TL;DR

- SEC April 4, 2025 guidance confirmed non-security status for qualifying stablecoins with 1-to-1 USD backing

- GENIUS Act July 2025 requires $1 high-liquid reserves per stablecoin with monthly Big 4 attestations

- 9 of 11 major stablecoins meet IFRS cash equivalent criteria under IAS 7

- 70% cart abandonment with 13% due to payment unavailability: stablecoin checkout integration delivers documented 25% abandonment reduction

- Instant settlement eliminates 2-5 day working capital float improving current ratios 10-15 basis points.

- Blockchain audit trails superior to traditional documentation, immutable transaction records with same-day ERP reconciliation

- 23% of CFOs expect stablecoin adoption within 2 years (39% for $10B+ companies)

Suppose a customer in Jakarta abandons their cart because PayPal doesn’t operate domestically in Indonesia. The e-commerce platform loses a $250 sale that cost $50 in customer acquisition.

Six months later, that same platform processes thousands of similar transactions through stablecoin payment infrastructure. Those payments now appear on the balance sheet as cash equivalents, improving the current ratio by 12 basis points, enough to satisfy a bank covenant that was uncomfortably close to threshold.

The SEC’s April 4, 2025 staff statement on stablecoins didn’t just clarify securities classification. It completed a transformation from payment obstacle to balance sheet optimization opportunity.

SEC April 2025 guidance signals stablecoins could qualify as cash equivalents, transforming payment infrastructure into balance sheet assets.

For CFOs managing international operations, this represents more than payment efficiency. It’s the convergence of customer conversion improvement (25% cart abandonment reduction documented in implementations), working capital optimization (eliminating 2-5 day settlement delays), and balance sheet classification clarity under evolving regulatory frameworks.

The question isn’t whether stablecoins will achieve mainstream financial statement integration. The regulatory evolution and accounting standards development suggest they will. The question is whether your balance sheet will be positioned to capture the optimization benefits as this transformation accelerates.

The Cart Abandonment Revenue Reality: Quantifying the Customer Conversion Problem

Before discussing balance sheet treatment, let’s establish the revenue impact that motivates payment infrastructure modernization.

The 70% Abandonment Baseline

Global E-commerce Conversion Data:

Average cart abandonment sits at 69.99% across all e-commerce platforms, meaning only 3 out of 10 shoppers complete purchases. Within that 70% abandonment rate, payment method unavailability accounts for 13% of lost conversions. Payment security concerns drive another 17% to abandon, while data security doubts account for 19%.

This isn’t theoretical revenue impact. For a business generating $10 million annually in completed e-commerce transactions, that 70% abandonment rate represents approximately $23 million in lost sales opportunities at the same conversion rate.

Payment Method Regional Variation

Consumer payment preferences vary dramatically by geography. US consumers split preferences: 29% debit cards, 28% credit cards, 20% cash, 11% direct payments, 12% alternative methods. But international markets show different patterns and Thailand sees 35% cash-on-delivery preference versus 25% card payments.

When payment infrastructure doesn’t match regional preferences, conversion suffers. A Southeast Asian customer encountering a US-only payment processor sees no checkout option matching their preferred method. They abandon. The platform loses the transaction and the customer acquisition cost invested to bring them to checkout.

Stablecoin Conversion Improvement Evidence

Documented Implementation Results:

E-commerce platforms implementing stablecoin checkout integration report 25% reduction in cart abandonment rates. This isn’t marginal improvement, it’s measurable revenue capture from customers who previously had no viable payment method.

The mechanism is straightforward: stablecoin infrastructure accepts local currency through conversion partners, processes payment through blockchain rails independent of traditional processor geographic limitations, and settles to the merchant in stablecoin or converted fiat based on preference.

Cross-Border Customer Economics:

International customers often represent higher transaction values and lifetime values than domestic customers. When payment processor limitations block these higher-value conversions, the revenue impact exceeds the simple abandonment percentage. Lost international conversions cost more than lost domestic ones.

For businesses operating in markets where traditional processors don’t adequately serve customers, stablecoin payment acceptance isn’t an optimization, it’s a requirement for market access.

April 4, 2025: The Regulatory Turning Point

The path from payment method to cash equivalent classification depends on regulatory clarity that didn’t exist before 2025. Two regulatory developments transformed the landscape.

SEC Staff Statement: Clarity on Securities Status

The Non-Security Declaration:

On April 4, 2025, SEC staff issued a statement providing the clarity enterprise CFOs needed: qualifying “Covered Stablecoins” do NOT constitute securities under federal securities laws.

This four-part test creates clear boundaries. Stablecoins meeting these criteria operate as payment instruments, not investment securities. That distinction matters enormously for balance sheet classification.

What Changed for CFOs:

Before April 2025, CFOs faced uncertainty about whether holding stablecoins for payment operations created securities holdings requiring different accounting treatment and regulatory oversight. The SEC statement eliminated that ambiguity for qualifying stablecoins.

Bloomberg subsequently reported that this guidance signals stablecoins could qualify as cash equivalents under specific conditions. A massive shift in accounting treatment potential that moves stablecoins from “digital assets” to “cash and cash equivalents” on balance sheets.

GENIUS Act: The Federal Framework Foundation

Federal Legislation Signed July 18, 2025:

The GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins) provides comprehensive federal regulatory structure for payment stablecoins.

Payment Stablecoin Definition:

The Act defines payment stablecoins as digital assets issued for payment or settlement purposes, redeemable at predetermined fixed amounts. This legal definition separates payment infrastructure from speculative cryptocurrency.

Reserve Requirements:

Issuers must maintain at least $1 of permissible high-liquid reserves per stablecoin issued. Permissible reserves include US dollars and short-term Treasury bills, the same high-quality liquid assets that support cash equivalent classification under accounting standards.

Audit and Disclosure Obligations:

Monthly disclosures of outstanding stablecoins and reserve composition, routine auditing by registered public accounting firms, and executive certification requirements create transparency similar to traditional banking disclosures.

GENIUS Act reserve requirements mirror cash equivalent criteria, $1 in high-liquid reserves per stablecoin issued.

For businesses with $50 billion or more in reserves, the Act requires US GAAP audited financial statements, demonstrating the legislation’s integration with established accounting frameworks rather than creating parallel standards.

Cash Equivalent Classification: The Accounting Standards Evolution

With regulatory clarity established, the accounting treatment question becomes central: how do CFOs classify stablecoins on enterprise balance sheets?

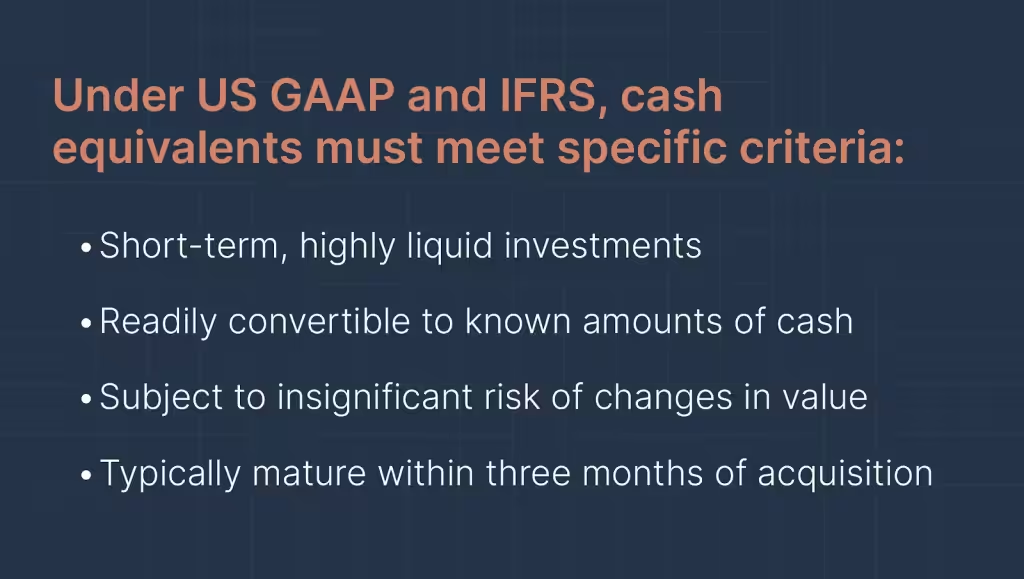

The Cash Equivalent Criteria Framework

Stablecoins designed to maintain 1-to-1 USD peg with on-demand redemption at par meet the “readily convertible to known amounts” and “short-term” requirements. The question becomes whether 1-to-1 reserve backing and redemption mechanisms satisfy “insignificant risk” criteria.

IFRS Analysis: 9 of 11 Stablecoins Qualify

Academic Research on International Standards:

Research examining major fiat-backed stablecoins against IAS 7 cash equivalent requirements found that 9 of 11 analyzed stablecoins meet objective requirements for cash equivalent classification under IFRS.

The key factors supporting classification:

- Contractual right to receive fixed or determinable amount

- On-demand redemption at par value

- Reserve backing by high-quality liquid assets

- Minimal credit risk from issuer default

MiCAR Regulatory Alignment:

Europe’s Markets in Crypto-Assets regulation, implemented in 2025, aligns with IFRS accounting practices. MiCAR requires stablecoin issuers to maintain verifiable reserves and undergo regular audits, creating regulatory structure that supports cash equivalent accounting treatment.

US GAAP Evolution Under GENIUS Act

Financial Asset Classification Potential:

Payment stablecoins meeting GENIUS Act criteria may qualify as financial assets under US GAAP because of redemption requirements at predetermined fixed amounts backed by high-liquid reserves.

Current Accounting Status:

Under current GAAP, stablecoins are not automatically classified as cash, though treatment is evolving. FASB’s 2025 digital asset accounting standards require fair value measurement for certain digital assets, but payment stablecoins with fixed redemption rights may receive different treatment.

Classification Options Available:

CFOs evaluating stablecoin accounting treatment have three primary classification paths:

- Cash and cash equivalents – if meeting liquidity, maturity, and risk criteria

- Short-term investments or financial instruments – measured at fair value or amortized cost

- Digital assets – under FASB’s 2025 fair value measurement guidance for crypto assets

The appropriate classification depends on specific stablecoin characteristics, business model for holding them, and redemption mechanisms available.

Balance Sheet Integration: From Revenue Capture to Financial Optimization

Once accounting classification is established, the operational and financial statement impacts become measurable.

Working Capital Transformation Through Instant Settlement

The Traditional Settlement Delay Problem:

Standard international payment processing creates 2-5 day gaps between transaction initiation and final settlement. During those days, capital is in transit and it’s neither available for operations nor reflected on the balance sheet as liquid assets.

For businesses processing significant international payment volume, this creates persistent working capital inefficiency. $500,000 constantly in transit represents capital that could otherwise deploy strategically or improve liquidity ratios.

Stablecoin Instant Settlement Impact:

Same-day settlement eliminates the working capital float. Payments received through stablecoin infrastructure settle immediately, appearing on the balance sheet the same day rather than 2-5 days later.

Quantified Balance Sheet Impact:

For a business with $10 million monthly international payment volume and 3-day average settlement delay, traditional systems keep approximately $1 million constantly in transit. Instant settlement frees that capital, improving:

- Current ratio by eliminating settlement float from working capital calculations

- Quick ratio through immediate access to liquid assets

- Cash conversion cycle by accelerating the receivables-to-cash timeline

Research shows companies can improve earnings by 5-10% through balance sheet optimization, with working capital efficiency as a primary lever.

The ERP Reconciliation Gap Solution

Traditional Accounting Challenge:

Traditional payment systems create reconciliation complexity. Your ERP records the transaction at initiation. The bank settles 2-5 days later. During that gap, your accounting team reconciles in-transit payments that haven’t reached final settlement.

This creates manual accounting work, audit complexity, and working capital reporting challenges. Which transactions are truly liquid assets versus in-transit payments? How do you report cash position when significant amounts sit in multi-day settlement processes?

Blockchain Audit Trail Advantage:

Stablecoin transactions provide immutable blockchain records that link directly to ERP entries. Transaction initiation equals settlement equals balance sheet recognition, all on the same day with unified data trails.

This eliminates the reconciliation gap. Finance teams don’t track in-transit payments across multiple days and systems. The blockchain transaction ID provides permanent, verifiable proof of settlement that auditors can independently confirm.

Instant settlement eliminates the 2-5 day reconciliation gap with transaction, settlement, and balance sheet recognition happening simultaneously.

From an internal control perspective, this enhances SOX compliance. The audit trail is superior to traditional payment documentation, settlement timing is immediate rather than uncertain, and reconciliation becomes automated rather than manual.

Real-World Implementation: Customer Conversion to Balance Sheet Optimization

Abstract accounting discussions matter less than concrete implementation examples showing how businesses bridge customer conversion improvements with balance sheet integration.

E-commerce Platform: Southeast Asia Market Entry

The Customer Conversion Challenge:

An e-commerce platform targeting Southeast Asian customers faced 70%+ cart abandonment rates in markets where PayPal operates with restrictions and Stripe isn’t available. Customer acquisition costs were substantial, $40-60 per customer, making abandoned carts at checkout particularly painful.

Stablecoin Integration Implementation:

The platform integrated stablecoin checkout accepting local currencies through regional conversion partners. Customers pay in Indonesian rupiah, Philippine pesos, or Thai baht. The platform receives stablecoin settlement, then converts to USD for balance sheet reporting or holds in stablecoin as cash equivalent.

Measurable Results:

- Cart abandonment reduction: 25% improvement (from 72% to 54% in pilot markets)

- Settlement timing: Same-day vs. previous 3-5 day timeline

- Working capital improvement: $800K freed from payment float for $15M monthly volume

- Balance sheet treatment: Stablecoin holdings classified as cash equivalents pending auditor review

Financial Statement Impact:

The current ratio improved by 15 basis points from working capital optimization. More importantly, the platform captured revenue from previously abandoned international carts. Approximately $1.8M annually in incremental sales from Southeast Asian markets.

B2B Marketplace: Supplier Payment Optimization

Cross-Border Payment Inefficiency:

A B2B marketplace connecting buyers with international suppliers processed $5 million monthly in supplier payments. Traditional wire transfers cost $45-140 per transaction with 2-5 day settlement, creating supplier relationship friction and working capital inefficiency.

Stablecoin Payment Rails:

The marketplace shifted to stablecoin supplier payments. Suppliers receive instant settlement at transaction costs below $5. The marketplace maintains stablecoin treasury positions that classify as cash equivalents, improving balance sheet liquidity presentation.

Operational and Financial Outcomes:

- Payment cost reduction: 80%+ savings on per-transaction fees

- Settlement timing: Instant vs. 2-5 days improves supplier satisfaction

- Working capital: $400K average reduction in payment float

- Balance sheet: Stablecoin treasury classified as cash equivalent improves quick ratio

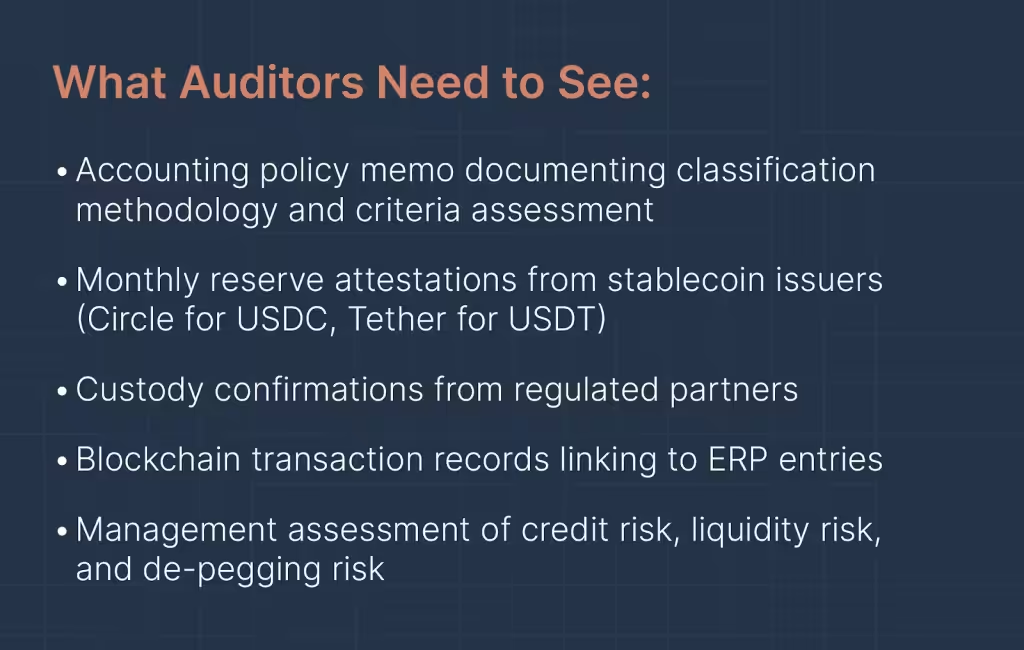

Audit Documentation:

The marketplace provides external auditors with blockchain transaction records, monthly reserve attestations from stablecoin issuers, and custody confirmations from regulated partners. Audit documentation is more comprehensive than traditional banking records, reducing audit complexity and fees.

The CFO Audit and Compliance Framework

Balance sheet optimization matters only if it maintains audit opinion cleanliness and regulatory compliance. Here’s the framework CFOs implement for stablecoin financial statement integration.

Financial Statement Disclosure Requirements

GENIUS Act Monthly Reporting:

For stablecoin issuers, the Act requires monthly disclosures of outstanding stablecoins and reserve composition. These reports must be certified by company executives and examined by registered public accounting firms.

For businesses holding stablecoins for payment operations (not issuing them), disclosure focuses on balance sheet classification methodology, accounting policy elections, and any material exposures.

Balance Sheet Presentation:

If classified as cash equivalents, stablecoins appear in the “Cash and cash equivalents” line item with footnote disclosure of composition. If classified as short-term investments, they appear separately with fair value or amortized cost measurement disclosure.

Income Statement Impact:

Transaction fee expenses appear in operating expenses, similar to traditional payment processing fees. Any FX gain/loss from stablecoin conversion appears in other income/expense. For stablecoins held at fair value, any value changes flow through the income statement.

Cash Flow Statement Classification:

Stablecoin payment receipts likely classify as operating cash flows. Purchases of stablecoins for treasury purposes may classify as investing activities depending on business model and accounting policy election.

Internal Control Design for SOX Compliance

Custody and Security Controls:

Enterprise stablecoin holdings require institutional custody solutions with SOC2 Type II certification. Treasury teams don’t manage private keys directly as the regulated custodians handle technical blockchain operations while CFOs maintain control through approval workflows.

Transaction Authorization Framework:

Spending limits by role and transaction type mirror traditional payment controls. Large stablecoin transfers require multi-signature approval. Segregation of duties separates transaction initiation from approval, just like traditional treasury controls.

Reconciliation Procedures:

Daily reconciliation of blockchain transactions to ERP records. Monthly verification that stablecoin balances per custody statements match general ledger. Quarterly attestation review from stablecoin issuers confirming reserve backing.

Risk Monitoring Processes:

Continuous monitoring of stablecoin market prices for sustained de-pegging. Monthly review of issuer reserve attestations. Quarterly assessment of custody partner financial health and regulatory status. Annual evaluation of accounting classification appropriateness.

External Audit Considerations

Reserve Backing Verification:

Major stablecoins maintain Big 4 accounting firm attestations. USDC holds 61% in cash and government money market funds, 12% in US Treasuries, with monthly Grant Thornton attestations. USDT provides regular reserve reports.

Auditors review these third-party attestations rather than auditing stablecoin issuer reserves directly. The monthly frequency provides more frequent verification than most banking relationships require.

Control Testing:

Auditors test internal controls over stablecoin transactions similarly to traditional payment controls: authorization effectiveness, reconciliation accuracy, segregation of duties, system access restrictions, and physical/logical security of custody arrangements.

The key difference: blockchain transaction records are immutable and independently verifiable. Auditors can confirm transactions on public blockchains without relying solely on company records or bank confirmations.

Risk Management: The De-Pegging Question and Credit Assessment

CFOs implementing stablecoin treasury operations face a question from audit committees, external auditors, and risk management functions: what happens if a stablecoin “de-pegs” from its dollar value?

Historical Stability Analysis

Established Stablecoin Performance:

USDC and USDT have maintained price stability over multi-year operational histories processing trillions in transaction volume. Temporary price deviations from $1.00 have been minimal and brief, typically measured in fractions of a cent for minutes or hours rather than sustained de-pegging.

Reserve Backing Mechanics:

The 1-to-1 reserve backing creates economic incentive for price stability. If price drops below $1.00, arbitrageurs purchase stablecoins and redeem for $1.00 of reserves, profiting from the spread while pushing price back to peg. If price rises above $1.00, issuers mint new stablecoins against reserves, increasing supply and pushing price down.

This arbitrage mechanism works when reserves are genuine, liquid, and redeemable on demand which are the exact requirements GENIUS Act mandates.

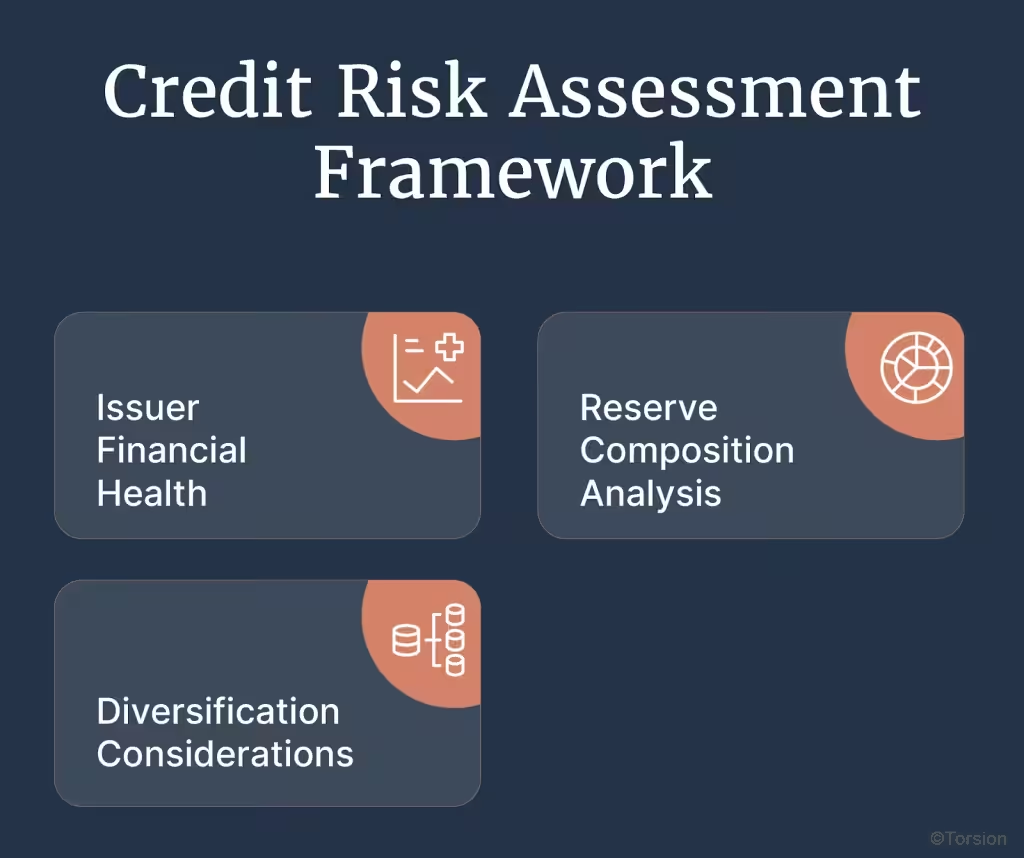

Credit Risk Assessment Framework

Issuer Financial Health:

Credit risk in stablecoin holdings comes from issuer inability to redeem at par. CFOs evaluate issuer financial health similarly to bank counterparty risk assessment: reserve adequacy, audit quality, regulatory compliance, operational track record, and financial condition of the issuing entity.

Reserve Composition Analysis:

Not all reserves are equal. USDC’s 61% in cash and government money market funds plus 12% in US Treasuries represents extremely high-quality liquid assets. These reserves can convert to cash immediately to support redemptions without liquidation risk.

Lower-quality reserves (corporate debt, longer-maturity securities, less liquid assets) create more credit and liquidity risk. GENIUS Act restricts permissible reserves to US dollars and short-term Treasury bills specifically to minimize these risks.

Diversification Considerations:

Some enterprises diversify stablecoin holdings across multiple issuers rather than concentrating with one. This mirrors traditional banking practice of maintaining relationships with multiple banks to diversify counterparty risk.

For large enterprises, maintaining both USDC and USDT positions provides issuer diversification while still benefiting from instant settlement and potential cash equivalent classification.

The Financial Statement Optimization Opportunity

Beyond accounting classification mechanics, stablecoin integration creates measurable balance sheet and income statement improvements.

Liquidity Ratio Enhancement

Current Ratio Improvement:

Stablecoins classified as cash equivalents appear in current assets with immediate liquidity. Traditional payment systems keep capital in 2-5 day settlement float that may or may not count as current assets depending on settlement timing uncertainty.

For businesses near bank covenant thresholds requiring minimum current ratios, even small improvements matter. A 10-15 basis point current ratio improvement from eliminated settlement float can create covenant compliance buffer.

Quick Ratio Impact:

The quick ratio (cash + receivables + marketable securities / current liabilities) measures immediate liquidity. Stablecoins with instant settlement and cash equivalent classification improve quick ratios more than traditional receivables that take days or weeks to convert to cash.

For businesses where quick ratio serves as key liquidity metric for investors or lenders, this improvement enhances financial presentation without requiring operational changes beyond payment infrastructure.

Working Capital Cycle Optimization

Cash Conversion Cycle Acceleration:

The cash conversion cycle measures days from cash outflow for inventory/services to cash inflow from sales. Faster payment settlement directly accelerates this cycle.

Traditional international payments adding 2-5 days to the cash-to-cash cycle extend working capital requirements. Instant settlement through stablecoin infrastructure eliminates those days, improving working capital efficiency without changing underlying business operations.

Balance Sheet Efficiency Research:

Studies show companies can improve earnings by 5-10% through balance sheet optimization, with working capital management as a primary driver. Eliminating settlement delays represents one lever for this optimization. Not transformative alone, but meaningful when combined with other efficiency improvements.

Income Statement Benefits

Transaction Cost Reduction:

Stablecoin payment processing runs at sub-1% transparent transaction costs versus 3-8% total costs for traditional international payments including wire fees, FX markups, and intermediary charges. This directly improves gross margins.

For a business processing $50 million annually in international payments, reducing total costs from 4% to 1% saves $1.5 million annually, material to income statement presentation.

FX Gain/Loss Volatility Reduction:

Instant settlement reduces the exposure window where currency fluctuations create unrealized gains or losses. Traditional 2-5 day settlement means holding foreign currency exposure during that period. Instant settlement eliminates that exposure window.

This reduces income statement volatility from FX movements, creating more predictable financial results valuable for both internal planning and external investor communication.

Implementation Decision Framework: When Balance Sheet Integration Makes Sense

Not every business needs stablecoin balance sheet integration immediately. Here’s the decision framework CFOs use to evaluate timing.

Business Model Alignment Assessment

International Customer Base Materiality:

If international customers represent less than 10% of revenue and cart abandonment isn’t a material issue, payment infrastructure modernization may not be top priority. But if international represents 25%+ of revenue with documented cart abandonment losses, customer conversion improvement justifies infrastructure investment.

Working Capital Sensitivity:

Capital-intensive businesses where working capital efficiency directly impacts profitability and growth capacity benefit more from instant settlement. Asset-light businesses with minimal working capital requirements see less balance sheet impact.

Growth Trajectory Considerations:

High-growth companies expanding internationally benefit from payment infrastructure that scales globally without geographic processor limitations. Mature companies with stable domestic operations see less strategic benefit.

Financial Statement Optimization Drivers

Liquidity Ratio Pressure:

If bank covenants require minimum current ratios or quick ratios, and the business operates near those thresholds, even modest ratio improvements from settlement optimization matter materially.

Working Capital Efficiency Mandates:

Board or investor pressure to improve working capital management creates internal stakeholders advocating for improvements. Stablecoin settlement optimization provides measurable working capital reduction.

Audit Complexity Reduction Goals:

If current international payment reconciliation creates significant manual accounting work and audit complexity, blockchain-based settlement with immutable audit trails reduces operational burden and potentially audit fees.

Risk-Adjusted Implementation Planning

Accounting Policy Development:

Work with external auditors before implementation to validate classification methodology. Document assessment of cash equivalent criteria. Establish disclosure framework for financial statement presentation.

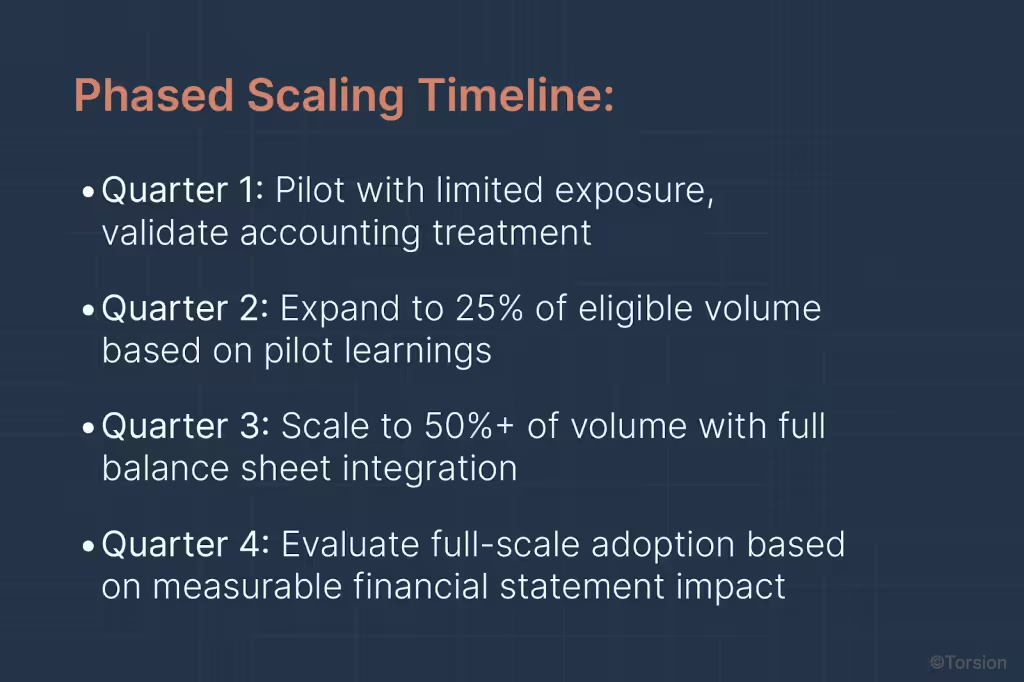

Pilot Program Approach:

Start with limited balance sheet exposure, perhaps 5-10% of payment volume, to validate accounting treatment, audit acceptance, and operational procedures before scaling to full international payment volume.

Stakeholder Communication Strategy:

Prepare investor relations materials explaining accounting treatment, business rationale, and balance sheet impact. Brief audit committee on risk management framework and internal controls.

The Strategic Balance Sheet Positioning

Stablecoin integration for enterprise balance sheets represents more than payment efficiency, it’s financial statement positioning for emerging infrastructure.

Competitive Financial Metrics

Peer Benchmarking Considerations:

As more enterprises adopt stablecoin treasury operations, balance sheet efficiency metrics begin showing peer comparison gaps. Companies optimizing working capital through instant settlement achieve better liquidity ratios than those maintaining traditional payment infrastructure.

Financial statement comparisons in investor presentations increasingly show these efficiency differences. The question evolves from “should we adopt new technology” to “can we afford the competitive financial disadvantage of not adopting?”

Investor Communication Opportunity:

For growth companies, the narrative of operational efficiency translating to balance sheet optimization resonates with investors focused on capital efficiency. Story transitions from “we’re growing internationally” to “we’re growing internationally while improving working capital efficiency through modern infrastructure.”

Future-Proofing Financial Operations

Regulatory Evolution Positioning:

SEC April 2025 guidance and GENIUS Act passage create regulatory clarity that didn’t exist previously. This clarity window enables enterprise adoption before potential future uncertainty. Early adopters establish accounting treatment and operational procedures while frameworks are evolving favorably.

Infrastructure Readiness Statistics:

With 86% of financial institutions reporting stablecoin infrastructure readiness and 23% of CFOs expecting adoption within 2 years (39% for $10B+ companies), mainstream integration is accelerating. First movers establish competitive advantages in balance sheet efficiency.

Accounting Standards Trajectory:

As FASB and IASB develop more specific guidance for digital assets meeting payment stablecoin criteria, accounting treatment will likely codify cash equivalent classification for qualifying stablecoins. Establishing procedures under current evolving guidance positions enterprises for smoother transition as standards formalize.

The Path Forward: From Revenue Optimization to Balance Sheet Integration

The journey from cart abandonment to cash equivalent classification demonstrates how operational improvements translate to financial statement optimization under the right regulatory framework.

The Transformation Components

Customer Conversion: 25% documented reduction in cart abandonment through expanded payment method availability captures revenue from international customers traditional processors couldn’t serve.

Working Capital: Instant settlement eliminates 2-5 day float, freeing capital and improving liquidity ratios without requiring additional cash investment.

Balance Sheet Classification: SEC guidance enabling potential cash equivalent treatment transforms payment infrastructure into financial statement optimization tool.

Audit Enhancement: Blockchain immutable records superior to traditional payment documentation reduce reconciliation complexity and potentially audit fees.

These components aren’t independent, they compound. Better customer conversion generates more revenue. Instant settlement of that revenue improves working capital. Cash equivalent classification optimizes balance sheet presentation. Superior audit trails reduce compliance burden.

The Strategic CFO Decision

For CFOs managing international operations with material cart abandonment losses, working capital efficiency opportunities, or balance sheet optimization mandates, stablecoin integration addresses multiple priorities simultaneously.

The question isn’t whether payment infrastructure will evolve toward instant settlement and regulatory-compliant stablecoin classification. The regulatory frameworks passed in 2025 and accounting standards evolution suggest that trajectory is established.

The strategic question for CFOs is whether your balance sheet will be positioned to capture the customer conversion, working capital, and financial statement optimization benefits as this infrastructure transformation accelerates, or whether you’ll implement reactively when peer financial metrics demonstrate the competitive gap.

Your customers are abandoning carts because payment infrastructure doesn’t match their needs. Your working capital is tied up in multi-day settlement processes. Your balance sheet could optimize through cash equivalent classification enabled by evolving regulatory guidance.

The components for transformation exist. The regulatory clarity enabling enterprise adoption is established. The accounting frameworks supporting balance sheet integration are evolving favorably.

Implementation timing determines whether you lead balance sheet optimization or follow as best practices become standard practices.