Key Takeaways

- Involuntary churn costs SaaS companies 20-40% of total churn, customers lost to payment failures, not product dissatisfaction

- Payment failure rates average 15% for credit cards, climbing to 15-25% in international markets

- Traditional dunning recovers 70% of failed payments; the remaining 30% represents permanent revenue loss

- Stablecoins eliminate payment failures through immutable settlement, geographic universality, and instant finalization

- USDC integration takes 2-4 weeks with existing billing systems (NetSuite, Stripe, SAP, QuickBooks)

- Payment finality prevents chargebacks and post-authorization failures, 0% chargeback rate vs. 0.5-1% traditional

- International expansion becomes viable when geographic processor blocks disappear

- ROI payback averages 2-4 months from involuntary churn reduction alone

- Stablecoins are cash equivalents for accounting, not crypto assets requiring specialized expertise

- Implementation delivers working code, teams own infrastructure post-launch with no vendor lock-in

Last Tuesday, a data scientist in Jakarta lost access to her team’s ML platform. Not because the product failed. Not because she found a competitor. Her credit card expired during the billing cycle, and the payment processor declined the transaction. By the time she noticed the service interruption three days later, her team had already scrambled to find alternatives.

She never canceled. The payment infrastructure canceled for her.

This scenario plays out thousands of times daily across B2B SaaS companies. Involuntary churn, customers lost due to payment failures rather than product dissatisfaction, accounts for 20-40% of total SaaS churn. That’s $129 billion in projected revenue losses across subscription businesses in 2025.

Here’s the uncomfortable truth: 53% of subscription churn stems from unpaid subscriptions due to failed payments, not unhappy customers. Your engineering team spends months perfecting product-market fit, your customer success team nurtures relationships, and your RevOps team optimizes retention playbooks, then payment infrastructure silently bleeds 0.8% of your Monthly Recurring Revenue every single month.

Traditional solutions, dunning emails, payment retries, backup payment methods, recover about 70% of failed payments at best. The remaining 30% represents permanent revenue loss. For a $10M ARR SaaS company, that’s $80K disappearing annually from customers who never wanted to leave.

Stablecoins eliminate the payment failure point entirely. Not by improving retry logic or sending better emails, but by removing the intermediaries that cause payments to fail in the first place. This is how.

The Silent Revenue Drain: Why Your Payments Are Failing

Average B2B SaaS companies experience 3.5% monthly churn. Break that down: 2.6% voluntary (customers who choose to leave) and 0.8% involuntary (customers lost to payment failures). That involuntary component is pure infrastructure failure, not product failure.

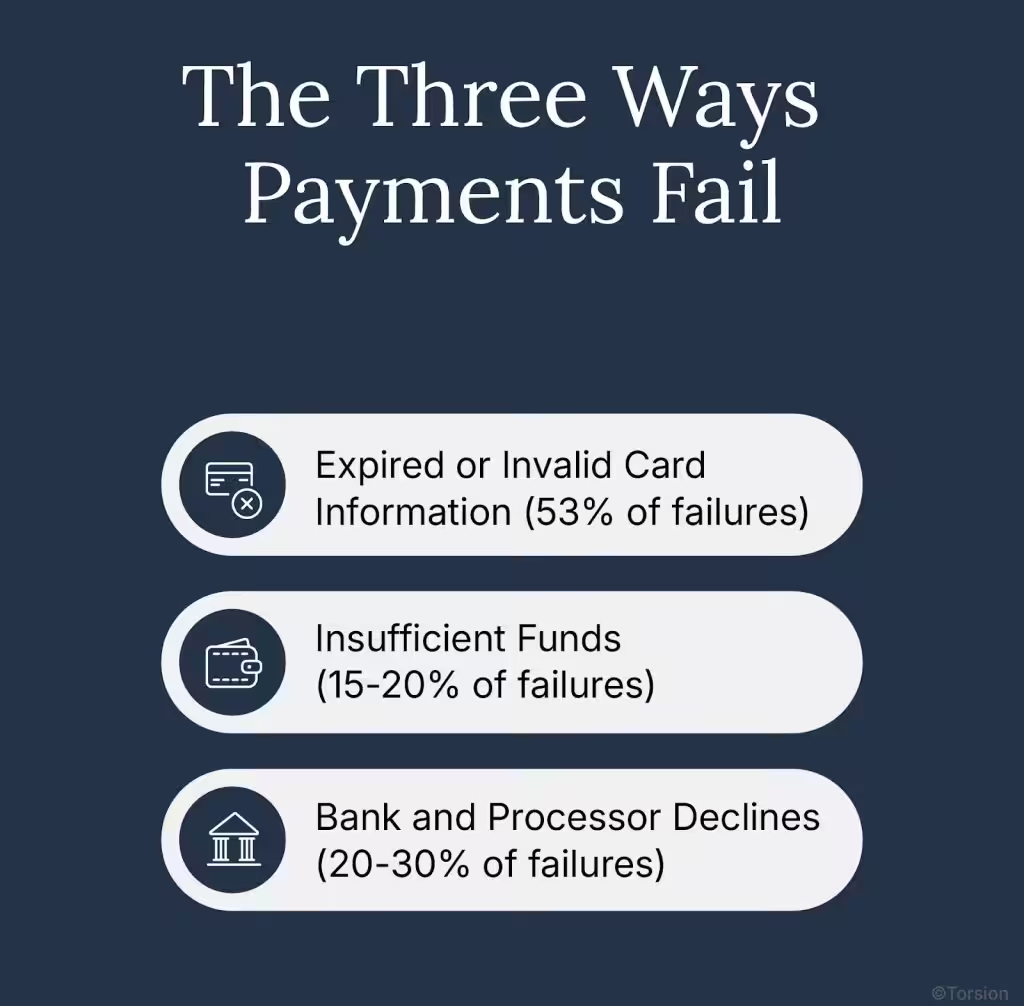

The Three Ways Payments Fail

1. Expired or Invalid Card Information (53% of failures)

Credit cards remain valid for approximately three years. Customers forget to update billing information. Companies relocate, triggering replacement cards. Banking relationships change. Each creates a failure point your dunning system can’t prevent.

The average credit card failure rate sits at 15%, meaning one in seven transactions fails before reaching your bank account. International markets amplify this dramatically. In Latin America, Southeast Asia, and parts of Africa, failure rates climb to 15-25% as payment processors actively block transactions from specific geographies.

2. Insufficient Funds (15-20% of failures)

B2B customers operate on cash flow cycles. Billing dates misalign with payroll schedules. International customers manage multi-currency accounts with timing delays. Seasonal businesses experience fluctuating working capital.

Your customer wants to pay. Their card simply lacks funds at the moment your payment processor attempts the charge. Traditional retry logic helps here, but introduces its own friction, service interruptions, dunning email fatigue, damaged customer perception.

3. Bank and Processor Declines (20-30% of failures)

Fraud detection systems generate false positives. Payment processors impose geographic restrictions. Network outages occur. Cross-border transactions trigger automatic blocks.

Most insidiously, payment processors block entire countries from processing transactions, not because your customers are risky, but because the processor’s risk models flag specific markets. Your product might solve critical problems for teams in Lagos or Buenos Aires, but your payment infrastructure never gives them a chance to subscribe.

The Business Impact Beyond Lost Revenue

Involuntary churn destroys more than this month’s MRR. Customer Acquisition Cost compounds the damage, you spent 5x more acquiring that customer than retaining them. Customer Lifetime Value calculations crumble when $50K+ enterprise accounts evaporate due to expired credit cards.

Product perception suffers. Research shows customers are 27% more likely to cancel permanently after experiencing service interruptions from failed payments, even when the interruption wasn’t their fault. Your infrastructure failure becomes their product dissatisfaction.

For international expansion, the problem becomes existential. If 59% of customers abandon checkout when their preferred payment method isn’t available, and your payment processor blocks 15-25% of international transactions, you’re not competing in those markets, you’re excluded by infrastructure.

Traditional payment recovery methods address symptoms. Stablecoins eliminate the disease.

Why Payment Retries and Dunning Aren’t Enough

Your payment operations team already runs a sophisticated retry machine. Smart dunning sequences. Account updater services pulling new card data from Visa and Mastercard networks. Grace periods extending access during payment resolution. Payment method diversification with ACH backup options.

These tactics recover 70% of failed payments in optimized implementations. For many engineering leaders, that feels like success, until you calculate what the remaining 30% costs.

The Recovery Rate Ceiling

Payment retry logic relies on the same failing infrastructure. If a credit card expired, retrying the same card produces the same failure. If a customer’s international transaction triggers processor blocks, retrying through the same processor hits the same geographic restrictions.

Dunning management requires customer action, they must manually update payment information, respond to emails, log into billing portals. Even with perfectly optimized sequences, 30% of customers never take that action before their service lapses.

Account updater services only solve card expiration. They don’t address insufficient funds, processor geographic blocks, or fraud false positives. ACH alternatives reduce failure rates to 3-5%, but international customers lack access to ACH clearing networks.

The Geographic Wall

For B2B SaaS companies pursuing international expansion, traditional payment infrastructure imposes hard constraints. Payment processors don’t just fail some transactions in growth markets, they prevent market entry entirely by blocking transactions from specific countries.

Foreign transaction fees stack up: 2.9% base rate, 1% international fee, 1-3% currency conversion markup. Suddenly your payment infrastructure costs 4-7% all-in, making your product uncompetitively priced in markets where you could win.

Settlement delays (2-5 business days for international transactions) create working capital constraints that compound as you scale. Your customer pays on Monday. Your bank account receives funds on Friday. That float kills cash flow for mid-market SaaS companies operating on tight margins.

The Fundamental Problem

Traditional payment rails introduce multiple failure points between customer intent and successful payment: card network, issuing bank, acquiring bank, payment processor. Each intermediary adds latency, fees, and failure risk.

Every entity in that chain applies its own risk models, geographic restrictions, and operational constraints. Your customer’s payment passes through five systems before reaching your account, and if any single one fails, the transaction fails.

Stablecoins collapse that chain into direct settlement. No card networks. No correspondent banks. No processors applying opaque geographic blocks. Just cryptographic verification of payment finality, settling in minutes rather than days.

How Stablecoins Eliminate Payment Failures: The Technical Reality

Let’s be precise about what stablecoins are and what they’re not. USDC (USD Coin) is a digital representation of US dollars, backed 1:1 by US Treasury bills and verified monthly by Big Four accounting firms. Not Bitcoin. Not volatile cryptocurrency. Not speculation.

Think of USDC as digital wire transfers that settle in 10 minutes instead of 2-5 days, can’t be reversed once confirmed, and cost $5 instead of $25-45 per transaction. The technology is blockchain; the business application is payment infrastructure that eliminates traditional failure points.

Payment Finality: The Involuntary Churn Killer

When a customer pays via USDC, blockchain settlement creates immutable payment finality. Once the transaction confirms (average 10 minutes), it cannot be reversed, charged back, or decline due to insufficient funds discovered later.

Contrast with credit card payments: authorization happens instantly, but settlement occurs 2-5 days later. During that window, chargebacks reverse transactions, insufficient funds trigger failures, and fraud detection systems retroactively decline payments. Each represents a delayed involuntary churn event.

Stablecoin settlement has a 0% chargeback rate compared to 0.5-1% for traditional payment methods. Payment finality means what looks paid is paid. Your finance team doesn’t discover failed settlements three days after providing service.

Geographic Universality: Expanding Without Permission

A single USDC integration serves every international market simultaneously. No payment processor approval needed to accept customers from Lagos, Jakarta, São Paulo, or Kiev. The blockchain doesn’t impose geographic restrictions, it validates cryptographic signatures.

This eliminates the 15-25% transaction failure rate plaguing international markets. Your customer in Buenos Aires pays the same way as your customer in Boston. No foreign exchange fees eating 1-3% of transaction value. No processor declining transactions because their risk model flags Argentina.

For B2B SaaS targeting international growth, this represents the difference between hypothetical market opportunity and actual market access. You’re not asking Stripe for permission to serve customers in new geographies, you’re accepting payment from anyone with internet access.

Cost Structure: Making International Pricing Viable

Credit cards cost 2.9-4.5% per transaction, with international surcharges adding another 1-3%. Wire transfers cost $25-45 per transaction for B2B invoice settlement. These costs make international customer acquisition mathematically unprofitable for many SaaS businesses.

USDC transaction costs: 0.1-0.3% or flat $0.50-$5 depending on blockchain and processor. For a $500 monthly SaaS subscription, that’s $1.45 in credit card fees versus $0.50-$2.50 in USDC fees. For a $10,000 annual contract paid via wire transfer, that’s $35 wire fee versus $5 USDC settlement.

International payments see 50-80% cost reduction. For companies processing $1M+ annually in international transactions, that’s $30K-60K in annual savings, enough to fund the integration implementation and generate positive ROI within the first year.

Instant Settlement: Working Capital as Competitive Advantage

Traditional payment settlement takes 2-5 business days. Stablecoin settlement occurs in 10 minutes average. This difference transforms working capital management.

For SaaS companies with tight cash flow, instant settlement means subscription renewals generate usable cash the same day rather than three days later. Finance teams measure this as 12 basis point current ratio improvement, meaningful for mid-market companies operating on 30-45 day cash cycles.

Operationally, instant settlement enables immediate service restoration when payment methods fail. Traditional ACH retries require waiting 3-5 days to confirm success. USDC payment confirmation happens in minutes, allowing support teams to restore access immediately rather than asking customers to “wait 3-5 business days for the retry to process.”

Automated Recurring Billing: Eliminating Expiration Failures

Smart contracts enable automated subscription renewals without credit card expiration concerns. Rather than storing card details that expire every 3 years, customers authorize recurring USDC payments that execute automatically each billing cycle.

The technical mechanism: customers pre-approve spending limits from their USDC wallet. Each billing cycle, your system requests payment up to the approved amount. The blockchain verifies authorization and executes settlement, no manual intervention, no card updates, no expiration failures.

This directly addresses the 53% of payment failures attributed to expired or invalid card information. Cards expire. USDC wallets don’t. Pre-authorized payment agreements persist until explicitly revoked by the customer.

Predictable USD-pegged pricing eliminates currency volatility concerns that plague cryptocurrency payments. Your customer sees $500/month subscription price. They authorize $500 USDC payment monthly. No exchange rate fluctuations, no crypto speculation, no volatility risk.

Implementation: From Blockchain to Your Billing System

Here’s what Alex, the VP of Engineering managing 30 engineers at a $15M ARR B2B SaaS company, actually needs to know when his CFO forwards him another article about stablecoin payments with the subject line “Can we do this to reduce wire fees?”

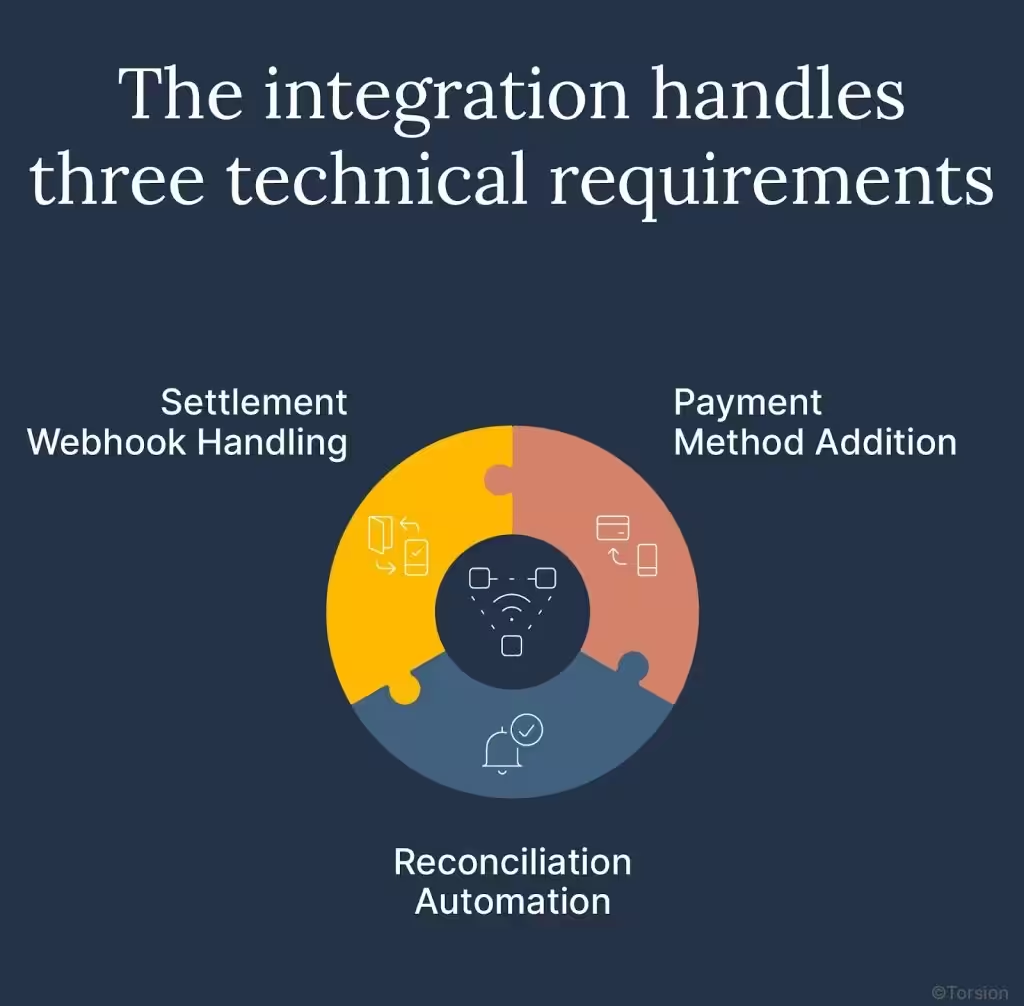

The Integration Architecture

Your team doesn’t rebuild billing infrastructure. Torsion builds an API layer connecting your existing billing system to a USDC processor, typically Circle or Coinbase Commerce. Your finance team keeps using NetSuite, SAP, QuickBooks, or Salesforce for invoice generation. Your engineering team keeps using Stripe or your custom payment stack for checkout flows.

1. Payment Method Addition: USDC appears as an additional payment option alongside credit cards and ACH. For B2B invoice settlement, this means adding a “Pay with USDC” button to invoices generated from NetSuite or SAP. For subscription checkout, this means USDC option in your existing Stripe integration or custom payment page.

2. Settlement Webhook Handling: When customers pay via USDC, blockchain confirmation triggers a webhook to your billing system updating payment status to “paid.” This requires handling blockchain-specific settlement confirmation logic, waiting for sufficient block confirmations, mapping USDC transaction IDs to invoice numbers, converting USDC amounts to USD at settlement exchange rate.

3. Reconciliation Automation: Finance teams receive daily reconciliation reports mapping USDC settlements to invoices, orders, or subscriptions in their existing format. This prevents the nightmare scenario where your accounting team manually tracks blockchain transactions in spreadsheets.

What Each Team Needs to Know

For Engineering Teams

Stack integration connects via REST API. Webhook endpoints receive settlement confirmations. Automated reconciliation maps USDC transactions to internal payment IDs. SOC2 Type II compliance and AML/KYC verification runs through Chainalysis or TRM Labs, not your infrastructure.

Code delivery happens through shared GitHub repository with complete technical documentation. Knowledge transfer ensures your team owns and maintains the integration post-launch, no vendor lock-in, no proprietary black boxes.

Implementation timeline depends on complexity: 1-2 weeks for simple integrations (adding USDC to existing Stripe checkout), 2-4 weeks for standard integrations (NetSuite or Salesforce billing, custom checkout), 4-6 weeks for complex integrations (SAP or legacy ERP systems, multiple use case implementations).

For Finance Teams

Accounting treatment: stablecoins classified as cash equivalents, not crypto assets on your balance sheet. This matters enormously for audit and financial reporting. You’re not holding cryptocurrency investments subject to volatile mark-to-market accounting. You’re receiving payment that settles to USD in your bank account.

Reconciliation reports deliver USDC transaction IDs mapped to invoices with USD-equivalent values for journal entries. Accounting systems (NetSuite, QuickBooks, SAP) receive automated journal entries in their native format: Debit Cash (USDC settlement) / Credit Accounts Receivable.

Audit trail includes blockchain transaction IDs (immutable proof of settlement), processor confirmation timestamps, bank deposit records, and reconciliation reports. This creates superior audit documentation compared to traditional wire transfers, which pass through opaque correspondent banking networks.

Tax reporting handles 1099 generation automatically where applicable, critical for companies paying contractors or suppliers via USDC.

For Compliance and Legal Teams

Regulatory framework clarity: GENIUS Act (US federal stablecoin regulation, effective July 2025) and MiCA (EU stablecoin regulation) provide clear legal frameworks. Circle and major USDC processors operate as regulated payment service providers, not unregulated cryptocurrency exchanges.

KYC requirements match standard business banking: same documentation required for opening a business bank account or Stripe merchant account. Transaction monitoring runs automatically through Chainalysis or TRM Labs, generating alerts for suspicious activity.

Quarterly compliance reporting auto-generates, covering AML monitoring, transaction patterns, and regulatory documentation needed for audits. This removes compliance burden from your legal team, they review reports rather than building monitoring infrastructure.

Three Common Implementation Paths

Path 1: International Checkout Recovery (2-3 weeks)

Use case: Recovering 5-10% of international transactions currently lost to processor geographic blocks.

What gets built: USDC payment option added to existing checkout (Stripe or custom stack). Customers see USD pricing; backend settles USDC automatically. Integration handles refunds, settlement confirmation, and daily reconciliation.

Deliverables: Payment method integration, settlement webhooks, fiat pricing display, refund flow, reconciliation reports.

Path 2: B2B Invoice Settlement (3-4 weeks)

Use case: Eliminating $30K-60K annual wire transfer fees for international B2B invoices.

What gets built: USDC payment option added to invoices generated from NetSuite, SAP, QuickBooks, or Salesforce. Payment webhooks trigger automatic “paid” status update. Finance receives reconciliation reports in existing format.

Deliverables: Billing system integration, invoice payment option, webhook automation, reconciliation reporting.

Path 3: Instant Refund Processing (2-3 weeks)

Use case: Reducing support ticket volume from “where’s my refund?” inquiries. ACH refunds take 5-10 business days; USDC refunds settle in 10 minutes.

What gets built: Customers choose instant USDC refund versus standard 5-10 day ACH. Support dashboard tracks refund status. Finance reporting includes USDC refunds in standard format.

Deliverables: Opt-in flow, wallet handling, refund processing, support dashboard, reconciliation.

Compliance Infrastructure: What Torsion Handles

The integration includes compliance infrastructure your team doesn’t need to build:

- AML/KYC setup with USDC processor (Circle or Coinbase Commerce)

- Transaction monitoring configuration through Chainalysis or TRM Labs

- Suspicious activity reporting protocols and alert templates

- Regulatory audit documentation aligned with GENIUS Act and MiCA frameworks

This matters because most engineering teams lack cryptocurrency compliance expertise. Building this infrastructure internally requires specialized knowledge your team doesn’t have and doesn’t want to acquire. Torsion delivers turnkey compliance that passes SOC2 audits and satisfies regulators.

Measuring Impact: Calculating Your Involuntary Churn Reduction

Engineering leaders need specific metrics proving stablecoin integration delivers ROI. Here’s how to calculate expected impact for your business.

The Four Metrics That Matter

Metric 1: Payment Failure Rate by Geography

Baseline: Credit card failure rate averages 15%, climbing to 15-25% in international markets (Latin America, Southeast Asia, Africa).

Target: Stablecoin transactions achieve near-zero failure rate post-settlement due to payment finality.

Measurement: Track payment success rate by country before and after offering USDC payment option. Focus on markets with currently high decline rates, these show largest improvement.

Metric 2: Recovery Rate from Failed Payments

Baseline: 70% recovery rate with optimized dunning sequences and retry logic.

Target: 95%+ recovery when offering USDC as alternative payment option after initial card failure.

Measurement: When primary payment method fails, offer USDC as alternative before entering dunning sequence. Track what percentage of failed payments convert to successful USDC payments.

Metric 3: Involuntary Churn Rate

Baseline: 0.8% monthly involuntary churn for average B2B SaaS.

Target: 0.3-0.4% reduction from payment failure elimination (50% involuntary churn reduction).

Measurement: Separate involuntary churn (attributed to payment failures) from voluntary churn (customer-initiated cancellations). Track involuntary churn rate monthly before and after USDC implementation.

Metric 4: International Customer Retention

Baseline: 5-10% transaction loss in blocked or high-decline international markets.

Target: 80-90% recovery of previously declined international transactions.

Measurement: Track conversion rate in international markets before and after USDC payment option. Focus on previously blocked geographies where processor restrictions created hard barriers.

Sample ROI Calculation

Company Profile

- $10M Annual Recurring Revenue

- 0.8% monthly involuntary churn ($80K annual loss)

- 60% of involuntary churn from payment failures ($48K)

- 30% of failed payments unrecoverable by dunning ($14.4K)

After USDC Implementation

- USDC payment option offered to international customers with payment failures

- 70% of previously unrecoverable payment failures resolved ($10K annual recovery)

- 5% conversion improvement on international traffic from reduced processor blocks ($25K-50K new ARR)

- Implementation cost: $15K-25K for fixed-scope integration

First-Year Financial Impact

- Direct involuntary churn reduction: $10K

- International market expansion: $25K-50K

- Wire fee reduction (if processing B2B payments): $15K-30K

- Total first-year impact: $50K-90K

- Payback period: 2-4 months

This calculation focuses exclusively on involuntary churn and international expansion. Additional benefits, wire fee reduction, working capital improvement from instant settlement, reduced payment processing costs, compound ROI but aren’t necessary to justify implementation.

Addressing the Concerns Your CFO Will Raise

When Alex presents this to his CFO and CTO, three questions always surface. Here are the answers technical leaders need.

“Do customers actually want to pay with stablecoins?”

The better question: do customers in blocked markets want access to your product? The answer is overwhelmingly yes.

Many USDC customers are new customers previously unable to subscribe due to payment processor restrictions. They’re not choosing USDC over credit cards because they love cryptocurrency, they’re choosing USDC because it’s their only payment option that works.

Presentation matters. Customers see USD pricing. USDC settlement happens on the backend. For subscription businesses, this means customers understand they’re paying $500/month, not 500 USDC. The blockchain mechanics remain invisible to end users.

Stablecoins processed $14 trillion in 2024, institutional adoption has crossed the legitimacy threshold. This isn’t experimental technology. It’s payment infrastructure mature enough that Stripe enabled recurring stablecoin payments in October 2025.

“What if the stablecoin ‘breaks’ or de-pegs?”

USDC is backed 1:1 by US Treasury bills, verified monthly by Big Four accounting firms. Reserve audits occur more frequently than most commercial banks. Major stablecoins (USDC and USDT) haven’t de-pegged meaningfully in three years of operation.

More importantly, same-day settlement means you have no long-term exposure. Unlike holding cryptocurrency as an investment, USDC payment settlement converts to USD in your bank account within hours. You’re not speculating on stablecoin stability, you’re using it as a payment rail.

The risk profile resembles foreign currency transactions more than crypto investment. When you accept payment in euros and convert to dollars, brief currency fluctuation risk exists during conversion. USDC settlement carries similar brief exposure (minutes rather than days), but the 1:1 USD peg minimizes even that risk.

“Our finance team doesn’t understand crypto”

They don’t need to. Torsion’s integration handles all blockchain complexity. Finance teams receive standard USD-denominated reports, journal entries in their existing ERP format, and reconciliation workflows identical to processing credit cards or ACH.

Accounting treatment classifies stablecoins as cash equivalents, not crypto assets. This means no volatile cryptocurrency accounting on balance sheets, no mark-to-market adjustments, no specialized crypto accounting expertise required. Finance teams treat USDC settlements exactly like foreign currency transactions, record at USD-equivalent value on settlement date.

The integration exists precisely to prevent your finance team from needing cryptocurrency knowledge. They interact with familiar systems (NetSuite, QuickBooks, SAP) receiving familiar reports (transaction IDs, amounts, dates, reconciliation statements). The blockchain layer remains invisible.

“What about regulatory compliance?”

GENIUS Act (US federal stablecoin framework, effective July 2025) and MiCA (EU stablecoin regulation) provide clear regulatory guidelines. Circle and major USDC processors operate as regulated payment service providers, subject to the same AML and KYC requirements as traditional payment processors.

Your compliance requirements match opening a business bank account: standard KYC documentation, transaction monitoring (automated through Chainalysis), quarterly compliance reporting (auto-generated).

The integration includes regulatory infrastructure, AML monitoring, transaction screening, suspicious activity reporting protocols, managed by the payment processor and integration layer, not your compliance team. This removes compliance burden rather than creating new obligations.

For enterprise companies with SOC2, HIPAA, or industry-specific requirements, the integration architecture supports existing compliance frameworks. SOC2 Type II certification, healthcare payment compliance, financial services regulatory requirements all map to existing USDC processor capabilities.

“Is this worth the engineering effort?”

Implementation timeline: 2-4 weeks typical. Integration connects to existing billing systems rather than replacing infrastructure. Code ownership post-implementation means no vendor dependency.

ROI payback period: 2-4 months from involuntary churn reduction alone, before counting international expansion revenue or wire fee savings.

The real question isn’t whether stablecoin integration is worth engineering effort. The question is whether DIY implementation makes sense versus fixed-scope implementation partner. Building this internally takes 8-12 weeks (often stretching to 14-16 with unforeseen blockchain complexity), requires specialized cryptocurrency knowledge your team doesn’t have, and still leaves gaps in compliance infrastructure.

Fixed-scope integration delivers working code in 2-4 weeks with compliance included. Your team spends 2-3 weeks in technical review and integration testing rather than 12-16 weeks building from scratch.

The Competitive Shift: Payment Reliability as Product Differentiation

We’re watching a competitive shift happen in real-time. Early-adopting SaaS companies offering stablecoin payments capture international markets their competitors cannot serve. Payment reliability transitions from operational concern to product differentiation.

When your competitor advertises “payment success in 150+ countries” and you’re constrained by payment processor geographic blocks, that’s not a feature gap, it’s a market access gap. When they close international enterprise deals with instant settlement and you quote 2-5 day payment clearing, that’s a competitive disadvantage disguised as payment infrastructure.

The Strategic Calculation

For SaaS companies with high involuntary churn from payment failures (>0.5% monthly), stablecoin integration delivers immediate ROI. The 8.6% first-year revenue increase from fixing involuntary churn alone justifies implementation cost and engineering effort.

For companies with significant international customer base (>15% revenue from outside North America), stablecoins unlock geographic expansion opportunities traditional processors block. Markets your team marked as “future consideration due to payment constraints” become immediately addressable.

For B2B companies with enterprise customers, invoice settlement via USDC eliminates wire fees and accelerates cash conversion. Finance teams measuring days sales outstanding (DSO) see material improvement when settlement compresses from 2-5 days to same-day.

The Market Momentum

Stripe enabled recurring stablecoin payments in October 2025. Coinbase Commerce, Circle, and Fireblocks all launched enterprise payment infrastructure in the past 18 months. The regulatory framework solidified with GENIUS Act passage in July 2025. Institutional adoption crossed the tipping point.

This isn’t speculative blockchain technology anymore. It’s payment infrastructure that processed $14 trillion in 2024, supported by regulated processors, integrated into familiar platforms like Stripe, and adopted by CFOs at Fortune 500 companies.

The Question That Determines Action

Calculate your current involuntary churn rate attributed specifically to payment failures (not product dissatisfaction). Identify what percentage of your revenue comes from international markets where payment processor blocks or high decline rates constrain growth.

If involuntary churn costs you $50K+ annually, or international payment failures block $100K+ in potential revenue, stablecoin integration delivers ROI in the first year.

The decision isn’t whether stablecoins will reduce involuntary churn, the payment finality mechanism makes that mathematically certain. The decision is whether your competitors will adopt this infrastructure before you do, capturing the international customers and enterprise accounts your payment processor currently blocks you from serving.

Next Steps: From Research to Implementation

You’ve identified involuntary churn as a revenue problem. You’ve quantified the cost of payment failures in your business. You’ve calculated potential ROI from stablecoin integration. Now what?

Calculate Your Specific Impact

Start with data:

- Current monthly involuntary churn rate (separate from voluntary churn)

- Percentage attributed to payment failures versus other causes

- International revenue as percentage of total (and decline rates by geography)

- B2B wire transfer volume and annual fees (if applicable)

These four numbers determine whether stablecoin integration makes strategic sense for your business now versus later.

Assess Integration Complexity

Review your billing infrastructure:

- What system generates invoices or processes subscriptions? (NetSuite, SAP, QuickBooks, Stripe, custom)

- What payment methods do you currently support? (Credit card, ACH, wire transfer)

- How does your finance team reconcile payments today? (Automated vs. manual)

- What compliance frameworks apply? (SOC2, HIPAA, financial services regulations)

Integration complexity determines timeline (2-4 weeks standard, up to 6 weeks for complex implementations) and cost.

Build Internal Alignment

Stablecoin integration requires cross-functional buy-in:

Engineering: Needs confidence that integration won’t create technical debt or require ongoing cryptocurrency expertise

Finance: Needs clarity on accounting treatment, reconciliation processes, and audit trail quality

Compliance: Needs assurance on regulatory frameworks (GENIUS Act, MiCA) and AML/KYC infrastructure

Revenue Operations: Needs proof that payment reliability will reduce involuntary churn measurably

The business case connects these concerns: quantified revenue impact (involuntary churn reduction + international expansion) exceeds implementation cost with 2-4 month payback period.

Implementation Partner Selection

You have three paths:

1. DIY Implementation: 8-12 weeks engineering effort, requires blockchain expertise, compliance gaps likely

2. Generic Consulting Firm: $150K-$300K, delivers documentation not working code, ongoing support uncertain

3. Fixed-Scope Integration Partner: 2-4 weeks timeline, working code with compliance included, team owns infrastructure post-launch

Torsion builds USDC payment integrations with Stripe, NetSuite, SAP, and QuickBooks in 2-4 weeks. API layer handles blockchain settlement; your team keeps existing processes. Fixed scope, you own the code.

Technical assessment evaluates your specific billing stack, use case priorities, and integration complexity. No commitment required, just clarity on whether stablecoins solve your specific involuntary churn problem and what implementation would actually entail.

The Involuntary Churn Problem Is Solvable

Involuntary churn isn’t an inevitable cost of doing business. It’s an infrastructure problem with an infrastructure solution.

Traditional payment rails, card networks, correspondent banks, payment processors, introduce failure points between customer intent and successful payment. Each intermediary applies geographic restrictions, charges fees, imposes settlement delays, and creates decline risk.

Stablecoins collapse that chain into direct settlement. Payment finality eliminates chargebacks and delayed failures. Geographic universality removes processor blocks. Instant settlement improves cash flow. Automated recurring billing prevents expiration failures.

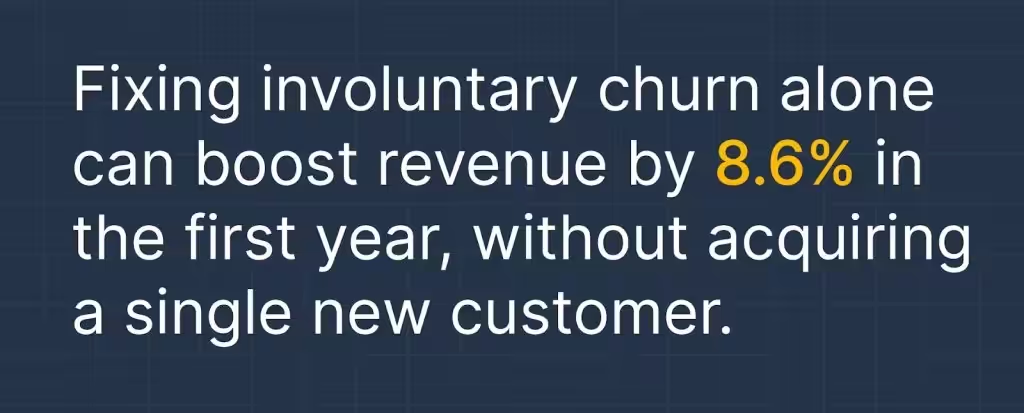

The data is unambiguous: fixing involuntary churn delivers 8.6% first-year revenue increase without acquiring a single new customer. For a $10M ARR SaaS company, that’s $860K. For a $50M ARR company, that’s $4.3M.

Your engineering team spent months optimizing product. Your customer success team nurtures relationships. Your RevOps team perfects retention playbooks. Now solve the infrastructure failure silently undoing that work.

The question isn’t whether stablecoins reduce involuntary churn. The question is whether your payment infrastructure will remain a competitive disadvantage while your competitors solve the problem.

Explore USDC Payment Integration for Your SaaS

Torsion builds stablecoin payment integrations with your existing billing systems in 2-4 weeks. REST API layer handles blockchain settlement, your team keeps existing workflows, you own the code post-implementation.

Schedule Technical Assessment →

What payment challenge costs you the most?

☐ High involuntary churn from payment failures (>0.5% monthly)

☐ International transaction declines blocking market expansion

☐ B2B wire transfer fees ($30K-60K+ annually)

☐ Slow settlement creating cash flow constraints

Technical assessment evaluates your billing stack, involuntary churn sources, and integration complexity. 30-minute consultation delivers specific timeline and ROI calculation for your business.