Bankruptcy Protection

- Stablecoin holders have priority claim on reserve assets if issuer fails

- Reserves held in segregated, bankruptcy-remote structure

- Redemption at par ($1 per stablecoin) on demand

The GENIUS Act treats reserve accuracy as a CEO/CFO certification matter, with criminal penalties for false disclosure. This makes audit-ready infrastructure non-negotiable for enterprise adoption.

Compliance Obligations for Infrastructure Partners

If you’re using stablecoins (not issuing them), your compliance requirements are standard banking controls:

Bank Secrecy Act (BSA) Compliance

- Full AML/CFT (Anti-Money Laundering / Countering Financing of Terrorism) obligations

- Customer identification programs (KYC)

- Transaction monitoring for suspicious activity

- Suspicious Activity Reports (SARs) when thresholds trigger

Sanctions Compliance

- Must maintain ability to freeze/seize stablecoins pursuant to court orders or OFAC sanctions

- Real-time screening against sanctions lists

Monthly Public Disclosures

- Issuers must disclose reserve composition and total stablecoins outstanding

- Enterprise users benefit from this transparency, you can verify backing monthly

What Torsion Handles:

Standard BSA/AML infrastructure through Chainalysis and TRM Labs integration, automated transaction monitoring, suspicious activity reporting, and monthly compliance documentation. Your treasury team continues using familiar workflows, the infrastructure handles crypto-specific compliance invisibly.

Implementation Timeline: The 15-Month Window

Here’s the critical timing:

Effective Date: Earlier of:

- January 18, 2027 (18 months after enactment), OR

- 120 days after Treasury Department issues implementing regulations

Service Provider Deadline:

- Digital asset exchanges and custodians have until July 18, 2028 to restrict offerings to GENIUS Act-compliant stablecoins only

Current Status (October 2025):

- Treasury Department issued notice of proposed rulemaking September 2025

- Public comment period open through October 17, 2025

- Final regulations expected Q1-Q2 2026

- Practical implication: Companies can implement now with compliant infrastructure

Why timing matters: 54% of companies plan adoption within 6-12 months. Those implementing Q4 2025/Q1 2026 capture cost savings and competitive positioning before the January 2027 rush.

MiCA: Europe’s Comprehensive Crypto Framework

While the GENIUS Act focuses narrowly on payment stablecoins, MiCA (Markets in Crypto-Assets) takes a broader approach, regulating all crypto assets, not just stablecoins.

Scope and Timeline (Europe Moved First)

Fully Applicable: December 30, 2024

- MiCA became enforceable seven months before GENIUS Act passed

- This created first-mover advantage for EU-based stablecoin issuers

What MiCA Regulates:

- Stablecoins (two categories: E-Money Tokens and Asset-Referenced Tokens)

- Crypto assets more broadly (utility tokens, governance tokens)

- Crypto Asset Service Providers (CASPs) like exchanges and custodians

The Two Stablecoin Categories:

- E-Money Tokens (EMTs): Fiat currency-pegged (USDC, USDT equivalents)

- Asset-Referenced Tokens (ARTs): Pegged to basket of assets or commodities

For enterprise payment use cases, EMTs are the relevant category.

Core Requirements for Stablecoin Issuers Under MiCA

Authorization Process

- Must obtain European Banking Authority (EBA) authorization before launching

- Non-EU issuers must establish EU legal entity with full regulatory compliance

- Market reality: 100% of new stablecoin projects need licensing as of 2025

Reserve Standards

- 100% liquid reserves matching circulating supply

- At least 30% in highly liquid assets (narrower than GENIUS Act)

- Reserves held in EU financial institutions (geographic sovereignty requirement)

- Quarterly audited reports with 95% minimum audit coverage

Redemption Rights

- Face value redemption on demand

- No interest payments to holders (distinguishes from deposit-taking)

- Protects consumers from issuer default risk

Operational Restrictions

- €200 million daily transaction cap per issuer for systemically important stablecoins

- This cap doesn’t exist under GENIUS Act

The Compliance Reality: Stricter Than Expected

MiCA’s implementation revealed higher barriers than many anticipated:

Application Rejection Rate: 45%

- Nearly half of stablecoin issuer applications rejected due to strict standards (2025 data)

Reclassification Requirement: 78%

- Over three-quarters of stablecoins in EU circulation require structural changes to comply

Current Compliance: Only 21%

- Just one-fifth of existing projects satisfied full MiCA requirements as of early 2025

Penalties for Non-Compliance

- €5 million or 5% of annual turnover, whichever is higher

MiCA-Compliant Stablecoins (Early Market Leaders)

- EUROe (Membrane Finance): First officially licensed euro stablecoin, Finnish FSA supervision

- EURC (Circle): Euro-backed sibling to USDC

- Monerium EUR: E-money token with EU license, programmable finance focus

- Anchored Euro (AEUR): Swiss-based, institutional backing

MiCA’s stricter standards created higher issuer compliance costs but clearer market structure for enterprise users. The EU stablecoin market is projected to grow 37% in 2025, reaching €450 billion, but only compliant issuers capture that opportunity.

What This Means for Multinational CFOs:

If your organization operates across U.S. and EU markets, compliance with both frameworks is required. The good news: core requirements align. The complexity: implementation details differ. Infrastructure partners like Torsion handle multi-jurisdiction compliance so treasury teams don’t need regulatory expertise in both.

Side-by-Side: Where GENIUS Act and MiCA Converge

For CFOs managing global treasury operations, understanding alignment and divergence matters.

Core Protections: Aligned Across Jurisdictions

| Requirement | GENIUS Act (U.S.) | MiCA (EU) |

| Reserve Backing | 1:1, monthly audits | 1:1, quarterly audits |

| Redemption Rights | At par, on demand | Face value, on demand |

| Algorithmic Stablecoins | Effectively banned | Explicitly banned |

| Interest Payments | Prohibited | Prohibited |

| Bankruptcy Protection | Priority for holders | Segregated reserves |

| Regulatory Oversight | Federal banking regulators | EBA + national authorities |

| Audit Frequency | Monthly | Quarterly |

The Key Alignment: Both frameworks treat stablecoins as electronic money/payment instruments, not securities. This removes SEC/ESMA uncertainty that paralyzed adoption pre-2025.

Where They Differ (and Why It Matters)

1. Scope

- GENIUS Act: Payment stablecoins only

- MiCA: All crypto assets (broader regulatory reach)

- Implication: MiCA compliance requires understanding broader crypto asset rules

2. Licensing Threshold

- GENIUS Act: State licensing allowed up to $10 billion circulation, then federal oversight required

- MiCA: Immediate EU-wide licensing required

- Implication: Lower barrier to entry in U.S. for smaller issuers

3. Operational Restrictions

- GENIUS Act: No daily transaction caps

- MiCA: €200 million/day cap per issuer for systemically important stablecoins

- Implication: High-volume enterprise use cases may face caps under MiCA

4. Reserve Geography

- GENIUS Act: Reserves can be held globally

- MiCA: Reserves must be in EU financial institutions

- Implication: EU sovereignty requirement adds operational complexity

5. Foreign Issuer Access

- GENIUS Act: Foreign issuers allowed if jurisdiction deemed “substantially similar” by Treasury

- MiCA: Must establish EU legal entity

- Implication: Circle (U.S.-based) can issue USDC for U.S. market but needs EU entity for EURC

The Passporting Opportunity (Coming 2026-2027)

The GENIUS Act authorizes the Treasury Department to pursue regulatory harmonization with comparable jurisdictions.

Potential outcome:

- U.S.-licensed issuers could expand to EU markets with home regulator backing

- EU-licensed issuers could gain U.S. market access without establishing separate entities

- Single regulatory approval, multi-jurisdiction market access

Current status: Under development, expected 2026-2027 as Treasury and EBA negotiate equivalency frameworks.

What this means for CFOs: If your organization operates globally, infrastructure that’s compliant with both frameworks from day one positions you for seamless expansion when passporting becomes available.

What Enterprise Adoption Actually Looks Like (Post-Regulation)

Regulatory clarity doesn’t just reduce risk, it accelerates implementation.

The Adoption Surge: Data from Q3 2025

Current Users: 13%

- 13% of companies already using stablecoins for payments (primarily cross-border)

Near-Term Implementers: 54%

- 54% of non-users plan adoption within 6-12 months (post-GENIUS Act survey conducted August 2025)

Long-Term Projection

- By 2030: 5-10% of cross-border payments via stablecoins = $2.1-4.2 trillion annually

- Stablecoin market cap projection: $3+ trillion by 2030

Cost Savings Driving Implementation

- 41% of current users report 10%+ cost reduction on global transactions

- Traditional wire costs: $20-50 per transaction

- Stablecoin costs: Under $5 per transaction

- Settlement acceleration: 3-5 days → minutes

The Banking Partner Shift (Critical Signal for CFOs)

Pre-GENIUS Act Reality:

- Banks hesitant to support stablecoin infrastructure due to regulatory uncertainty

- 51% of EU firms, 20% of U.S. firms cited “limited banking support” as barrier

Post-GENIUS Act Reality:

- “Banks warming up to working with stablecoin infrastructure”

- Major banks now building stablecoin capabilities

- CFOs can engage banking partners about timelines without regulatory pushback

What this signals: When banks, the most risk-averse financial institutions, commit resources to stablecoin infrastructure, regulatory clarity is real.

Real Enterprise Use Cases Enabled by Regulation

Payment Processors Repositioning

- Stripe: Applied for OCC national bank charter under GENIUS Act framework

- Strategic intent: Direct stablecoin issuance and payment infrastructure

- Implication: Major payment processors see stablecoins as core infrastructure, not experimental

Asset Managers Entering Market

- BlackRock: Re-tooled money market fund specifically to serve stablecoin issuers

- Significance: World’s largest asset manager validates regulated stablecoin infrastructure

- Signal to CFOs: Institutional-grade financial services now support stablecoin ecosystem

Corporate Treasury Applications

- Manufacturers: 50%+ cost reduction on international supplier payments

- Tech companies: Instant contractor payments across 10+ countries

- E-commerce: Market expansion to regions blocked by traditional payment processors

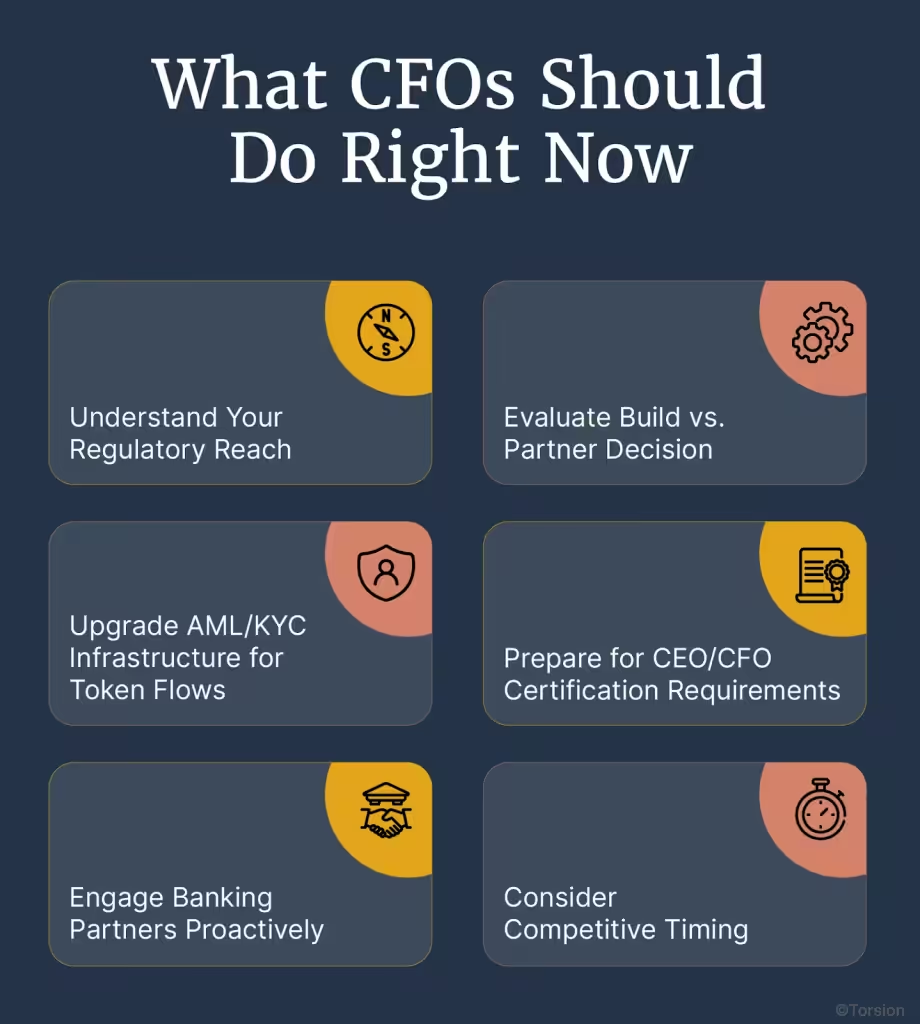

What CFOs Should Do Right Now

Regulatory clarity creates action items.

1. Understand Your Regulatory Reach

Map Current Operations:

- Which jurisdictions do your payments touch?

- U.S. only? GENIUS Act applies, January 2027 deadline

- EU operations? MiCA compliance mandatory now (December 2024 effective)

- Both? Need infrastructure compliant with both frameworks

Identify Compliance Obligations:

- Are you issuing stablecoins (requires licensing) or using them (requires standard BSA/AML)?

- Reality check: Most CFOs are users, not issuers

- User obligations: Standard BSA/AML compliance your treasury already maintains

2. Evaluate Build vs. Partner Decision

Build In-House Reality:

- Timeline: 12-18 months

- Cost: $5M+ development, $2-5M annual compliance

- Challenge: January 2027 deadline is 15 months away, building in-house may miss window

Partner with Infrastructure Reality:

- Timeline: 2-4 weeks implementation

- Cost: Transaction-based pricing (under $5 per payment)

- Advantage: GENIUS Act + MiCA compliance built-in from day one

The Strategic Question:

- Is stablecoin infrastructure your core competency?

- Or is capturing cost savings through compliant infrastructure your goal?

Torsion’s Positioning:

Just as Torsion bridges AI strategy to execution, the same principle applies to payment infrastructure: CFOs understand the regulatory requirements and business case. What they need is compliant execution. Torsion handles technical integration, GENIUS Act and MiCA compliance, and accounting treatment, turning regulatory frameworks into competitive advantages.

3. Upgrade AML/KYC Infrastructure for Token Flows

What GENIUS Act Requires:

- Transaction monitoring for stablecoin payments, not just wire transfers

- Suspicious activity reporting when token flows trigger thresholds

- Travel Rule compliance for transactions over $3,000

- Real-time sanctions screening

What Your Treasury Team Likely Has:

- BSA/AML infrastructure for traditional banking transactions

- Gap: Token flow monitoring and blockchain transaction analysis

What Torsion Provides:

- Chainalysis and TRM Labs integration for AML/KYC

- Automated suspicious activity reporting

- Transaction monitoring purpose-built for stablecoin payments

- Full compliance documentation for auditors

4. Prepare for CEO/CFO Certification Requirements

Personal Liability Reality:

- GENIUS Act requires monthly CEO/CFO certification of reserve accuracy

- Criminal penalties: Up to 20 years imprisonment, $5 million fine for false certification

- This makes audit-ready infrastructure non-negotiable

What Auditors Need:

- Transaction IDs (blockchain proof of payment)

- Reserve audit reports (monthly attestations from compliant issuers)

- Custody confirmation from regulated custodians

- KYC documentation for all counterparties

What Torsion Provides Automatically:

- All of the above, formatted for enterprise accounting systems

- Monthly compliance reports

- Full audit trail with immutable blockchain records

- SOC 2 Type II certified infrastructure

5. Engage Banking Partners Proactively

The Conversation CFOs Should Have:

- “What’s your timeline for supporting stablecoin payment infrastructure?”

- “Do you have partnerships with GENIUS Act-compliant issuers?”

- “What documentation do you need from us for stablecoin-based treasury operations?”

Why This Matters:

- Banks now have regulatory clarity to build stablecoin capabilities

- Early conversations secure priority as banks roll out infrastructure

- Late movers may face capacity constraints in 2026-2027

6. Consider Competitive Timing

The 54% Window:

- 54% of companies plan adoption within 6-12 months

- Those implementing Q4 2025/Q1 2026 capture first-mover advantages

- Late movers face catch-up on both technology and market positioning

Cost Savings Compound:

- 41% seeing 10%+ cost reduction immediately

- Every quarter delayed = higher cumulative opportunity cost

- Payment cost reduction: $20-50 → under $5 per transaction

The Strategic Question:

Is this a 2025 priority or 2026 priority? Companies answering “2025” will report measurable cost savings on Q1 2026 earnings calls. Companies answering “2026” will be explaining why competitors moved first.

From Regulatory Clarity to Strategic Imperative

Three years ago, CFOs evaluating stablecoin payments faced regulatory uncertainty that made implementation career-risky. The GENIUS Act (July 2025) and MiCA (December 2024) ended that uncertainty.

What these frameworks established:

- Clear definitions: Payment stablecoins are regulated electronic money, not securities

- Reserve requirements: 1:1 backing, monthly audits, CEO/CFO certification

- Consumer protections: Bankruptcy priority, redemption at par, algorithmic ban

- Compliance obligations: Standard BSA/AML for users, enhanced oversight for issuers

- Implementation timeline: January 2027 for GENIUS Act, already effective for MiCA

What the market shows:

- 54% of companies plan adoption within 6-12 months (post-regulation survey)

- 41% of current users report 10%+ cost reduction

- Cross-border payment opportunity: $2.1-4.2 trillion by 2030

- Major institutions (Stripe, BlackRock) positioning for stablecoin infrastructure

What remains is execution.

Most CFOs don’t need to issue stablecoins, they need to use them efficiently while maintaining GENIUS Act and MiCA compliance. This requires infrastructure that handles technical integration, regulatory reporting, and accounting treatment without requiring treasury teams to build crypto expertise.

Torsion provides enterprise-grade stablecoin implementation with built-in GENIUS Act and MiCA compliance. We handle the technical integration, regulatory compliance, and accounting treatment so your treasury team captures cost savings without regulatory exposure or crypto expertise.

The question CFOs faced in June 2025 was “Is regulation coming?” That question is answered. The question CFOs face in October 2025 is “How do we implement compliant infrastructure before competitors capture market share?”

Regulatory frameworks don’t just reduce risk, they create competitive windows.

The window is open.

Implementation timelines are measured in weeks, not quarters. The companies implementing Q4 2025 will report stablecoin cost savings on Q1 2026 earnings calls. The companies still evaluating in Q1 2026 will be explaining to boards why competitors moved first.

Ready to implement GENIUS Act and MiCA-compliant stablecoin infrastructure? Torsion bridges regulatory strategy to operational execution, 2-4 week implementation with full compliance built in.