TL;DR

The Inflection Point

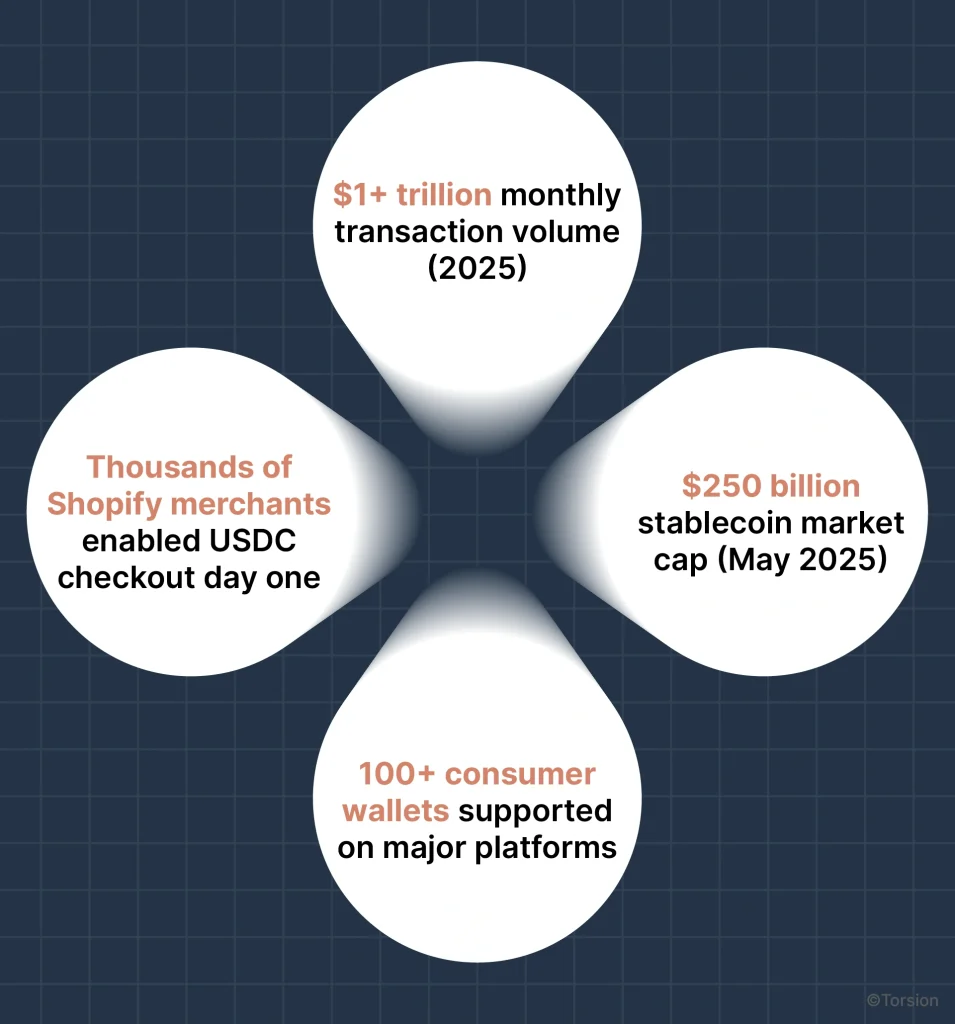

- Shopify launched native USDC checkout in June 2025. $1T+ monthly stablecoin volume now matches major card networks

The Business Impact

- 95% cost reduction: 0.1-0.3% fees vs. 2.9-4.5% traditional

- 25% cart abandonment drop: Proven across merchant networks

- Instant settlement: 40 seconds to 6 minutes vs. 2-3 days

The Implementation Reality

- 2-4 weeks for Stripe/payment processor integration

- Zero blockchain expertise required—APIs abstract complexity

- Shopify merchants: 0.50% rebate on USDC transactions

The Strategic Choice

- Stablecoins add payment option (don’t replace traditional methods)

- Early adopters gain 18-24 month operational learning advantage

- Pilot with 5-10% traffic to validate before scaling

E-commerce has its signature moments of infrastructure transformation.

2005: Amazon Prime redefined expectations and two-day shipping became the baseline.

2015: Mobile commerce went mainstream and one-click checkout became standard.

2025: Stablecoins emerged as production e-commerce infrastructure with major platform integration.

Most CTOs missed the significance of June 2025. While everyone debated AI strategy, Shopify quietly launched USDC checkout powered by Coinbase and Stripe. Not as an experiment. As production infrastructure serving thousands of merchants from day one.

The signal? Stablecoins processed over $1 trillion in monthly payment volume in 2025, matching major card networks but with 95% lower fees and sub-minute settlement. This isn’t blockchain’s theoretical future. It’s payment infrastructure quietly reshaping commerce while most technical leaders aren’t watching.

Here’s the architectural reality: 70% of online purchases end in cart abandonment. The final mile, payment processing, remains the weakest link in the entire commerce stack. Traditional payment rails introduce latency (2-3 day settlement), geographic restrictions (processor country blocks), and cost inefficiencies (2.9-4.5% all-in fees) that simply don’t exist in domestic card transactions.

Stablecoins solve this through fundamentally different infrastructure. Blockchain networks process payments peer-to-peer in 40 seconds to 6 minutes, operate 24/7/365 without banking hours, and charge 0.1-0.3% processing fees. Early adopters are capturing measurable advantages: 25% cart abandonment reduction, 95% payment cost savings, and access to previously blocked international markets.

The question isn’t whether stablecoins will transform e-commerce payments. They already are. The question is whether your platform captures the first-mover advantage or waits until competitors force your hand.

The Silent Revolution Already Reshaping Commerce

Stablecoin payments crossed the chasm from experimental to production infrastructure in 2025. The evidence isn’t in whitepapers, it’s in platform integrations.

Shopify’s USDC integration (June 2025) partnered Coinbase and Stripe to offer native stablecoin checkout on the Base network. Merchants receive a 0.50% rebate on USDC transactions, not just avoiding the 2.9% credit card fee, but earning back half a percent. For a merchant processing $500K monthly, that’s a $17,500 swing from traditional payments (costing $14,500) to stablecoin payments (earning $2,500 rebate).

PayPal launched PYUSD in 2023, initially dismissed as defensive positioning. By 2025, it’s processing meaningful volume across merchant networks as consumers realize digital dollars spend like regular dollars but settle faster.

Visa reported $710 billion in stablecoin transaction volume in March 2025. The world’s largest card network now processes more stablecoin transactions than many regional card schemes, showing the infrastructure evolution.

TransFi documented 25% cart abandonment reduction across their merchant network after adding crypto/stablecoin checkout options. This isn’t theoretical benefit. It’s measured conversion improvement from production systems.

The pattern: “Silent revolution”. Most consumers don’t realize they’re using blockchain infrastructure. They experience faster checkout, lower fees, and eliminated payment failures. The technology disappears into user experience—the hallmark of mature infrastructure adoption.

“Stablecoins have grown to over a trillion dollars in monthly payment volume, trusted by users around the globe.” — Shopify, June 2025 announcement

Volume Reality: Already Larger Than Regional Card Networks

Stablecoins aren’t preparing to compete with traditional payments. They’re already processing comparable volume:

For context: Discover Card processes approximately $400 billion annually. American Express processes approximately $1.4 trillion annually. Stablecoins are processing $12+ trillion annualized between Discover and Amex in total volume, achieved in under seven years since USDC’s 2018 launch.

The infrastructure matured while technical leaders were distracted by other priorities. Now it’s production-ready, platform-integrated, and capturing market share through superior economics.

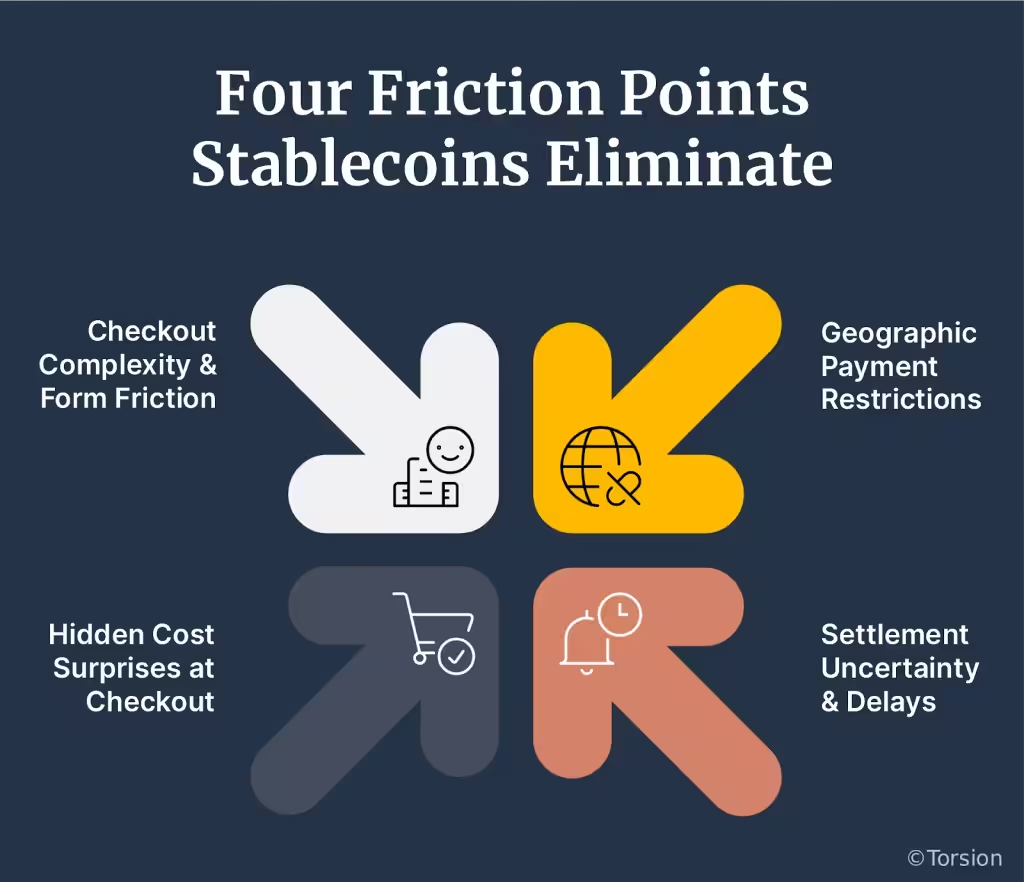

Four Friction Points Stablecoins Eliminate

E-commerce checkout represents four sequential failure points. Each reduces conversion. Each costs revenue. Stablecoins address all four through architectural differences, not incremental improvements.

Friction Point #1: Geographic Payment Restrictions

Traditional Architecture

International card transactions route through correspondent banking networks built for wire transfers, not real-time commerce. Payment processors maintain geographic exclusion lists based on banking relationships and regulatory complexity. A customer in Nigeria trying to buy from a US merchant faces arbitrary payment blocks—not because of fraud risk, but because the payment infrastructure doesn’t exist.

The Cost

Merchants lose access to markets representing $1.2 trillion in annual cross-border payment volume. Not because demand doesn’t exist. Because payment rails can’t reach those customers.

Stablecoin Architecture

Blockchain networks operate peer-to-peer without correspondent banking intermediaries. Payments route directly from customer wallet to merchant address, processed by decentralized validator networks. No geographic restrictions. No processor approval required. No arbitrary exclusions.

The Experience Transformation

- Customer in Sri Lanka buying from US merchant: Payment succeeds instead of failing

- Merchant serving Latin America: 22% payment failure rate drops to < 3%

- Platform expansion: Access previously blocked markets without new banking relationships

Benefits

- Feature: Peer-to-peer blockchain payment routing

- Functional Benefit: Eliminate geographic processor restrictions

- Higher-Order Benefit: Access $1.2T cross-border payment market

- Emotional Benefit: Competitive advantage through expanded market access

Friction Point #2: Settlement Uncertainty & Delays

Traditional Architecture

Credit card payments require 2-3 business days for settlement. The authorization happens instantly (customer sees “payment successful”), but the merchant doesn’t receive funds for 48-72 hours. Weekend transactions? Add 2-3 additional days. International transactions? Sometimes 5-7 days.

This creates multiple problems

- Fulfillment delays: Merchants wait for settlement before shipping high-value items

- Chargeback risk: 120-day dispute window means uncertainty never fully resolves

- Working capital constraints: Cash tied up in payment float instead of operations

Stablecoin Architecture

Settlement occurs in 40 seconds to 6 minutes on major blockchains. When the transaction confirms, the merchant controls the funds. No intermediary holding period. No settlement batch processing. No banking hours limiting when payments clear.

The settlement is also irreversible. No chargeback risk. No 120-day dispute window. The transaction finality provides certainty traditional payments never achieve.

The Experience Transformation

- Friday evening order: Ships Saturday morning because payment settled overnight

- High-value purchase: No “pending verification” delays, instant fulfillment confidence

- International order: No time zone coordination or multi-day settlement waits

Operational Impact

Businesses report significant working capital efficiency improvements because instant settlement eliminates payment timing uncertainty. Cash previously held in reserves for payment float can be redeployed to inventory, marketing, or product development.

Benefits

- Feature: Blockchain settlement in 40 seconds to 6 minutes

- Functional Benefit: Instant payment certainty, no chargeback risk

- Higher-Order Benefit: Working capital efficiency, faster fulfillment

- Emotional Benefit: Operational control and competitive fulfillment speed

Friction Point #3: Hidden Cost Surprises at Checkout

Traditional Architecture

Payment processors advertise “2.9% + $0.30” but the actual cost structure includes:

- Base processing fee: 2.9% (advertised rate)

- International card markup: Additional 1-1.5%

- Currency conversion spread: 2-3% hidden in exchange rate

- Cross-border transaction fee: $0.50-2.00 per transaction

Actual all-in cost: 4.5-7.5% for international transactions.

Customers experience this as surprise fees at final checkout step. A $100 product becomes $103-107 after currency conversion. The psychological impact: 17% of customers abandon carts after seeing unexpected fees.

Stablecoin Architecture

Payments occur in dollar-denominated stablecoins. No currency conversion because both parties transact in digital dollars. Processing fees are transparent network costs ($0.50-3.00 regardless of transaction amount).

Merchants save 95% on processing costs (from 2.9-4.5% to 0.1-0.3%). Some pass savings to customers (competitive pricing). Others capture margin improvement. Both options unavailable with traditional payment economics.

The Experience Transformation

- Price displayed = price paid: No checkout surprises, no hidden conversion spreads

- Transparent fees: Customer sees “$1.20 network fee” not “3.2% processing + FX markup”

- Merchant economics: $100 sale nets $99.70 (stablecoin) vs. $95.50 (credit card international)

Competitive Positioning

Early stablecoin adopters can afford 2-3% lower pricing than competitors while maintaining equivalent margins. In commoditized markets, that pricing advantage drives substantial market share gain.

Benefits

- Feature: Dollar-denominated transactions with transparent network fees

- Functional Benefit: 95% cost reduction (from 2.9-4.5% to 0.1-0.3%)

- Higher-Order Benefit: Competitive pricing or margin expansion

- Emotional Benefit: Strategic flexibility through superior economics

Friction Point #4: Checkout Complexity & Form Friction

Traditional Architecture

Credit card checkout requires

- 16-digit card number (prone to typos)

- Expiration date

- CVV security code

- Billing address (full street address, city, state, zip)

- Email confirmation

- Multi-step authentication (3D Secure for international cards)

Average completion time: 3-5 minutes. Each additional form field reduces conversion by 2-4%.

Stablecoin Architecture

- Customer clicks “Pay with USDC”

- Wallet authorization prompt (FaceID, TouchID, PIN)

- Transaction confirms (40 seconds average)

No form fields. No address entry. No card number typos. Biometric approval or PIN provides security without friction.

The Experience Transformation

- One-click authorization: Similar to Apple Pay UX but with stablecoin economics

- Guest checkout supported: Pay with credit card → auto-converts to USDC → merchant receives stablecoin

- Returning customer flow: Saved wallet = instant re-purchase without re-entering details

Shopify Implementation

The USDC checkout integrates with Shop Pay (Shopify’s accelerated checkout). Customers see familiar Shop Pay button. Backend settles in stablecoins. User experience identical to traditional payments but with superior economics and settlement.

Benefits

- Feature: Wallet-based one-click authorization

- Functional Benefit: Faster checkout, fewer form fields, biometric security

- Higher-Order Benefit: Reduced cart abandonment, improved conversion rates

- Emotional Benefit: Customer experience leadership and competitive differentiation

Shopify’s USDC Integration: Infrastructure Goes Mainstream

June 2025 marked stablecoins crossing from experimental to standard e-commerce infrastructure.

The Partnership Architecture

- Shopify: Platform and merchant relationship

- Coinbase: Custody and blockchain infrastructure

- Stripe: Payment processing and settlement

- Base Network: Layer-2 Ethereum blockchain (low fees, fast settlement)

Merchant Economics

- 0.50% rebate on USDC transactions (vs. paying 2.9% credit card fees)

- No foreign exchange fees on international transactions

- Automatic currency conversion: Merchant chooses to receive USDC directly or auto-convert to local fiat

Customer Experience

- 100+ wallet options supported: Metamask, Rainbow, Coinbase Wallet, Trust Wallet, etc.

- Shop Pay integration: Familiar one-click checkout powered by stablecoins

- Guest checkout: Pay with credit card, backend converts to USDC automatically

Why This Matters

Shopify’s merchant base represents significant e-commerce market share globally. Early adoption among even a fraction of merchants signals substantial infrastructure shift. The infrastructure shift from experimental to mainstream happens through platform-level adoption, not merchant-by-merchant evangelism.

First 90 Days Results

- Thousands of merchants activated USDC checkout day one

- Enhanced international conversion rates reported across merchant base

- Platform roadmap: Shopify has indicated plans to explore customer incentives for USDC payments as adoption grows

TransFi: 25% Cart Abandonment Reduction

TransFi provides payment infrastructure for cross-border e-commerce, processing transactions for online retailers in emerging markets.

The Problem

Merchants serving international customers faced 70% cart abandonment rates. Primary causes:

- Payment method restrictions (customer’s card not accepted)

- Cross-border transaction failures (processor declined)

- Currency conversion uncertainty (customers unsure of final cost)

The Implementation

Integrated crypto/stablecoin checkout option alongside traditional payment methods. Customers see:

- Credit/debit card

- PayPal/digital wallets

- Pay with stablecoins (USDC, USDT)

The Results

- 25% cart abandonment reduction across merchant network

- Higher average order value from international customers (confidence in payment success)

- Expanded market reach to regions with limited credit card penetration

Why It Worked

Stablecoins didn’t replace traditional payments, they complemented them. Customers who previously failed at checkout had new option that succeeded. The incremental conversion improvement from previously lost customers drove ROI without cannibalizing existing payment methods.

D2C Platform Economics: 95% Cost Reduction

Direct-to-consumer brands face margin pressure from customer acquisition costs, fulfillment expenses, and payment processing fees. Every basis point of cost reduction flows directly to profitability or competitive pricing.

Traditional Payment Economics (International Transaction)

- Product price: $100

- Credit card processing: 2.9% ($2.90)

- International card markup: 1.5% ($1.50)

- Currency conversion spread: 2% ($2.00)

- Merchant nets: $93.60

Stablecoin Payment Economics

- Product price: $100

- Transaction fee: 0.2% ($0.20)

- Network fee: $1.50 (flat regardless of amount)

- Merchant nets: $98.30

The Margin Impact

$98.30 (stablecoin) vs. $93.60 (credit card) = $4.70 additional margin per $100 transaction

For a business processing $1M monthly in international transactions, that’s $47,000 monthly or $564,000 annually in recovered margin. That capital enables:

- Competitive pricing: Lower prices by 2-3% while maintaining margins

- Marketing investment: Redeploy savings to customer acquisition

- Product development: Fund R&D from operational efficiency

Market Access Benefit

D2C brands using stablecoins can serve unbanked and underbanked populations globally. Credit card penetration in emerging markets: 20-30%. Smartphone + internet penetration: 60-80%. Stablecoins reach the gap, customers who can’t access traditional payments but can download a wallet app.

Benefits

- Feature: 95% payment cost reduction

- Functional Benefit: Improved unit economics on every transaction

- Higher-Order Benefit: Competitive pricing flexibility or margin expansion

- Emotional Benefit: Strategic control and financial sustainability

Behind the Magic: How It Actually Works

CTOs evaluating stablecoins need architectural understanding, not marketing fluff. Here’s the technical reality.

Layer 1: Blockchain Infrastructure

Base Network (Shopify’s Choice)

- Type: Ethereum Layer-2 (inherits Ethereum security, improves speed/cost)

- Transaction speed: 2-5 seconds average confirmation

- Cost: $0.50-1.50 per transaction (regardless of amount)

- Why Shopify chose it: Coinbase-backed, optimized for commerce, EVM-compatible

Ethereum Mainnet

- Type: Layer-1 blockchain (highest security, most liquidity)

- Transaction speed: 12 seconds per block, 1-2 minutes for finality

- Cost: $3-15 per transaction (variable based on network congestion)

- Use case: High-value transactions, maximum security requirements

Solana

- Type: High-performance Layer-1

- Transaction speed: 400ms average confirmation

- Cost: $0.00025 per transaction (fractions of a penny)

- Trade-off: Different security model, occasional network instability

Platform Selection Criteria

- Transaction volume: High volume favors low-cost chains (Solana, Base)

- Transaction value: High value favors high-security chains (Ethereum)

- Integration ecosystem: Shopify/Stripe support favors Base, Ethereum

Layer 2: Stablecoin Selection

USDC (Circle)

- Market cap: Significant market leader (2025)

- Backing: 1:1 cash and short-term US Treasury bills

- Audits: Monthly attestations by major accounting firms

- Regulation: Licensed money transmitter, GENIUS Act compliant

- Platform support: Shopify, Stripe, Coinbase, PayPal, Visa

USDT (Tether)

- Market cap: Largest stablecoin by market cap

- Backing: Mixed reserves (cash, Treasury bills, commercial paper)

- Audits: Quarterly attestations

- Use case: Highest liquidity, international markets, crypto-native customers

PYUSD (PayPal)

- Launch: 2023

- Backing: 1:1 dollar reserves

- Integration: Native PayPal ecosystem integration

- Use case: PayPal merchants, mainstream consumer adoption

Selection Criteria for Merchants

- USDC: Regulatory compliance priority, US-focused customers, Shopify integration

- USDT: International focus, crypto-native customers, maximum liquidity

- PYUSD: PayPal ecosystem, mainstream consumers, brand recognition

Layer 3: Application Integration

Payment Processor APIs

- Stripe: Enable stablecoin support via dashboard toggle, webhook integration for settlement notifications

- Coinbase Commerce: REST API, similar integration pattern to traditional payment gateways

- PayPal: PYUSD native in PayPal checkout flow, minimal merchant integration

Platform Plugins

- Shopify: Native USDC support via Shopify Payments (no plugin required)

- WooCommerce: Crypto payment plugins available (Coinbase Commerce, custom)

- Magento/Adobe Commerce: Custom integration or third-party extensions

Custom Implementation

For custom platforms, integration requires –

- Wallet connection library (WalletConnect, RainbowKit)

- Blockchain RPC provider (Alchemy, Infura, QuickNode)

- Transaction monitoring (webhook listeners for payment confirmation)

- Settlement logic (auto-convert to fiat or hold stablecoins)

Timeline Comparison

- Platform-native (Shopify): 1-2 weeks (configuration + testing)

- Payment processor API: 2-4 weeks (integration + testing)

- Custom implementation: 6-12 weeks (development + security audit + testing)

Customer Journey: The Technical Flow You Must Know

Step 1: Payment Method Selection

Customer lands on checkout, sees payment options:

- Credit/Debit Card

- PayPal

- Shop Pay

- Pay with USDC ← New option

Step 2: Wallet Connection

Customer clicks “Pay with USDC”:

- If wallet installed: Browser prompts wallet authorization (Metamask popup)

- If no wallet: Guest checkout option (pay with credit card, backend converts to USDC)

- If returning customer: Shop Pay remembers wallet, one-click authorization

Step 3: Transaction Authorization

Customer authorizes payment via:

- Biometric: FaceID, TouchID (mobile wallets)

- PIN: Wallet password/PIN (desktop)

- Hardware wallet: Ledger/Trezor confirmation (security-conscious users)

Step 4: Blockchain Processing

- Transaction broadcasts to blockchain network

- Validators process transaction (40 seconds to 6 minutes depending on network)

- Merchant receives payment confirmation webhook

Step 5: Order Fulfillment

- Merchant system receives webhook: “Payment confirmed”

- Order status updates to “Processing”

- Fulfillment triggers (same as credit card authorization)

Customer sees: “Payment successful” → “Order confirmed” → “Preparing shipment”

Backend reality: Stablecoin settled instantly, merchant controls funds immediately

Merchant Backend Options

Option A: Receive Stablecoins Directly

- Merchant maintains USDC balance in treasury wallet

- Use cases: Pay suppliers in USDC, hold as cash equivalent

- Complexity: Requires internal treasury procedures for crypto holdings

- Benefit: Maximum cost savings (no conversion fees)

Option B: Auto-Convert to Fiat

- Payment processor converts USDC to local currency instantly upon receipt

- Merchant receives: Traditional bank deposit (USD, EUR, etc.)

- Complexity: Zero—merchant never touches crypto

- Benefit: Zero operational change, automatic stablecoin economics

Option C: Hybrid Approach

- Hold portion in USDC for specific use cases

- Auto-convert remainder to fiat for operational expenses

- Optimization: Balance cost savings with operational simplicity

Shopify Default: Option B (auto-convert to merchant’s local currency). Merchants can opt into Option A or C through settings.

Compliance & Security Handled

KYC/AML Requirements

- Customer verification: Payment processor handles (same as credit card)

- Merchant verification: Platform onboarding process (Shopify, Stripe KYC)

- Transaction monitoring: Blockchain analytics detect suspicious activity

Regulatory Compliance

- GENIUS Act: Federal framework (July 2025) requires stablecoin reserve backing and audits

- State licensing: Payment processors hold money transmission licenses (merchants don’t need separate licenses)

- Tax reporting: 1099 forms generated by payment processors (same as PayPal)

Security Architecture

- Private key custody: Payment processors use institutional custody solutions

- Multi-signature wallets: Require multiple authorizations for large transfers

- Hot/cold wallet split: Daily operating funds in hot wallets, bulk reserves in cold storage

Merchant Risk Profile

Zero additional security burden compared to traditional payments. Payment processor abstracts blockchain complexity and manages all custody/security requirements.

Overcoming Adoption Barriers

CTOs face legitimate concerns beyond technical architecture. Here’s the reality check on common objections.

Barrier #1: My Customers Don’t Have Crypto Wallets

The Perception

Stablecoin payments require crypto-native customers who already own wallets and understand blockchain. Mainstream consumers won’t adopt.

The Reality

Multiple friction-reduction strategies exist including –

Guest Checkout with Auto-Conversion

Customer pays with credit card → Payment processor converts to USDC → Merchant receives stablecoin → Customer never knows blockchain was involved. Shopify enables this by default.

Embedded Wallets

Platform creates wallet automatically during first purchase. Customer only interacts with familiar email/password login. Wallet exists but user never sees private keys or blockchain complexity.

Familiar UX Design

Shopify’s USDC checkout looks identical to credit card checkout. Customer sees “Pay with USDC” button similar to “Pay with Apple Pay.” The blockchain disappears into user experience.

Adoption Strategy

- Phase 1: Enable stablecoin checkout, rely on crypto-native early adopters

- Phase 2: Add guest checkout auto-conversion as infrastructure matures

- Phase 3: Market stablecoin benefits (lower fees, faster settlement) as differentiation

Current Adoption Data

Early data suggests single-digit to mid-teens customer adoption rates when stablecoin options are offered alongside traditional payments. Rate climbs significantly after first successful transaction (trust + familiarity). Not mainstream yet, but growing steadily as infrastructure matures.

Barrier #2: Integration Sounds Complicated

The Perception

Blockchain integration requires specialized developers, months of development, and significant technical risk. Too much complexity for incremental payment method.

The Reality

Payment processor APIs abstract blockchain complexity to familiar REST API patterns.

Stripe Integration Example

1. Enable stablecoin support in Stripe dashboard (toggle setting)

2. Add webhook listener for “payment.succeeded” event

3. Test with $1 transaction on testnet

4. Deploy to production

Implementation timeline: 2-4 weeks including testing and team training.

Technical lift comparison

- Adding Apple Pay: 1-2 weeks (similar API integration)

- Adding PayPal: 1-2 weeks (similar API integration)

- Adding stablecoin payments: 2-4 weeks (same pattern, slightly newer)

No Blockchain Expertise Required

Payment processor handles

- Wallet connection UI

- Transaction broadcasting

- Confirmation monitoring

- Settlement to merchant account

- Currency conversion (if selected)

Developer Experience

If your team can integrate Stripe or PayPal, they can integrate stablecoin payments. The API patterns are intentionally familiar.

Risk Mitigation

Run pilot with 5-10% of traffic to validate before full rollout. Traditional payment methods remain enabled, stablecoins add options and don’t replace existing infrastructure.

Barrier #3: Regulatory Uncertainty

The Perception

Stablecoins operate in legal gray area. Future regulations could force shutdowns or create compliance nightmares. Too risky for production commerce systems.

The Reality (October 2025)

Federal Framework Established

GENIUS Act (passed July 2025) provides federal stablecoin regulations:

- Reserve backing requirements (1:1 dollar reserves)

- Monthly audit mandates

- Federal licensing for stablecoin issuers

- Consumer protection standards

Institutional Validation

- Circle announced IPO plans signaling institutional maturity

- Visa processing $710B stablecoin volume (March 2025)

- Major banks offering services: Societe Generale, Santander, BNY Mellon

Payment Processor Compliance

Stripe, PayPal, and Coinbase hold money transmission licenses in all 50 states. They handle regulatory compliance and merchants don’t need separate licenses or compliance programs.

Regulatory Risk Today

Lower than 2023-2024. Clear federal framework, institutional adoption, payment processor compliance infrastructure all reduce merchant risk to near-parity with traditional payment methods.

Fail-Safe Strategy

If regulatory environment changes unfavorably, disable stablecoin checkout option (configuration change, not architecture overhaul). Traditional payment methods remain unaffected.

Barrier #4: What If Stablecoins Fail?

The Perception

TerraUSD collapsed in 2022, losing dollar peg and wiping out billions. Enterprise stablecoins could suffer similar fate, leaving merchants holding worthless tokens.

The Reality

Enterprise stablecoins (USDC, USDT) use fundamentally different architecture than algorithmic stablecoins (UST/Terra).

Reserve-Backed vs. Algorithmic

- USDC/USDT: 1:1 backing by cash and Treasury bills in bank accounts

- UST (failed): Algorithmic model with no reserve backing (mathematical peg maintenance)

Verification Mechanisms

- Monthly audits by major accounting firms verify reserves

- Public attestations published monthly

- Regulatory oversight under GENIUS Act requires ongoing reserve verification

Diversification Strategy

Accept multiple stablecoins (USDC + USDT + PYUSD) to reduce single-issuer risk. If one experiences temporary issues, others remain functional.

Instant Conversion Option

Configure auto-conversion to fiat currency immediately upon receipt. Merchant exposure window: 2-5 minutes (transaction confirmation time). Risk negligible compared to holding overnight.

Historical Performance

USDC has maintained dollar parity within 0.03% for the vast majority of its existence (launched 2018). Temporary deviations (such as the Silicon Valley Bank situation in March 2023) corrected within 72 hours. No merchant holding USDC lost funds.

Fail-Safe

Traditional payment methods remain enabled. Stablecoins represent 5-15% of payment volume initially, not core dependency. If confidence erodes, disable features and revert to traditional payments exclusively.

The Future: Where E-commerce Payments Go Next [Analysis & Projections]

The following projections represent analysis based on historical platform adoption patterns and competitive dynamics, not confirmed product roadmaps.

Platform-level stablecoin adoption follows predictable innovation curves. Shopify moved first (June 2025). Competitors will likely follow. The question is timeline and implementation quality.

2025-2026: Platform Proliferation

Analysis: Major e-commerce platforms will likely offer stablecoin checkout options by late 2026 based on competitive dynamics.

Market Forces Driving Adoption

- Competitive pressure: Shopify’s 0.50% rebate creates merchant incentive to evaluate platforms

- Merchant demand: Cost savings (95%) and international reach represent significant benefits

- Infrastructure maturity: Payment processor solutions (Stripe, PayPal) reduce technical barriers

Projected Timeline (based on typical platform adoption patterns)

- Late 2025: WooCommerce plugins mature with improved integrations

- Early 2026: Additional commerce platforms likely announce explorations

- Late 2026: Broader platform ecosystem support becomes available

Why Major Platforms Will Evaluate

Payment processing represents significant cost center. A 95% reduction in processing costs creates strong financial incentive to explore alternatives that benefit both platforms and merchants.

Strategic Implication

Early movers (2025-2026) potentially gain 18-24 month competitive learning advantage before stablecoin checkout becomes widely available infrastructure. First-mover potential benefits: customer acquisition in underserved markets, superior unit economics enabling competitive pricing, brand positioning as innovation leader.

2026-2027: Consumer Incentive Programs

Current State: Merchant rebates (Shopify’s 0.50%)

Potential Evolution: Consumer-facing incentives

Possible Incentive Models

- Discounts: Merchants passing savings to customers choosing stablecoin payment

- Loyalty programs: Enhanced rewards for stablecoin transactions

- Fee coverage: Merchants absorbing network fees for stablecoin payments

Psychology of Adoption

Consumer incentives historically accelerate payment method adoption. Credit cards achieved ubiquity partially through rewards programs (cashback, points, miles). Stablecoins may follow similar adoption patterns.

Cross-Platform Potential

Stablecoins enable loyalty programs that could work across multiple merchants through blockchain interoperability: a structural advantage over closed-loop traditional programs.

2027-2028: Smart Contract Commerce Evolution

Automated Escrow

Payments could release automatically when shipment tracking confirms delivery. Smart contracts hold funds until both parties satisfied, reducing disputes.

Subscription Billing

Traditional challenge: Card expires, customer churns. Potential solution: Wallet authorization valid indefinitely (unless customer revokes), enabling seamless renewals.

Dynamic Pricing

Smart contracts could adjust pricing based on payment method, settlement speed, and transaction costs in real-time.

B2B Potential

- Conditional payments: Funds release when quality checks pass

- Supply chain automation: IoT sensors triggering payments when goods confirm in transit

- Embedded commerce: Automated purchasing based on predefined conditions

Timeline: Smart contract commerce evolution from experimental to production implementations likely spans 2027-2028 as platforms add programmability layers.

The Long-Term Trajectory

Strategic Analysis

Stablecoins represent structural cost and speed advantages (95% reduction, instant settlement) that compound over time. As infrastructure matures, user experience improves, and adoption grows, the economic advantages become increasingly difficult for traditional payment rails to match.

Platform Integration Momentum

When major platforms support stablecoins natively, merchant adoption accelerates exponentially. The shift from “specialty option” to “standard infrastructure” follows typical technology adoption curves.

Competitive Implications

Organizations implementing stablecoin payments in 2025-2027 gain:

- Market learning advantage: 18-24 months operational experience

- Cost structure benefit: Immediate margin or pricing flexibility

- Customer experience differentiation: Early adoption signals innovation

- Technical capability: Team develops blockchain integration expertise

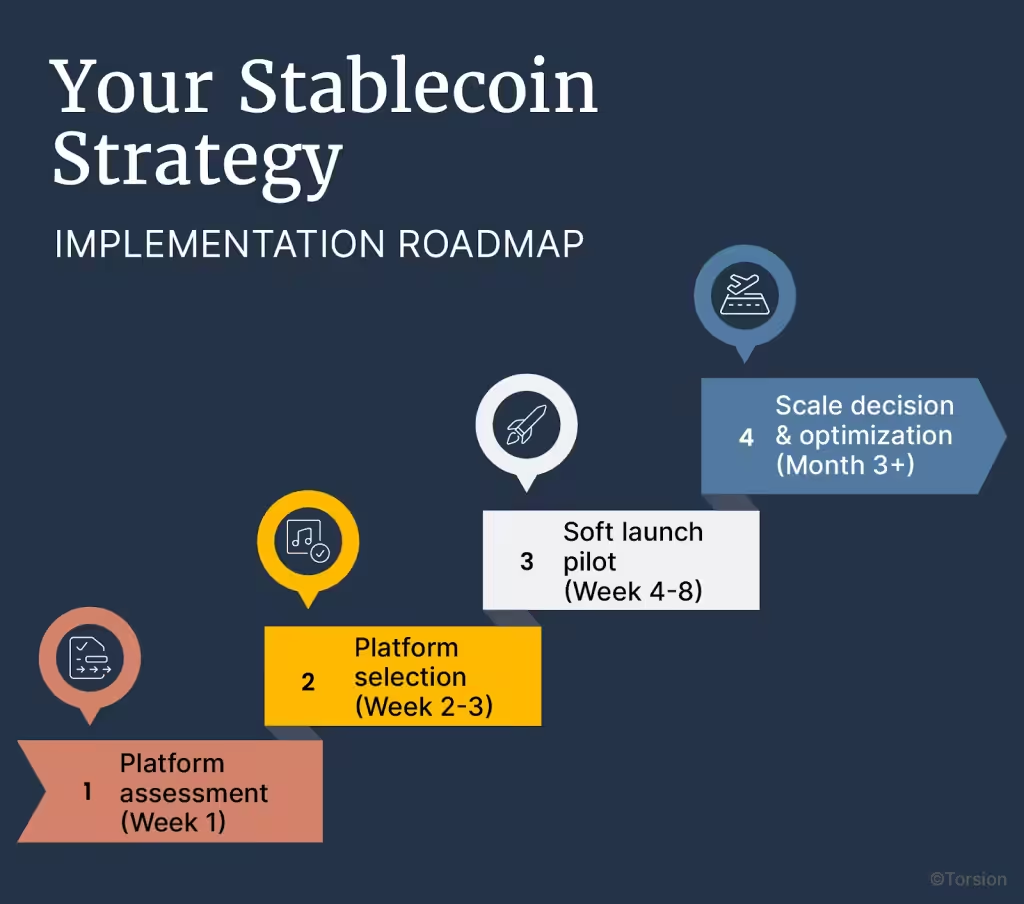

Your Stablecoin Strategy: Implementation Roadmap

CTOs evaluating stablecoins need concrete next steps, not just vision statements. Here’s the pragmatic adoption framework.

Step 1: Platform Assessment (Week 1)

Pull 90 days of payment data and analyze

- Cart abandonment rate overall and by geography

- International payment failure rate (what percentage of international transactions fail)

- All-in processing costs including hidden fees (FX spreads, international markups)

- Customer requests for alternative payment methods (support tickets, feedback)

Competitive Analysis

- Which competitors offer crypto/stablecoin checkout

- What market positioning opportunities exist

- Potential advantages available in your vertical

Platform Capabilities

- If Shopify Plus: Native USDC support available now

- If WooCommerce: Evaluate available plugins or Stripe integration

- If custom platform: Assess Stripe API integration timeline vs. Coinbase Commerce

Establish baseline metrics for

- Cart abandonment rate (reference: 25% reduction achieved by TransFi)

- International conversion rate

- Payment processing costs

- Customer satisfaction (CSAT/NPS impact)

Step 2: Platform Selection (Week 2-3)

If Using Shopify Plus:

- Enable USDC checkout via Shopify Payments dashboard

- Configure auto-conversion vs. direct USDC receipt (recommend auto-conversion for simplicity)

- Test checkout flow with internal team (5-10 test transactions)

- Timeline: 1-2 weeks to production-ready

If Using Other Platforms:

- Stripe integration: Best for platforms already using Stripe (familiar API, proven infrastructure)

- Coinbase Commerce: Alternative for custom platforms

- PayPal PYUSD: Option for PayPal-heavy merchant base

If Custom Platform:

- Evaluate build vs. integrate: Custom implementation provides maximum control but requires 6-12 weeks development

- Security audit requirement: Smart contract interactions require security review (add 2-4 weeks)

- Maintenance burden: Ongoing monitoring, updates, security patches

Recommendation for Most CTOs

Use payment processor APIs (Stripe, Coinbase Commerce) rather than custom implementation. Focus engineering resources on core product differentiation, not payment infrastructure.

Step 3: Soft Launch Pilot (Week 4-8)

Enable stablecoin checkout for

- 5% of traffic initially (A/B test vs. traditional-only checkout)

- Specific product categories (higher-margin items or international best-sellers)

- Select customer segments (based on browsing behavior or demographics)

Track KPIs daily

- Stablecoin adoption rate: What percentage of eligible customers choose USDC payment

- Conversion rate impact: Do customers who see stablecoin option convert differently than control

- Payment success rate: Do stablecoin transactions succeed more reliably than cards

- Customer feedback: Support tickets, reviews, direct feedback about experience

Monitor for

- Transaction confirmation times: Are settlements happening within expected 2-6 minute window

- Failed transactions: Root cause analysis (wallet connection issues, insufficient balance, network congestion)

- Integration errors: API timeouts, webhook delivery failures, settlement discrepancies

Prepare support team with

- Stablecoin basics: What they are, how they work (simple explanation)

- Troubleshooting guide: Wallet connection issues, transaction stuck, refund process

- Escalation path: When to involve engineering team vs. payment processor support

Timeline: Run pilot for 30-60 days to gather statistically significant data before scale decision.

Step 4: Scale Decision & Optimization (Month 3+)

Quantitative Metrics

- Did cart abandonment decrease? Target: 10-25% reduction

- Did international conversion improve? Target: 5-15% improvement

- Did processing costs drop? Target: 50-70% on stablecoin transactions

- What adoption rate achieved? Benchmark: Single-digit to mid-teens is strong first 90 days

Qualitative Assessment

- Customer feedback: Positive, neutral, or negative sentiment

- Support burden: Did stablecoin payments create disproportionate support load

- Team confidence: Does engineering team feel comfortable maintaining infrastructure

- Strategic value: Does this support international expansion or competitive positioning goals

If pilot succeeds

- Expand to 50% of traffic (month 4)

- Enable for all products (month 5)

- Consider promoting stablecoin option in marketing (month 6)

- Evaluate customer incentives if economics support (month 6-9)

Advanced Optimization

- Multi-stablecoin support: Add USDT for international customers, PYUSD for PayPal ecosystem

- Smart routing: Suggest optimal payment method based on customer location and transaction size

- Loyalty integration: Reward stablecoin usage with bonus points or exclusive perks

The Choice: Lead or Follow

E-commerce stands at a payment infrastructure inflection point. The evidence isn’t in whitepapers or conference presentations. It’s in production systems processing real transactions.

$1 trillion in monthly stablecoin transaction volume, more than many regional card networks. Shopify, Stripe, Coinbase built the integration infrastructure. Early merchants capturing measurable benefits: 25% cart abandonment reduction, 95% payment cost savings, expanded international market access.

Shopify’s June 2025 launch moved stablecoins from experimental to mainstream e-commerce infrastructure. Other platforms will likely follow within 18-24 months based on competitive dynamics and merchant demand.

The strategic choice: Explore early adoption (2025-2026) or wait until competitive pressure requires implementation at later stage.

Potential early-mover advantages

- Market learning: 18-24 month operational experience head start

- Cost structure: Infrastructure enabling pricing flexibility

- Customer experience: Innovation positioning and brand differentiation

- Technical capability: Team develops blockchain integration expertise

Considerations for waiting

- Infrastructure continues maturing

- More reference implementations become available

- Broader ecosystem support develops

- Risk of competitors capturing market advantages during waiting period

Cart abandonment decreases 25%. Processing costs drop 95%. International markets become accessible. These represent present realities for merchants who’ve implemented stablecoin payments, not future possibilities.

The infrastructure exists. Regulations provide clarity (GENIUS Act, July 2025). Platforms offer integration (Shopify, Stripe, Coinbase). Global wallet users continue growing.

What’s your stablecoin strategy?

Partner with Torsion for Expert Implementation

Torsion helps e-commerce platforms adopt stablecoin payments through technical integration, compliance guidance, and customer experience optimization.

What You Get

- ✓ Platform-specific integration roadmaps (Shopify, WooCommerce, Magento, custom platforms)

- ✓ Technical implementation support (API integration, testing, deployment)

- ✓ Compliance framework guidance (GENIUS Act, state regulations, documentation)

- ✓ Customer experience optimization (checkout flow design, friction reduction strategies)

- ✓ Performance monitoring (KPI tracking, ongoing improvement recommendations)

Why Partner vs. DIY

- Faster time-to-market: 4-8 weeks vs. 6-12 months internal development

- Expert compliance: Navigate regulations without dedicated legal team

- Maintained focus: Engineering team stays on core product, not payment infrastructure

- Proven approaches: Implementation strategies validated across merchant segments

Ready to explore stablecoin checkout for your platform? Schedule a strategy session to assess integration options and potential conversion improvements.

FAQs

How does Shopify’s USDC integration actually work?

Shopify partnered with Coinbase and Stripe to offer native USDC checkout on the Base blockchain network. Merchants enable the feature through Shopify Payments dashboard. Customers can pay from 100+ supported wallets (Metamask, Rainbow, Coinbase Wallet) or use guest checkout where they pay with credit card and the backend automatically converts to USDC.

Merchants receive a 0.50% rebate on USDC transactions (compared to paying 2.9% for credit card processing). They choose whether to receive USDC directly or have it automatically converted to their local currency. The checkout experience integrates with Shop Pay, so customers see familiar interface powered by stablecoin infrastructure.

Do we need blockchain developers on our team?

No. Payment processors (Stripe, Coinbase, PayPal) abstract blockchain complexity behind familiar REST APIs. The integration resembles adding Apple Pay or PayPal enable the feature via API, add webhook listeners for payment confirmations, test, and deploy.

Your existing engineering team can handle implementation if they have experience with payment gateway integrations. Blockchain expertise becomes relevant only if building custom smart contract functionality or direct blockchain integration (which most merchants don’t need).

How does this integrate with our existing payment stack?

Stablecoins add payment option alongside existing methods and don’t replace credit cards, PayPal, or other processors. Customers see “Pay with USDC” as one choice among several at checkout.

Backend integration depends on pathway:

- Shopify: Native integration works like any Shopify Payments method

- Stripe: Stablecoin transactions appear in Stripe dashboard alongside card payments

- Custom: Requires webhook handling for payment confirmations and settlement logic

Accounting systems receive transaction records through existing payment processor APIs. Stablecoins appear as payment method type (similar to “Visa” or “PayPal” in transaction records).

What happens to customer data and privacy?

Blockchain transactions are pseudonymous, customer wallet addresses are visible on-chain but not linked to personal identities without additional information. Payment processors handle KYC/AML requirements the same as traditional payments.

For most implementations, customer personal data (name, email, shipping address) remains in your existing systems and doesn’t touch the blockchain. Only the payment transaction (amount and wallet addresses) processes on-chain.

GDPR and privacy regulations apply the same as traditional payments. Payment processors are responsible for compliance with data protection laws.

What if customers don’t have crypto wallets?

Multiple solutions eliminate wallet friction:

Guest Checkout: Customers pay with credit card at checkout. Payment processor converts to USDC in the background. Merchant receives stablecoin settlement. Customer never realizes blockchain was involved.

Embedded Wallets: Platform creates wallet automatically during first purchase. Customer logs in with email/password (no private key management). Wallet exists but complexity is abstracted.

One-Click Setup: Major wallets (Metamask, Rainbow, Coinbase Wallet) now offer one-click setup flows integrated directly into checkout. Customer creates wallet during purchase without leaving merchant site.

Shopify enables guest checkout by default, so merchants can accept stablecoin payments without requiring customers to own wallets.

How do we educate customers about stablecoin payments?

Best practice: Don’t over-explain. Successful implementations treat stablecoins like any payment method.

Checkout messaging: “Pay with USDC” or “Pay with digital dollars” works better than technical blockchain explanations. Most customers care about speed and fees, not underlying technology.

Optional education: Provide help link near payment option: “What is USDC?” → Simple explanation: “Digital dollars that settle instantly with low fees.”

Post-purchase: After successful transaction, optional email: “You paid with USDC and saved $X in fees. Next time, payment will be even faster.”

TransFi’s 25% cart abandonment reduction came from adding the option without heavy education campaigns. Customers who want it recognize it; others use traditional methods.

What regulatory compliance do we need to maintain?

Federal Level (United States):

GENIUS Act (July 2025) established federal stablecoin framework requiring:

- Reserve backing (1:1 dollar reserves)

- Monthly audits by major accounting firms

- Federal licensing for stablecoin issuers (Circle, Tether, PayPal)

- Consumer protection standards

Merchant obligations: None beyond existing payment processing compliance. Payment processors (Stripe, Coinbase, PayPal) hold money transmission licenses and handle regulatory requirements.

International:

- EU: MiCA (Markets in Crypto-Assets) provides similar framework

- UK: FCA regulations for stablecoin issuers

- Other jurisdictions: Varying approaches, but payment processors handle compliance

Tax reporting: Payment processors generate 1099 forms for stablecoin transactions (same as PayPal or Venmo). Stablecoin receipts are taxable income like any payment method.

What happens if a stablecoin loses its peg?

Reserve-backed stablecoins (USDC, USDT, PYUSD): Maintain dollar parity through actual cash/Treasury reserves. Historical performance shows USDC maintained parity within 0.03% for vast majority of existence. Temporary deviations (e.g., Silicon Valley Bank situation, March 2023) corrected within 72 hours.

Algorithmic stablecoins (Terra/UST – collapsed 2022): Used mathematical formulas without reserve backing. Fundamentally different architecture.

Merchant protection strategies:

- Auto-convert to fiat immediately: Exposure window only 2-6 minutes (transaction confirmation time)

- Diversify across multiple stablecoins: Accept USDC + USDT + PYUSD to reduce single-issuer risk

- Monitor reserves: Check monthly audit attestations published by issuers

- Traditional fallback: Keep credit cards and other methods enabled

Payment processors typically provide automatic conversion options that eliminate holding period risk entirely.

What’s Torsion’s role in stablecoin implementation?

Torsion helps e-commerce platforms adopt stablecoin payments through technical integration, compliance guidance, and optimization.

Services provided:

- Platform-specific integration: Shopify Plus, WooCommerce, Magento, custom platforms

- Technical implementation: API integration, testing, deployment support

- Compliance frameworks: GENIUS Act guidance, documentation, audit preparation

- Customer experience optimization: Checkout flow design, wallet friction reduction

- Performance monitoring: KPI tracking, A/B testing, ongoing improvement

Value proposition: Engineering teams focus on core product while Torsion handles payment infrastructure complexity. Faster implementation (4-8 weeks vs. 6-12 months DIY), expert compliance navigation, and proven playbooks from merchant implementations across segments.

When to partner vs. DIY:

- DIY: Simple Shopify implementation, strong internal blockchain expertise

- Partner: Custom platforms, compliance-heavy industries, resource-constrained teams, strategic speed priority