Key Takeaways

- Stripe’s dual charter strategy (Georgia MALPB + OCC trust charter) signals vertical integration, owning card network access + stablecoin infrastructure + custody services

- October 2025 charter wave: Stripe/Bridge, Coinbase, Circle, Paxos, Ripple all applied post-GENIUS Act, reveals industry consensus on blockchain settlement shift

- 12-24 month charter approval timeline creates strategic window for CTOs to pilot stablecoin infrastructure before chartered platforms operational Q3-Q4 2026

- Payment cost transformation: Traditional 2.9-4.5% → stablecoin 0.5-1.0% represents $2M-$5M annual savings for $150M volume companies

- No blockchain expertise required: REST API integration abstracts complexity, engineering teams treat stablecoins like any payment processor

- GENIUS Act (July 2025) resolved regulatory uncertainty blocking 2020-2021 charter applications; institutional adoption now feasible with clear compliance path

- Early adopter advantage: 18-24 months cost savings + optimization experience competitors miss while waiting for chartered platforms

- Hybrid architecture optimal: Maintain traditional processing, add stablecoin for high-ROI use cases (international, B2B, high-volume)

- Compliance included: Processors handle AML/KYC, transaction monitoring, regulatory reporting, teams don’t build crypto compliance programs

- ROI payback averages 3-6 months for high-volume processors from payment cost reduction alone, excluding working capital and international expansion benefits

October 14, 2025. While most CTOs were reviewing Q3 infrastructure metrics, Stripe’s subsidiary Bridge filed an application with the Office of the Comptroller of the Currency for a national trust charter. Less than two weeks earlier, Coinbase submitted a similar application.

For the payment processor powering millions of businesses globally, this wasn’t regulatory housekeeping. It was infrastructure repositioning.

Jordan Martinez, CTO at a $150M revenue fintech platform, noticed the headline in his morning fintech newsletter. His first reaction: “What does a trust charter even do, and why should I care?”

His second reaction, after coffee and deeper research: “If Stripe is spending 12-24 months and millions in legal costs to become a federally chartered institution, this signals something fundamental about payment infrastructure’s direction.”

He was right. Within months of GENIUS Act passage (federal stablecoin framework signed July 2025), payment infrastructure’s biggest players, Stripe, Coinbase, Circle, Paxos, Ripple, all applied for federal bank charters. This wasn’t coincidence. It was coordinated industry repositioning.

Traditional payment architecture: Merchant → Processor → Sponsor Bank → Card Network → Issuing Bank (5 intermediaries, 2-5 days settlement, 2.9-4.5% fees)

Emerging architecture: Merchant → Chartered Platform → Blockchain → Settlement (2 intermediaries, 10 minutes, 0.5-1% fees)

For CTOs like Jordan processing $150M annually in transactions ($4.35M-$6.75M in annual payment fees), charter applications aren’t abstract regulatory news. They’re concrete infrastructure signals demanding strategic response: pilot stablecoin infrastructure now and gain 18-24 month optimization advantage, or wait for chartered platforms to launch in Q3-Q4 2026 and enter as late follower.

This is what Stripe’s charter strategy reveals, and what CTOs should do during the 12-24 month window before chartered platforms go live.

Stripe’s Dual Charter Strategy: Building End-to-End Payment Control

The Strategic Timeline That Tells the Story

April 2025: Georgia MALPB Charter Approved

Stripe became a Merchant Acquirer Limited Purpose Bank (MALPB) in Georgia, eliminating sponsor bank dependency for card processing. This granted direct membership in card networks (Visa, Mastercard), allowing Stripe to process transactions without intermediary banks.

Business impact:

- Sponsor bank markup eliminated: 0.10-0.15% cost reduction per transaction

- Settlement acceleration: 2-5 days → 1-2 days for merchants

- Reduced failure points: fewer entities between merchant and card network

For Stripe’s enterprise customers, this translated to lower fees and faster access to funds. For Stripe, this meant owning more of the payment infrastructure stack rather than partnering.

October 2024: Bridge Acquisition (The Setup Move)

Months before the charter application, Stripe acquired Bridge, a stablecoin infrastructure startup enabling organizations to issue custom stablecoins. Bridge’s platform provides instant exchange between custom stablecoins and major ones (USDC, Tether), solving the liquidity problem that makes custom stablecoins unviable.

Revenue model innovation: Organizations issuing stablecoins retain yield on underlying reserves (typically US Treasury bills generating 4-5% annually), rather than paying third-party issuers like Circle or Tether. On $1 billion in reserves, this represents $40M-$50M annual revenue opportunity.

October 2025: OCC Trust Charter Application (The Infrastructure Play)

Bridge applied for federal trust charter to operate stablecoin issuance and custody under OCC supervision. This charter would authorize:

- Stablecoin creation, management, and redemption under federal framework

- Digital asset custody for institutional clients

- Payment services using stablecoins and blockchain networks

- Reserve management (maintaining backing assets for stablecoins)

What the Combined Strategy Reveals

Vertical Integration, Not Partnership

Stripe’s strategy maps to complete payment stack ownership:

- Card processing: Direct network membership via MALPB charter

- Stablecoin infrastructure: Issuance platform via Bridge acquisition

- Federal oversight: Trust charter for regulated stablecoin operations

- Blockchain development: Building Tempo blockchain (announced 2025)

This isn’t diversification. It’s infrastructure repositioning, owning the entire payment flow from merchant to final settlement, whether via card networks or blockchain.

The Cost Structure Transformation

Current Stripe pricing: 2.9% + $0.30 per transaction for most merchants

MALPB charter cost reduction: Eliminating sponsor bank markup reduces Stripe’s cost by 0.10-0.15% per transaction

Stablecoin settlement potential: Blockchain settlement eliminates card network fees (1.5-2.0% of transaction cost)

Combined: If Stripe passes savings to merchants, hybrid model could reduce costs from 2.9% to 1.5-2.0%, or Stripe captures margin improvement while maintaining competitive pricing.

For merchants processing $150M annually, the difference between 2.9% and 1.5% represents $2.1M in annual savings, material enough to drive infrastructure decisions.

Why This Timing?

Regulatory Clarity Window Opens

GENIUS Act (passed Senate June 2025, signed into law July 2025) established federal framework for stablecoin regulation. This resolved uncertainty that blocked previous charter applications in 2020-2021, where conditional approvals expired because companies couldn’t operationalize under unclear rules.

What GENIUS Act provides:

- 1:1 USD reserve backing requirements (high-quality liquid assets like US Treasury bills)

- Monthly Big Four accounting firm audits

- Consumer protection standards (clear redemption rights, disclosure requirements)

- Federal or state charter requirement for stablecoin issuers

Post-GENIUS Act, institutional adoption became feasible with clear compliance path. Charter applications surged immediately.

The Competitive Wave

Stripe isn’t alone, the charter application wave reveals industry consensus:

- Coinbase (October 3, 2025): Custody expansion and payment services

- Bridge/Stripe (October 14, 2025): Stablecoin issuance platform

- Paxos (August 12, 2025): Stablecoin infrastructure

- Circle (2025): USDC issuer seeking federal charter

- Ripple (2025): Blockchain payment networks

Companies spending 12-24 months and millions pursuing federal charters aren’t hedging, they’re repositioning for fundamental shift. Charter status becomes competitive moat separating regulated infrastructure from uncertain alternatives.

Trust Charter Mechanics: What It Enables and Why Banks Are Fighting It

For CTOs evaluating infrastructure strategy, understanding trust charter specifics matters less than understanding what regulatory positioning enables. But the constraints reveal why this matters.

What Federal Trust Charters Provide

Operational Authorities:

- Stablecoin issuance: Create and manage USD-backed tokens under federal supervision

- Custody services: Hold digital assets for institutional clients

- Payment operations: Facilitate transactions using stablecoins or digital assets

- Reserve management: Maintain backing assets (US Treasury bills) for stablecoins

What Charters Cannot Do:

- No deposit-taking: Cannot accept FDIC-insured customer deposits

- No lending: Cannot make loans or extend credit

- Limited Fed access: Master accounts possible but not automatic

The constraint reveals the strategy: payment infrastructure companies want federal oversight for legitimacy without full banking regulatory burden.

The Federal Preemption Advantage

State Licensing Eliminated

Traditional money transmitter operations require 50 separate state licenses, each with different capital requirements, examination schedules, and compliance obligations. Legal costs: $2M-$5M annually maintaining multi-state licensing.

Federal trust charter replaces 50 state licenses with single OCC supervision. Nationwide operations require one application, not 50 approvals. For payment platforms expanding internationally, this simplification represents massive operational advantage.

Why CTOs Should Care: Integration partners with federal charters mean fewer compliance variables when expanding to new markets or transaction types. State-by-state money transmitter licensing creates integration complexity most engineering teams don’t want to manage.

The Banking Industry Pushback (And What It Signals)

July 2025: Banking Trade Groups Send Opposition Letter to OCC

Bank Policy Institute, American Bankers Association, and America’s Credit Unions co-signed letter urging OCC to postpone charter decisions. Their arguments:

- Trust charters being used for “novel” activities beyond traditional fiduciary services

- Fintech companies gain charter benefits without full bank regulatory constraints

- Applications lack sufficient public information for meaningful assessment

- OCC policy change without proper public comment process

What this opposition reveals: Traditional banks perceive competitive threat serious enough to lobby regulators. Trust charters enable nationwide payment operations without deposit insurance costs or lending risk, potentially undercutting traditional bank payment services on price.

For CTOs, this signals charter applications represent genuine infrastructure shift, not regulatory compliance theater. Banks don’t lobby against irrelevant changes.

The Timeline Reality: Application to Operations

Charter Approval Process:

- Application submission with public notice period

- OCC review (6-12 months typical)

- Conditional approval (if granted)

- Pre-opening period: build systems, hire compliance team, establish controls (6-12 months)

- Pre-opening examination by OCC

- Final charter authorization

- Operations begin

Total timeline: 12-24 months from application to operations.

Current status (November 2025):

- Bridge/Stripe application pending (submitted October 14, 2025)

- Coinbase application pending (submitted October 3, 2025)

- No new trust charters approved in 2025 yet

Earliest operational timeframe: Q3-Q4 2026 for current applications.

This timeline creates the strategic window CTOs must navigate: 12-18 months before chartered platforms launch. Early adopters pilot stablecoin infrastructure during this window, gaining optimization experience competitors won’t have when chartered platforms go live.

The Stablecoin Infrastructure Build-Out: Why Everyone’s Applying Now

The charter application wave wasn’t spontaneous. It followed years of infrastructure development and regulatory uncertainty resolution.

The Previous Wave That Failed (2020-2021)

Applications submitted but companies couldn’t operationalize:

- Anchorage Digital Bank: Only crypto-native OCC-chartered bank (approved 2021)

- Protego Trust Bank: Conditional approval expired without launch

- Paxos National Trust: Conditional approval expired

Why 2020-2021 failed: No federal stablecoin framework. State-level money transmitter patchwork. OCC interpretive guidance subject to change. Result, conditional approvals companies couldn’t act on due to regulatory uncertainty.

Why 2025 Succeeds: The GENIUS Act Framework

Federal Stablecoin Regulation Established

GENIUS Act (July 2025) provides clarity previous applicants lacked:

- Reserve requirements: 1:1 USD backing in US Treasury bills or equivalent

- Audit standards: Monthly Big Four accounting firm verification

- Consumer protections: Redemption rights, disclosure requirements

- Charter path: Explicit authorization for federal charters for stablecoin issuers

This removes the regulatory uncertainty that killed 2020-2021 applications. Institutional adoption now feasible with clear compliance roadmap.

Market Scale Justifying Infrastructure Investment

Stablecoin Transaction Volume:

- $14 trillion processed in 2024, surpassing Visa

- $8.9 trillion in first half of 2025 alone

- $1+ trillion monthly volume consistently maintained

Institutional Adoption Indicators:

- 86% of financial institutions report infrastructure ready for stablecoin adoption

- 15% of CFOs plan to accept stablecoin payments within 2 years

- 23% of Fortune 500 treasury teams evaluating stablecoin strategies

This isn’t experimental technology, transaction volume rivals major card networks. Charter applications signal companies positioning for stablecoins as primary payment rails, not niche use case.

Bridge’s Custom Stablecoin Strategy

The Yield Problem Stripe Is Solving

Major stablecoins (USDC, Tether): Established liquidity, but yield on reserves goes to issuer (Circle, Tether Limited), not the organization using the stablecoin.

Custom stablecoins: Organization retains reserve yield, but lacks liquidity, custom tokens can’t easily exchange for goods/services.

Yield opportunity: $1 billion in stablecoin reserves generates $40M-$50M annually at 4-5% Treasury yields. For neobanks, payment platforms, or large marketplaces issuing billions in stablecoins, this represents significant revenue.

Bridge’s solution:

- Platform enabling organizations to issue custom stablecoins

- Instant exchange between custom and major stablecoins (USDC, Tether)

- Organizations retain reserve yield instead of paying third-party issuers

- Federal charter provides regulatory legitimacy for enterprise issuers

Target customers: Neobanks, digital wallets, payment firms, large marketplaces wanting branded stablecoins with yield retention.

This reveals broader trend: vertical integration. Stripe isn’t just accepting stablecoins, it’s building stablecoin issuance infrastructure. Circle is building Arc blockchain. PayPal issued PYUSD stablecoin. Payment platforms are integrating blockchain infrastructure rather than partnering.

What CTOs Should Do During the 12-24 Month Charter Window

Charter applications create strategic timing decision CTOs must navigate: pilot stablecoin infrastructure now, or wait for chartered platforms to launch in Q3-Q4 2026?

The Strategic Window: Now Through Q3 2026

Current state (November 2025):

- Charter applications pending, none approved yet in 2025

- GENIUS Act framework established (July 2025)

- Stripe/Coinbase Commerce/Circle operate under state licenses currently

- Stablecoin support available from major processors (Stripe already enabled USDC)

Chartered operations timeline: Q3-Q4 2026 earliest

The decision: 12-18 month window to pilot stablecoin infrastructure before chartered platforms fully operational.

What Early Adopters Gain

Cost Optimization Learning Curve

ROI calculation for $150M annual transaction volume:

- Current payment costs: 2.9-4.5% = $4.35M-$6.75M annually

- Stablecoin settlement: 0.5-1.0% = $750K-$1.5M annually

- Potential savings: $3M-$5.25M annually

Piloting during charter window allows:

- Transaction type optimization (which transactions benefit most from stablecoin settlement)

- Volume threshold identification (when to route via stablecoin vs. traditional)

- Process refinement before scaling

Companies piloting now gain 12-18 months cost savings competitors won’t capture while waiting for chartered platforms.

Working Capital Improvements

Traditional settlement: 2-5 days means $2M-$8M constantly in transit for $150M annual volume company. At 10% cost of capital, this represents $200K-$800K annual opportunity cost.

Stablecoin settlement: 10 minutes average, effectively eliminating working capital float. Early adopters optimize treasury operations 18 months before late followers.

International Expansion Enablement

Payment processor geographic restrictions block 5-10% of international transactions. Wire transfer costs ($45-140 per transaction) make sub-$1000 B2B transactions uneconomical.

Stablecoin settlement:

- <$5 transaction cost regardless of geography

- No FX markups (USDC pegged 1:1 to USD)

- 10-minute settlement globally

Early adopters launch international markets 12-18 months before competitors waiting for chartered platforms.

Implementation Expertise

Piloting reveals integration challenges:

- ERP reconciliation complexity

- Customer adoption patterns

- Compliance workflow optimization

- Accounting process refinement

When chartered platforms launch Q3-Q4 2026, early pilots have optimized implementations. Late followers scramble to build processes from scratch during compressed timeline.

Risk Mitigation: Hybrid Infrastructure Strategy

Don’t Replace, Add Options

Maintain traditional card processing for majority of transactions. Add stablecoin settlement for specific high-ROI use cases:

Priority Use Case 1: International Transactions

- Problem: $45-140 wire fees, 2-4% FX markups, 3-5 day settlement

- Stablecoin ROI: 70-80% cost reduction, 10-minute settlement

- Pilot approach: Route international B2B transactions over $500 via stablecoin initially

Priority Use Case 2: High-Volume Processing

- Problem: $150M annual volume at 2.9% = $4.35M fees

- Stablecoin ROI: 1.5-2.0% cost reduction = $2M-$3M savings

- Pilot approach: 10-20% of transaction volume routed via stablecoin, scale based on results

Priority Use Case 3: B2B Invoice Settlement

- Problem: Net 30-60 payment terms, wire costs, reconciliation complexity

- Stablecoin ROI: Instant settlement, automated reconciliation, lower costs

- Pilot approach: Offer stablecoin option for invoices >$5K initially

Maintain traditional processing for:

- Small transaction volumes (<$1M annually where cost optimization less material)

- Consumer-facing retail (low stablecoin wallet penetration currently)

- Highly regulated industries requiring extra compliance review

This hybrid approach provides downside protection, if stablecoin adoption slower than expected, traditional infrastructure continues operating unchanged.

Implementation Without Blockchain Expertise: The Technical Reality

CTOs hesitate on stablecoin adoption because they assume blockchain expertise requirement. Modern integration architecture eliminates this concern.

The API Abstraction Layer

Integration Architecture:

What engineering teams see: REST API integration resembling any payment processor

- API endpoints for initiating payments

- Webhook handlers for settlement confirmations

- Transaction ID mapping to internal systems

- Standard error handling and retry logic

What runs underneath (handled by integration layer):

- Blockchain transaction submission

- Gas fee optimization

- Block confirmation monitoring

- Wallet security and key management

- Network selection (Ethereum, Polygon, Solana)

Engineering teams don’t interact with blockchain directly, API layer abstracts complexity identical to how Stripe abstracts card network interactions.

Three Integration Pathways

Option 1: Stripe USDC Support (Fastest – 2-4 Weeks)

Implementation:

- Enable USDC in Stripe dashboard toggle

- Configure auto-conversion (customer pays USDC → merchant receives USD)

- Test settlement webhooks in staging environment

- Deploy to production with 5-10% traffic initially

What Stripe handles:

- Blockchain settlement

- AML/KYC compliance

- Wallet custody

- Fiat conversion

What your team builds:

- Webhook endpoint integration (4-8 hours development)

- ERP reconciliation mapping (8-16 hours)

- Dashboard updates showing stablecoin transactions (optional)

Option 2: Circle/Coinbase Commerce Direct (Standard – 2-4 Weeks)

Implementation:

- REST API integration with Circle or Coinbase Commerce

- Custom webhook handling for blockchain settlement confirmations

- Reconciliation automation with existing ERP (NetSuite, SAP, QuickBooks)

What platform handles:

- USDC issuance/redemption

- Blockchain infrastructure

- Compliance monitoring (AML/KYC via Chainalysis/TRM Labs)

- Regulatory reporting

What your team builds:

- API integration (1-2 weeks)

- Webhook settlement logic (2-4 days)

- ERP reconciliation automation (4-6 days)

- Admin dashboard for finance team (optional)

Option 3: Custom Implementation with Torsion (Enterprise – 2-4 Weeks)

Implementation:

- Platform-agnostic integration (works with Stripe, Circle, Coinbase, or future chartered platforms)

- Complete compliance infrastructure (AML/KYC, GENIUS Act reporting, SOC2)

- ERP reconciliation automation in existing format

- Accounting treatment documentation for auditors

What Torsion delivers:

- API integration layer connecting payment systems to stablecoin processors

- Webhook handling and settlement confirmation logic

- Automated reconciliation mapping to NetSuite/SAP/QuickBooks

- Compliance infrastructure (transaction monitoring, reporting)

- Code ownership post-implementation (no vendor lock-in)

Timeline: 2-4 weeks for most implementations, 4-6 weeks for complex legacy systems

Compliance: What Engineering Teams Don’t Need to Build

AML/KYC Infrastructure

Payment processors (Stripe, Circle, Coinbase) handle Anti-Money Laundering and Know Your Customer requirements:

- Customer identity verification

- Transaction monitoring for suspicious activity

- Sanctions screening (OFAC compliance)

- Suspicious Activity Report (SAR) filing when required

Engineering teams don’t build cryptocurrency compliance programs, processors manage regulatory obligations identical to traditional payment compliance.

Accounting Treatment

Stablecoins classified as cash equivalents, not crypto assets, on balance sheets. This means:

- Revenue recognition unchanged (ASC 606 applies normally)

- Journal entries similar to foreign currency transactions

- No volatile cryptocurrency accounting (mark-to-market unnecessary)

Finance teams receive reconciliation reports showing:

- Transaction ID

- USD-equivalent amount at settlement

- Settlement timestamp

- Mapping to internal invoice/order ID

Reports appear in standard ERP format, finance teams don’t learn cryptocurrency accounting.

The Decision Framework: Pilot Now or Wait for Charters?

CTOs face timing decision with material competitive implications.

Pilot Now (Recommended for Most)

Who should pilot immediately:

- High-volume processors ($50M+ annual transactions): 1.5-2% cost reduction = $750K-$1.5M annual savings justifies immediate pilot

- International businesses: Payment processor blocks or high wire costs ($45-140/transaction) preventing market expansion

- B2B companies: Invoice settlement via wire transfer costs >$50K annually

Advantages:

- 18-24 month cost savings competitors won’t capture while waiting

- Process optimization before mainstream adoption surge

- Competitive advantage in markets where stablecoin settlement enables expansion

- Platform flexibility, pilot with current unchartered platforms, migrate to chartered alternatives when available

Risks:

- Implementation effort (2-4 weeks) without guaranteed ROI if adoption slower than projected

- Regulatory uncertainty if GENIUS Act enforcement changes (low probability given legislative framework)

- Customer adoption challenges if wallet penetration lower than expected

Risk mitigation: Hybrid architecture (maintain traditional + add stablecoin) limits downside. If pilot underperforms, traditional processing continues unchanged.

Wait for Chartered Platforms (Q3-Q4 2026)

Who should wait:

- Low-volume businesses (<$10M annual transactions): Cost savings ($50K-$150K) may not justify implementation effort

- Highly regulated industries: Extra legal review required may delay implementation regardless of charter status

- Companies lacking technical resources: Engineering teams at capacity cannot allocate 2-4 weeks for integration

Advantages:

- Regulatory certainty: Federal charter provides maximum compliance confidence

- Proven implementation: Learn from early adopters’ challenges and optimizations

- Lower integration risk: Chartered platforms likely have more mature integration tooling

Disadvantages:

- 18-24 months of cost savings lost ($1M-$3M for $150M volume company)

- Competitive disadvantage if early movers gain market share in international expansion

- Learning curve delay: Entering as late follower when mainstream adoption accelerates

The Hybrid Approach (Optimal for Most Mid-Market CTOs)

Strategy: Pilot with current platforms now, migrate to chartered platforms when operational.

Implementation:

- Months 1-2: Evaluate use case ROI (international transactions, high-volume processing, B2B settlement)

- Months 3-5: Implement pilot with Stripe USDC support or Circle/Coinbase direct integration (2-4 weeks)

- Months 6-12: Scale successful pilot from 10% to 25-30% of transaction volume

- Q3-Q4 2026: Evaluate chartered platform launches (Stripe/Bridge, Coinbase, Circle)

- 2027: Migrate to chartered platforms if enterprise risk/compliance requires, or maintain current integration if performing well

This approach captures cost savings and optimization experience during charter approval window, while maintaining flexibility to migrate to chartered platforms when available.

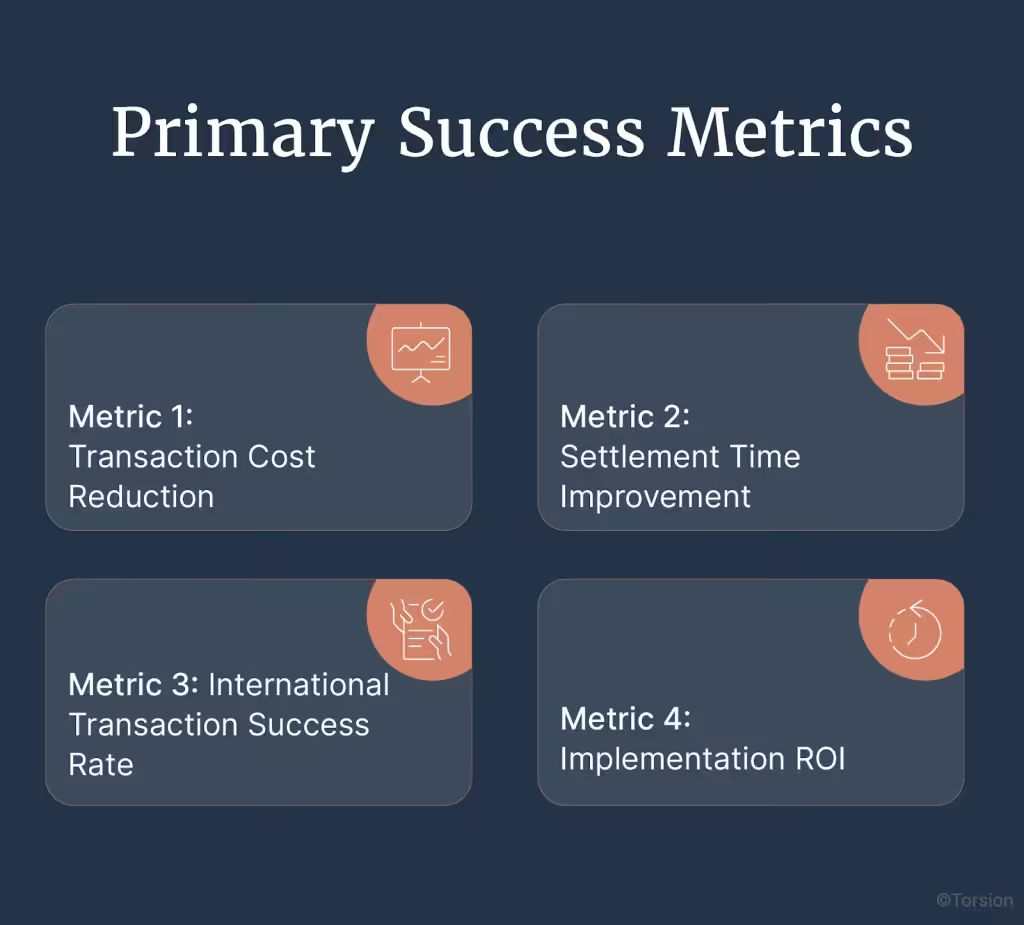

Measuring Success: The Metrics That Matter

Implementation without measurement wastes infrastructure investment. CTOs need proof stablecoin adoption delivers projected ROI.

Primary Success Metrics

Metric 1: Transaction Cost Reduction

Baseline: Current effective rate across all transactions (typically 2.9-4.5%)

Target: Stablecoin transactions at 0.5-1.0% (blended rate improves as volume shifts)

Measurement:

- Track payment processing costs monthly (traditional vs. stablecoin)

- Calculate weighted average rate across transaction mix

- Monitor cost per transaction by payment method

- Project annual savings at different volume thresholds

Success criteria: 30-50% cost reduction on stablecoin-settled transactions within 6 months

Metric 2: Settlement Time Improvement

Baseline: 2-5 days for traditional payment settlement

Target: 10 minutes average for stablecoin settlement

Measurement:

- Track time from transaction completion to funds available

- Calculate working capital freed from faster settlement

- Measure impact on treasury operations and cash forecasting

Success criteria: 95%+ stablecoin transactions settle within 20 minutes

Metric 3: International Transaction Success Rate

Baseline: 5-10% decline rate in international markets (payment processor blocks)

Target: <1% decline rate for stablecoin transactions

Measurement:

- Track transaction success rate by geography

- Monitor decline reasons (processor blocks vs. other causes)

- Calculate revenue recovered from previously blocked markets

Success criteria: 80-90% reduction in geography-related payment failures within 3 months

Metric 4: Implementation ROI

Investment:

- Engineering time: 2-4 weeks × team hourly rate

- Integration costs: $15K-$35K for enterprise implementations

- Ongoing operational costs: Minimal (processor fees offset by savings)

Returns:

- Annual payment cost savings (primary)

- Working capital optimization (secondary)

- International market revenue expansion (tertiary)

Success criteria: Payback period <6 months for high-volume processors, <12 months for mid-volume

Sample ROI: $150M Annual Transaction Volume

Current State:

- Transaction volume: $150M annually

- Effective payment rate: 2.9% (blended average)

- Annual payment costs: $4.35M

- International transaction decline rate: 8% ($6M attempted, $480K lost)

Pilot Implementation (Months 3-6):

- Stablecoin option added for international transactions and high-value B2B ($30M volume, 20% of total)

- Stablecoin effective rate: 0.8% (including processor fees)

- Traditional transactions continue at 2.9% ($120M volume, 80% of total)

Results After 6 Months:

- Stablecoin transaction costs: $240K (0.8% of $30M)

- Traditional transaction costs: $3.48M (2.9% of $120M)

- Total costs: $3.72M vs. $4.35M baseline = $630K annual savings (14.5% reduction)

- International decline rate: 2% ($120K vs. $480K lost = $360K revenue recovered)

- Combined first-year impact: $990K

Implementation cost: $25K-$35K (Torsion integration)

ROI: 2,829-3,960% return; payback period 9-13 days

These numbers reflect conservative pilot scope (20% volume). At 50% volume routed via stablecoin, savings exceed $1.5M annually.

Strategic Positioning: The Infrastructure Shift Happening Now

What the Charter Wave Signals

When Stripe, Coinbase, Circle, Paxos, and Ripple all pursue federal charters within months, they’re broadcasting consensus: Stablecoins transition from niche payment option to primary settlement infrastructure over next 3-5 years.

Companies don’t spend 12-24 months and millions in charter application costs for incremental opportunities. They reposition for fundamental infrastructure shift.

The Competitive Separation

Chartered platforms (post-approval Q3-Q4 2026):

- Attract enterprise customers requiring regulatory certainty

- “Federally chartered” becomes trust signal in sales process

- Higher compliance costs offset by lower customer acquisition friction

Unchartered platforms (current state):

- Faster iteration without OCC examination overhead

- Lower operational costs but harder enterprise sales

- May lose market share to chartered competitors as regulation matures

Traditional payment processors (without stablecoin strategy):

- Defend card network economics (2.9-4.5% fees) against 0.5-1% stablecoin alternative

- Risk losing high-volume merchants to cost-optimized competitors

- Forced to add stablecoin support or cede market share

Early adopter CTOs (pilot during charter window):

- Capture 18-24 months cost savings and optimization experience

- Build competitive advantage in international markets

- Gain infrastructure expertise before mainstream adoption surge

Late follower CTOs (wait for chartered platforms):

- Enter with regulatory confidence but 18-24 month disadvantage

- Scramble to build processes when competitors have optimized implementations

- Accept higher costs and competitive weakness during wait period

The 2027-2028 Outlook

2026: Chartered platforms operational, GENIUS Act enforcement established, enterprise adoption accelerates

2027: Stablecoin infrastructure mature at scale, cost advantages force industry-wide consideration

2028: Blockchain settlement competes directly with card networks for primary payment rails, late movers scramble to catch up

The infrastructure shift rarely reverses once transaction volume reaches critical mass. Stablecoins processed $14 trillion in 2024, already matching major card networks. Charter applications signal payment infrastructure’s biggest players repositioning for blockchain-based settlement as permanent infrastructure, not temporary experiment.

Implementation Strategy: Your Next 90 Days

Charter applications aren’t abstract news, they’re timing signals for infrastructure decisions CTOs must make now.

Immediate Actions (Next 30 Days)

Calculate Use Case ROI

International transaction analysis:

- Current volume and average transaction size

- Wire fees paid annually ($45-140 per transaction)

- FX markup costs (2-4% of value)

- Stablecoin savings projection: 70-80% cost reduction

High-volume processing analysis:

- Annual payment processing volume

- Current effective rate (blended across all payment methods)

- Stablecoin potential: 1.5-2% rate reduction at scale

- Annual savings projection at 20%, 50%, 80% volume thresholds

Working capital analysis:

- Average settlement time (2-5 days)

- Dollar value in transit at any given time

- Opportunity cost at cost of capital percentage

- Instant settlement value: recovered working capital

Assemble Cross-Functional Team

- Engineering: Integration requirements, timeline estimation, resource allocation

- Finance/Treasury: Accounting treatment, reconciliation requirements, ROI validation

- Legal/Compliance: GENIUS Act framework, risk assessment, charter implications

- Product: Customer experience, international expansion alignment

Define Pilot Scope

Start narrow, prove value, then scale:

- Priority Use Case 1: International transactions (highest ROI, clearest value)

- Priority Use Case 2: B2B invoice settlement >$5K (material cost savings)

- Volume target: 10-20% of transactions initially, scale based on results

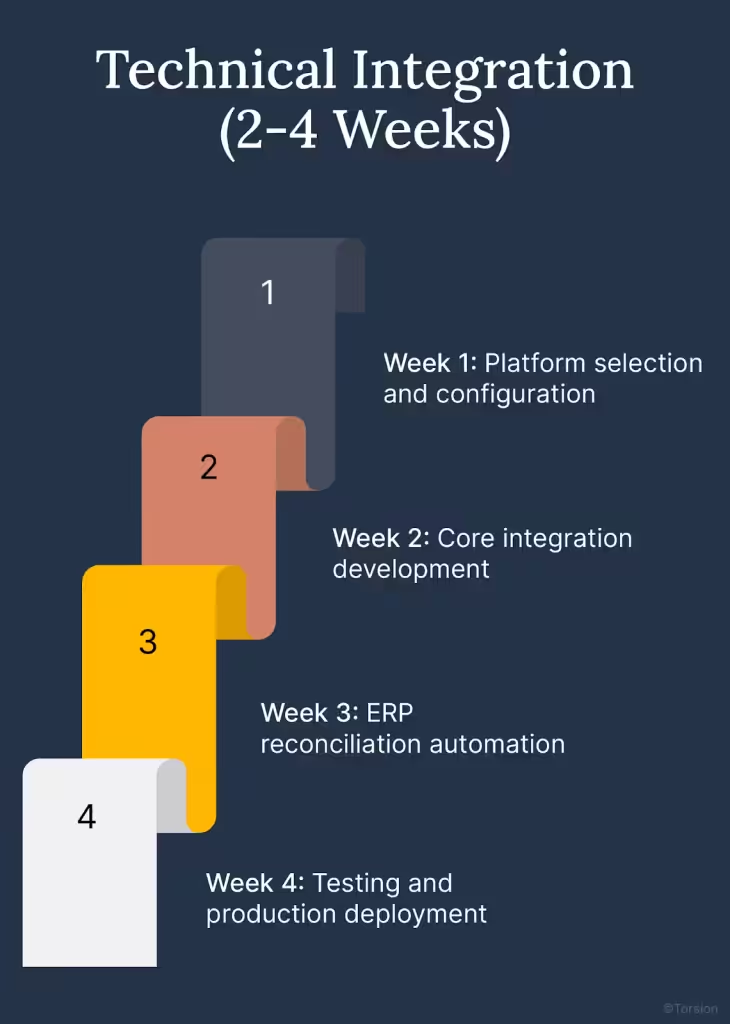

Implementation Phase (Days 30-90)

Technical Integration (2-4 Weeks)

Week 1: Platform selection and configuration

- Choose integration path (Stripe USDC, Circle direct, Coinbase Commerce, or Torsion)

- Configure sandbox environment and test credentials

- Review technical documentation and API specifications

Week 2: Core integration development

- REST API integration with payment platform

- Webhook handlers for settlement confirmations

- Transaction ID mapping to internal systems

- Error handling and retry logic

Week 3: ERP reconciliation automation

- NetSuite/SAP/QuickBooks integration for automated reconciliation

- Journal entry generation in existing format

- Finance team dashboard for transaction monitoring

Week 4: Testing and production deployment

- Staging environment testing with test transactions

- Production deployment to 5-10% traffic initially

- Monitoring setup for settlement times, costs, failure rates

Compliance Documentation (Parallel Effort)

- Accounting treatment memo for auditors (stablecoins as cash equivalents)

- AML/KYC procedures documented (processor-managed typically)

- Transaction monitoring thresholds established

- Regulatory reporting protocols (GENIUS Act compliance)

Scale Decision (Day 90+)

Evaluation Criteria:

- Cost reduction achieved: Target 30-50% reduction on stablecoin transactions

- Settlement time improvement: 95%+ transactions <20 minutes

- Operational complexity: Reconciliation automation success, manual intervention required

- Customer adoption: If customer-facing, what percentage choose stablecoin option

Scale paths:

- Expand if: 30%+ cost reduction, <10% operational burden increase, clean reconciliation

- Maintain pilot if: 15-30% savings, moderate complexity, some manual processes remain

- Revisit if: <15% savings or significant operational challenges discovered

Charter monitoring (Ongoing through 2026):

- Track Bridge/Stripe charter progress (application October 2025)

- Monitor Coinbase, Circle, Paxos charter status

- Evaluate migration to chartered platforms when operational Q3-Q4 2026

The Infrastructure Decision CTOs Can’t Delay

Stripe’s OCC charter application wasn’t regulatory compliance. It was infrastructure repositioning, signaling payment architecture shifting from card networks to blockchain settlement over next 3-5 years.

The dual charter strategy, Georgia MALPB for card processing + OCC trust charter for stablecoin operations, maps to complete payment stack control: direct network membership, stablecoin issuance, custody services, federal oversight.

For CTOs processing $50M-$200M annually in transactions, charter applications create timing decision with material competitive implications:

Pilot now (recommended): Capture 18-24 months cost savings ($1M-$4M for typical mid-market company), gain optimization experience before chartered platforms launch Q3-Q4 2026, build competitive advantage in international markets.

Wait for charters (lower risk, higher cost): Enter with maximum regulatory certainty but accept 18-24 month cost disadvantage and competitive weakness while competitors optimize implementations.

Do nothing: Payment costs remain 2.9-4.5% while competitors achieve 0.5-1.5%, international expansion blocked, infrastructure disadvantage compounds as stablecoin adoption scales industry-wide.

The charter application wave, Stripe, Coinbase, Circle, Paxos, Ripple, reveals industry consensus: Stablecoins aren’t speculative experiment but infrastructure repositioning payment companies believe becomes permanent settlement rails.

CTOs delaying evaluation until chartered platforms launch in 12-18 months miss the optimization window. Cost savings, working capital improvements, and process expertise compound during pilot period, advantages late followers don’t recover.

Payment infrastructure rarely shifts this fundamentally. The question isn’t whether blockchain settlement competes with card networks, transaction volume ($14 trillion in 2024) proves viability. The question is whether your infrastructure strategy positions for this shift, or risks competitive disadvantage when chartered platforms launch and mainstream enterprise adoption accelerates.

Prepare Your Stablecoin Infrastructure Strategy

Torsion builds enterprise stablecoin payment infrastructure, integrating with Stripe, Circle, Coinbase Commerce, or chartered platforms when operational. REST API integration, compliance infrastructure included, you own the code post-implementation.

Implementation includes:

- Use case ROI analysis (international, high-volume, B2B settlement)

- Platform integration (2-4 weeks), works with current and future chartered platforms

- Compliance infrastructure (AML/KYC, GENIUS Act reporting, SOC2)

- ERP reconciliation automation (NetSuite, SAP, QuickBooks)

Schedule Infrastructure Assessment →

What’s your primary stablecoin evaluation driver?

☐ Payment cost reduction ($2M-$5M annual savings opportunity)

☐ International market expansion (payment processor blocks limiting growth)

☐ Charter application timing strategy (pilot now vs. wait for Q3-Q4 2026)

☐ Competitive positioning (understanding infrastructure shift implications)

Assessment evaluates payment infrastructure, calculates use case ROI, and delivers pilot implementation roadmap for execution before chartered platforms launch Q3-Q4 2026.